Introduction

Picture this: an entrepreneur holds equity across eight different stocks—but all of them are IT companies. When a sector-wide correction hits, his portfolio drops 30% in three months. On paper, he was "diversified." In practice, he had concentrated all his eggs in one industry basket.

This scenario plays out repeatedly among affluent investors who confuse the number of holdings with genuine diversification. The deeper issue is structural: without a deliberate allocation strategy, even a large portfolio can carry hidden concentrations that derail financial goals.

What follows is a practical framework for building portfolios that hold up when markets don't — covering allocation strategy, Indian asset class behavior, portfolio construction, and rebalancing.

Key Takeaways

- Asset allocation sets the proportions across major asset classes (equity, debt, gold, real estate); diversification spreads risk within each class

- The right allocation is personal—goals, time horizon, and risk tolerance all shape it

- Owning multiple stocks in the same sector is not diversification—true diversification spans sectors, instruments, and geographies

- Rebalancing prevents your portfolio from drifting into unintended risk territory as markets move

- Neither strategy eliminates losses, but together they improve your portfolio's risk-adjusted returns over time

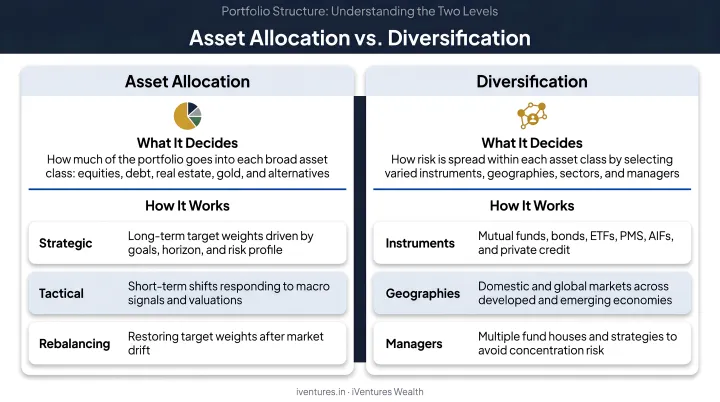

Asset Allocation vs. Diversification: What's the Difference?

These two terms are often used interchangeably. They shouldn't be.

Asset allocation is the structural blueprint of your portfolio—the deliberate decision about what percentage of your total wealth goes into broad asset classes like equity, debt, gold, real estate, and alternatives. It answers: how much in each bucket?

Diversification operates one level down. Once you've decided how much goes into equity, diversification determines what you hold within that equity bucket—across companies, sectors, market caps, and geographies.

Put simply: allocation sets the structure; diversification fills it intelligently. A portfolio with four asset classes but concentrated bets within each one is only half-built.

Why Both Matter Simultaneously

A multi-asset portfolio can still be dangerously undiversified. Consider an investor with 60% in equity, 30% in debt, and 10% in gold—a reasonable-looking allocation on the surface.

If that equity sleeve holds five stocks, all in the banking sector, a banking crisis strips out the portfolio's entire growth engine regardless of how the debt or gold portions perform.

The reverse is also true: you can own 50 stocks and still be poorly allocated if all 50 are equities and your goal is three years away.

As AMFI notes, spreading investments across asset classes means risk in one category can be countered by others. That said, both concepts have real limits:

- Neither allocation nor diversification guarantees profits

- They reduce—but do not eliminate—the possibility of loss

- Both are risk management tools, calibrated to your return goals and time horizon

- Their effectiveness depends on how well the underlying choices are executed

The Major Asset Classes and Their Risk-Return Profiles

Understanding what each asset class does—and how they interact—is the foundation of intelligent allocation.

Equity

Equity offers the highest long-term return potential among mainstream asset classes, alongside the highest short-term volatility. The Nifty 50 has delivered a 12.38% CAGR since inception (base date November 1995), making it the primary benchmark for Indian large-cap equity returns.

Indian investors can access equity through:

- Direct stocks on NSE/BSE

- Equity mutual funds (large-cap, mid-cap, small-cap, flexi-cap)

- Index funds and ETFs tracking Nifty 50 or Nifty 500

- International equity funds for global exposure

Equity is most appropriate for goals with a 7-year-plus horizon, where time absorbs volatility.

Debt Instruments

Debt—bonds, government securities, corporate bonds, and debt mutual funds—serves as portfolio ballast. Returns are lower than equity but more predictable, making debt valuable during equity downturns and essential for goals within shorter timeframes.

Key debt categories, each carrying a distinct maturity and credit risk profile:

- Liquid and ultra-short-duration funds — for capital preservation and near-term liquidity

- Gilt funds — for duration exposure backed by sovereign credit

- Corporate bond funds — for yield pickup with managed credit risk

- Dynamic bond funds — for active interest rate positioning

The distinction between these categories matters more than most investors realise.

Gold

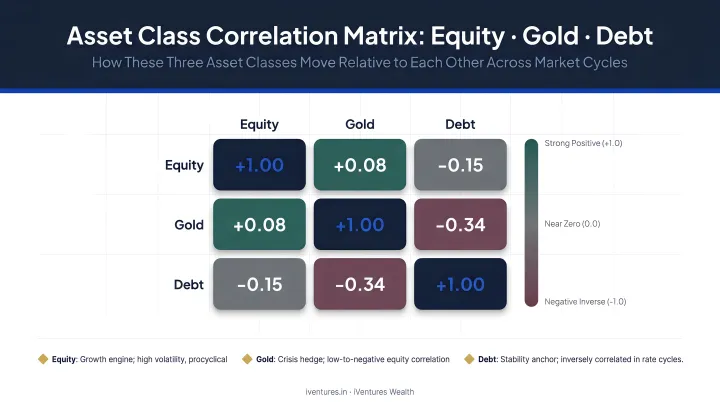

Gold plays a dual role in Indian portfolios: it is both culturally entrenched and structurally relevant as a diversifier. Accessible via Sovereign Gold Bonds (SGBs), Gold ETFs, or digital gold, it has historically shown low correlation with Indian equities.

Indian data from 2000 to 2022 shows gold's equity correlation was negative during the Global Financial Crisis (coefficient: -0.06), then turned positive during COVID-19 (coefficient: +0.14). The World Gold Council's analysis found that a 7.5%–15% gold allocation improved risk-adjusted returns over the 19-year period ending December 2025. Gold is a reliable diversifier on balance — but its crisis-hedge properties are context-dependent, not guaranteed.

Real Estate, REITs, and Alternatives

Unlike gold, which offers liquid market access, direct real estate demands large capital, low liquidity, and long horizons. REITs provide liquid access to commercial real estate—Mindspace REIT, for instance, has delivered annualised returns of 13.3% with a distribution yield of 6.9% as of Q4 FY25.

For UHNIs and family offices, alternative investment funds (AIFs) across Category I, II, and III offer access to private equity, private credit, and hedge-fund-style strategies. Private credit in particular has gained ground as a yield-enhancement tool, with some AIF strategies targeting 12–16% IRR through senior secured lending. These carry category-specific risks and typically require a minimum ₹1 crore commitment per SEBI regulations.

The Correlation Principle

What makes multi-asset allocation effective is correlation—or the lack of it. Asset classes that don't move in tandem with each other reduce overall portfolio volatility when combined. Mixing uncorrelated assets (equity + gold, for example) is precisely why a diversified portfolio typically experiences smaller drawdowns than a single-asset portfolio, even if each individual asset class carries risk on its own.

What Determines the Right Asset Allocation for You

There is no universal formula. The right allocation emerges from the intersection of three personal factors.

Financial Goals and Time Horizons

Different goals carry different timelines, and timelines drive allocation. A goal 20 years away can absorb equity's short-term volatility and benefit from compounding. A goal 3 years away cannot.

Consider two investors:

- A 35-year-old founder building a retirement corpus has 25+ years. A high equity allocation (60–75%) makes sense, since short-term corrections are recoverable and compounding needs time to work

- A 58-year-old CXO approaching retirement in 5–7 years needs capital preservation. A tilt toward debt and gold protects the portfolio from a poorly-timed market downturn just before withdrawal

The timeline difference between these two investors isn't just a number — it changes the entire structure of the portfolio. iVentures Wealth maps each financial goal to a separate allocation sleeve rather than treating the entire portfolio as one pool. A client simultaneously planning for children's education (15-year horizon) and marriage (22-year horizon) gets two distinct goal buckets with separate asset allocation strategies, each calibrated to its specific timeline and corpus requirement.

Risk Tolerance vs. Risk Capacity

Time horizon tells you when you need the money. Risk profiling tells you how much turbulence you can handle getting there. The two concepts are related but measure different things:

- Risk capacity: how much portfolio loss your balance sheet can absorb without derailing your goals

- Risk tolerance: how much volatility you can stomach without making reactive decisions that lock in losses

An investor might have the financial capacity to ride out a 40% drawdown but sell in panic at 20%. Formal risk profiling, as required under SEBI's Investment Advisers framework, captures both dimensions, ensuring the recommended allocation reflects what you can actually hold through a difficult market, not just what you theoretically should.

Life Stages and Evolving Allocation

Allocation is not a one-time decision. A framework appropriate at 35 should shift gradually as you approach 55 and then 65. PFRDA's NPS Auto Choice lifecycle funds offer a regulated example of this principle: equity exposure tapers as age increases, moving through LC75, LC50, and LC25 options.

For UHNIs and family offices with assets spread across multiple entities (operating businesses, promoter equity, corporate treasury, trusts), developing a coherent consolidated allocation requires viewing the entire balance sheet together. Concentration risks and gaps that are invisible when each account is reviewed separately become apparent only at the consolidated level. iVentures Wealth addresses this through a unified family wealth dashboard that brings together exposures across all entities, giving families a complete picture of where their wealth actually sits.

How to Build a Diversified Portfolio

Diversification operates at two levels, and most investors only pay attention to one.

Across Asset Classes

This is the level most people understand: hold equity, debt, gold, and potentially real estate or alternatives in proportions suited to your goals. Each class responds differently to market conditions — when equities fall, debt or gold often holds steady — and holding them together reduces drawdowns and dampens overall portfolio volatility.

Within Asset Classes

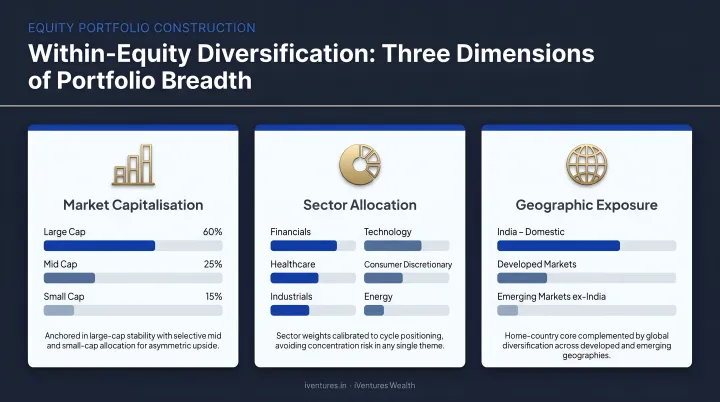

This is where genuine diversification gets built—or lost. Within equity specifically:

- By market cap: large-cap, mid-cap, and small-cap companies have different return and risk profiles

- By sector: holding five IT stocks is not diversification; a truly diversified equity sleeve spans multiple sectors

- By geography: Indian equities represent roughly 3% of global market capitalisation, yet most Indian investors have 90%+ of their equity in India—a concentrated home-country bet

Within debt: varying maturities (short, medium, long) and credit quality (government versus corporate) reduces interest rate and credit risk.

Avoiding Sector Concentration

AMFI classifies sectoral funds as investing in a single sector. These can deliver strong returns when their sector runs, but concentration risk is persistent. Owning multiple sectoral funds in the same industry is effectively the same as owning individual stocks in that sector.

Common sectors where this trap appears:

- Banking and financial services funds held alongside PSU bank funds

- Two or three technology-focused funds with near-identical holdings

- Infrastructure and capital goods funds that overlap significantly in underlying stocks

Using Pooled Instruments Efficiently

Mutual funds, ETFs, and index funds simplify diversification by providing instant exposure to dozens or hundreds of underlying securities. The Nifty 500 index, for instance, covers approximately 92% of NSE's free-float market capitalisation across the top 500 companies. A single index fund tracking this provides far broader exposure than most investors can replicate through stock-picking alone.

Fund overlap is the key caveat. Holding five large-cap mutual funds that all own the same top-20 Nifty 50 stocks creates the illusion of diversification without the substance. Portfolio consolidation reviews regularly surface this pattern among investors who have accumulated funds across multiple advisors over the years — iVentures Wealth's Asset Consolidation service specifically addresses this.

For global exposure, the RBI's Liberalised Remittance Scheme permits resident Indians to remit up to USD 250,000 per financial year for overseas investments—an accessible route to geographic diversification through international funds and ETFs.

Portfolio Rebalancing: Staying True to Your Strategy

Even a well-constructed portfolio drifts over time. Rebalancing is how you correct that drift.

Why Portfolios Drift

Imagine a 60/40 equity-debt portfolio constructed three years ago. A sustained equity bull run pushes the equity allocation to 75%, with debt shrinking to 25%. The investor's risk profile hasn't changed—but the portfolio now carries significantly more equity risk than originally intended. If a correction arrives, the damage is larger than planned for.

Rebalancing restores the original structure—and two approaches make that possible.

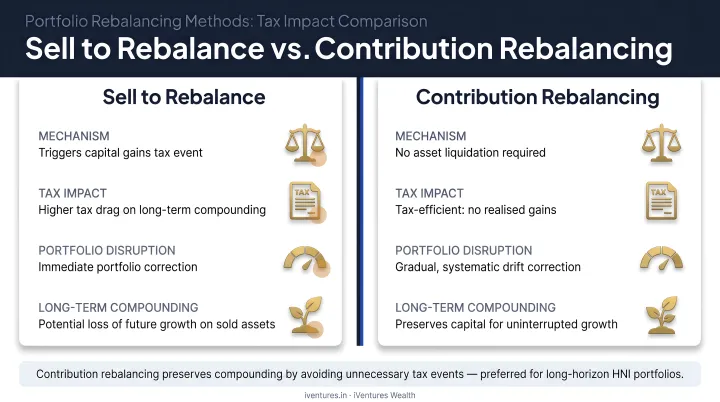

Two Rebalancing Methods

- Sell to rebalance: liquidate a portion of the overweighted asset class and redeploy proceeds into underweighted ones. Simple and direct, but triggers a capital gains tax event

- Rebalance through contributions: direct fresh investments into underweighted asset classes over time. No existing holdings are sold, so no tax event is triggered

Under India's post-Budget 2024 capital gains framework, short-term gains on equity and equity mutual funds attract 20% tax, while long-term gains (held over 12 months) attract 12.5%, with an LTCG exemption of ₹1.25 lakh per financial year. Which method you choose should factor in these tax implications — the difference in net outcome can be material at higher portfolio sizes.

When to Rebalance

Most advisers recommend reviewing allocation annually or semi-annually at minimum. A threshold-based trigger—rebalancing when any asset class drifts more than 5–10% from its target—adds a safety net between scheduled reviews.

iVentures Wealth's Wealth Monitor App provides consolidated portfolio views that display current allocation across asset classes, making it straightforward to spot when an asset class has drifted beyond its target allocation and a rebalance is overdue. Clients also receive quarterly portfolio reviews where tax-loss harvesting windows and capital gains timing are considered as part of any rebalancing recommendation.

Frequently Asked Questions

What is the difference between asset allocation and diversification?

Asset allocation determines what proportion of your total portfolio goes into broad categories—equity, debt, gold, real estate. Diversification spreads holdings within each category to reduce concentration in any single security, sector, or geography. Both work together but address different dimensions of risk.

Is 70/30 better than 60/40?

Neither is universally superior. A 70/30 equity-heavy split suits investors with long time horizons (10+ years) and high risk tolerance. A 60/40 split is more moderate and better suited to investors who are 5–8 years from a major goal or uncomfortable with sharp drawdowns. The right split depends on your personal goals, income stability, and risk capacity.

What is the 40-40-20 rule in investing?

The 40-40-20 rule is a simple guideline suggesting 40% in equity, 40% in debt, and 20% in alternatives like gold or real estate. It's a useful starting reference point for moderate-risk investors, but not a formula—actual allocation should be tailored to your specific goals, time horizon, and risk profile.

How often should I rebalance my portfolio?

Annual or semi-annual reviews work well as a baseline, supplemented by threshold-based checks when any asset class drifts more than 5–10% from its target. Before executing changes, weigh transaction costs and capital gains tax implications—contributing new funds to underweight assets often rebalances without triggering taxable events.

Can diversification fully protect against investment losses?

No. Diversification reduces the impact of any single investment failing, but it cannot eliminate market-wide risk. During broad downturns—like 2008 or COVID-19—most asset classes fall together in the short term, though a well-diversified portfolio typically recovers more steadily than a concentrated one.