India's appeal as a destination for NRI savings has grown steadily. According to World Bank estimates, India received approximately USD 129 billion in remittances in 2024 — the largest in the world — reflecting the scale of diaspora capital flows back into the country. A meaningful portion of this finds its way into fixed deposits.

This article covers the three NRI FD types, current indicative rate ranges, what drives those rates, and how to pick the right structure for your goals.

Key Takeaways

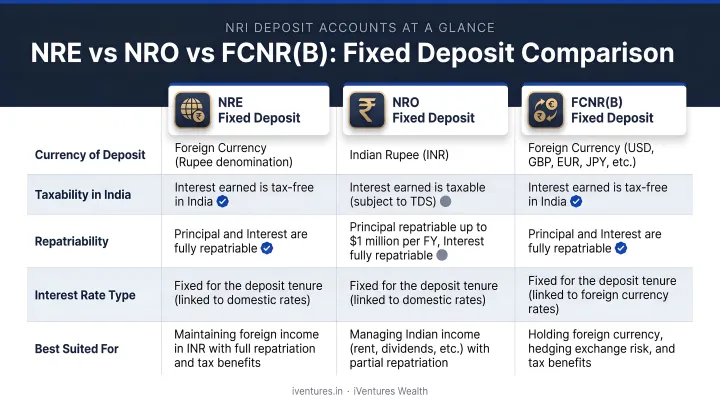

- NRI FDs come in three types — NRE, NRO, and FCNR(B) — each with distinct tax treatment, repatriation rights, and rate structures

- NRE and FCNR(B) interest is fully tax-free in India; NRO interest attracts 30% TDS (reducible under DTAA)

- INR NRE/NRO rates currently range ~6.25%–7.25% p.a. across major banks; FCNR(B) USD rates sit between ~3.85%–6.00% p.a., varying by tenure and bank

- Choosing the wrong FD type reduces effective returns — even when nominal rates look identical

- For NRIs with substantial portfolios, FDs work best as the debt anchor within a broader strategy, not as a standalone instrument

What Are NRI Fixed Deposits? The Three Account Types Explained

NRI Fixed Deposits are term deposits governed by FEMA, available exclusively to Non-Resident Indians, OCIs, and PIOs. Unlike standard resident FDs, these accounts differ in fund source, tax treatment, and repatriation rights — and choosing the wrong type can cost you significantly in tax or liquidity.

NRE Fixed Deposit

Funded from foreign income converted to INR. What you need to know:

- Tax treatment: Interest and principal are fully exempt from Indian income tax under Section 10(4)(ii) of the Income Tax Act

- Repatriation: Both principal and interest are freely repatriable — no RBI approval, no annual cap

- Tenure: Minimum 1 year, up to 10 years

- Best for: NRIs who want to park overseas earnings in India, earn market-rate INR returns, and retain the flexibility to move funds back

NRO Fixed Deposit

Designed for income earned within India — rent, dividends, pensions. Key features:

- Tax treatment: Interest is taxable; banks deduct TDS at 30% plus applicable surcharge and cess

- Repatriation: Capital repatriation is capped at USD 1 million per financial year, requiring Form 15CA/15CB and CA certification

- Tenure: 7 days to 10 years — the most flexible option for short-term parking of India-source income

- Best for: Managing existing Indian income, not for routing foreign earnings

FCNR(B) Fixed Deposit

Deposited and held in a permitted foreign currency — USD, GBP, EUR, AUD, CAD, JPY among others. Core mechanics:

- Tax treatment: Interest is tax-free in India; fully repatriable

- Currency exposure: Funds stay in your chosen foreign currency throughout — no INR conversion at entry, so rupee volatility doesn't affect your deposit value

- Tenure: 1 to 5 years; RBI requires interest to be calculated and paid at 180-day intervals

- Rates: Set by currency, not just tenure — USD FCNR rates track US Fed policy, not RBI repo

- Best for: NRIs who want to earn returns in their home currency without rupee exposure

The table below captures how these three accounts stack up across the factors that matter most to NRI investors.

Quick Comparison

| Feature | NRE FD | NRO FD | FCNR(B) FD |

|---|---|---|---|

| Currency of deposit | INR | INR | Foreign (USD, GBP, EUR, etc.) |

| Tax on interest | Exempt (Sec 10(4)(ii)) | 30% TDS + surcharge | Exempt |

| Repatriation | Fully free | USD 1M/year cap | Fully free |

| Tenure range | 1–10 years | 7 days–10 years | 1–5 years |

| Best use case | Foreign income, INR returns | India-source income | Avoid currency risk |

NRI FD Interest Rates: Ranges Across Account Types and Tenures

NRE and NRO FD rates are INR-denominated and track domestic bank deposit rates. Based on rate pages reviewed across major banks (SBI, ICICI, HDFC, Axis, Kotak) in mid-2026, the indicative cross-bank ranges are:

| Tenure Band | Indicative INR Rate Range |

|---|---|

| ~1 year | 6.25% – 7.25% p.a. |

| ~2 years | 6.40% – 6.60% p.a. |

| 3–5 years | 6.30% – 6.60% p.a. |

These are indicative ranges only. Rates vary by bank, deposit size, and special tenures, and change frequently. Verify directly with your bank before placing a deposit.

How Tenure Affects Rates

The relationship between tenure and rate is not linear. A few patterns hold across most banks:

- Mid-range tenures (1–3 years) tend to attract the most competitive rates

- Very short tenures (under 6 months for NRO) typically yield less

- Very long tenures (5+ years) often underperform the 1–3 year band

- Banks manage asset-liability profiles actively — a 2-year NRE FD may occasionally outperform a 5-year one

FCNR(B) Rate Dynamics

USD FCNR(B) rates are set independently of RBI's domestic repo rate. They are influenced by US Fed funds rates, LIBOR/SOFR benchmarks, and the individual bank's foreign currency funding needs.

Current indicative USD FCNR(B) ranges across major banks:

| Tenure Band | USD FCNR(B) Range |

|---|---|

| 1 year to <2 years | 3.85% – 4.40% p.a. |

| 2 years to <3 years | 3.55% – 3.85% p.a. |

| 3–5 years | 2.95% – 6.00% p.a. |

Figures differ by bank and callable/non-callable status. The wide spread at 3–5 years reflects structural differences across institutions — verify directly with individual banks.

When US rates are elevated, USD FCNR(B) deposits can compete meaningfully with INR NRE FDs — especially when the NRI also wants to avoid rupee exposure between deposit and eventual repatriation.

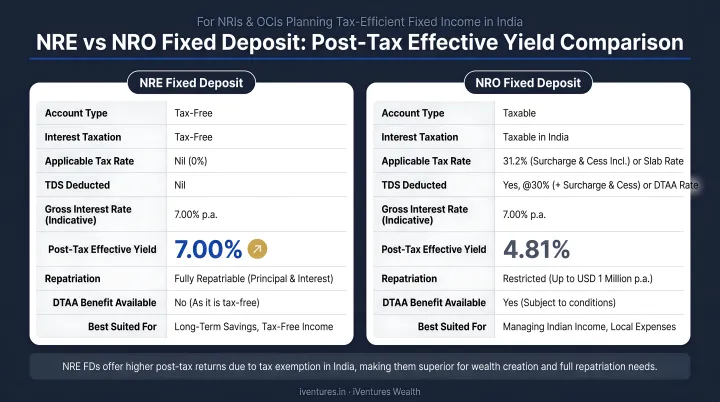

Post-Tax Rate: The Number That Actually Matters

A 7.5% NRO FD rate does not outperform a 7.0% NRE FD rate for most NRIs — the tax treatment makes all the difference:

- NRE FD at 7.0%: Effective post-tax yield = 7.0% (fully exempt)

- NRO FD at 7.5%: After 30% TDS = effective yield of ~5.25% (before surcharge and cess)

The gap is significant. NRIs who compare headline rates without accounting for TDS systematically underestimate the cost of parking foreign income in an NRO account.

Senior Citizen Rate Benefits

Some banks extend an additional 0.25%–0.50% p.a. to NRI depositors above age 60 on NRO FDs, but this is not universal. ICICI Bank, for example, explicitly states that senior citizen rates apply only to resident deposits — NRI FDs are excluded. HDFC and Kotak rate tables show senior citizen columns in NRO/NRE tables, but eligibility footnotes vary. Check with your specific bank before assuming this benefit applies.

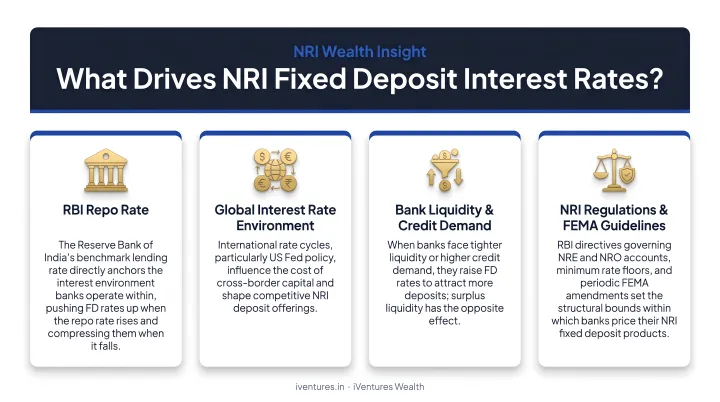

What Drives NRI Fixed Deposit Interest Rates

Four factors shape NRI FD rates. Understanding them helps you anticipate rate movements and time deposits more effectively.

RBI Policy and Repo Rate

INR NRE and NRO FD rates follow domestic monetary policy. When RBI raises the repo rate, banks typically raise deposit rates within weeks. When it cuts, rates follow. As of mid-2026, multiple market sources indicate the RBI repo rate is at 5.25% with a neutral stance — verify the current rate directly on the RBI press releases page before making rate-timing decisions.

FCNR(B) rates follow a different path — they track the policy rates of the respective foreign currency (US Fed, Bank of England, ECB), not RBI.

Bank-Specific Liquidity Needs

Banks with high credit-deposit ratios offer higher deposit rates to attract inflows. Smaller private banks and small finance banks frequently top the rate tables, but this comes with credit risk that PSU bank depositors don't face. For large NRI deposits, the trade-off between an extra 0.25%–0.50% and the counterparty profile of the institution deserves careful consideration.

Remittance Flows and Currency Conditions

When the INR weakens, NRI overseas earnings convert to more rupees, making Indian deposits more attractive. Banks respond by promoting special NRI deposit schemes to capture that inflow.

India is the world's largest remittance recipient — USD 120 billion in 2023 per World Bank data. Any meaningful currency depreciation reliably triggers NRI deposit rate competition across banks.

Deposit Amount and Negotiation

For large deposits — typically above ₹1 crore — some banks are willing to negotiate preferential rates outside their published schedules. This is especially relevant for UHNI NRIs. Published rate cards are a floor, not a ceiling; your bank's relationship manager is the right starting point for any deposit above that threshold.

Taxation and Repatriation: How They Shape Your Actual Returns

The headline rate is only part of the return equation. Tax and repatriation structure determine what arrives in your overseas account as usable funds.

Tax positions by account type:

- NRE FD: Interest exempt under Section 10(4)(ii) of the Income Tax Act — no TDS deducted

- FCNR(B) FD: Interest is tax-exempt in India — no TDS deducted

- NRO FD: Interest taxed at 30% TDS plus applicable surcharge and cess under Section 195

DTAA: Reducing the NRO Tax Bite

NRIs from countries with a Double Taxation Avoidance Agreement with India can claim reduced withholding rates on NRO interest. To claim this benefit, the NRI must submit:

- Tax Residency Certificate (TRC) from their country of residence

- Form 10F where the TRC does not contain all prescribed particulars

Example DTAA withholding rates on interest (verify treaty text before relying on these figures):

- USA: 15% in most individual cases (Article 11 of India-US treaty)

- Canada: ~15% under Article 11 (India-Canada treaty)

- UAE: India-UAE DTAA exists — the exact NRO interest rate requires official treaty verification before application

For NRIs from the US paying the full 30% TDS on NRO interest, switching to the DTAA rate could cut the effective tax by half. iVentures Wealth assists NRI clients with this process, covering TRC management, Form 10F filing, and Form 15CA/15CB compliance for NRO repatriation.

Repatriation Rules

| Account | Capital Repatriation | Process |

|---|---|---|

| NRE FD | Fully free, no limit | No additional documentation required |

| FCNR(B) FD | Fully free, no limit | No additional documentation required |

| NRO FD | USD 1 million per financial year | Requires Form 15CA/15CB and CA certificate |

The NRO repatriation cap matters most for NRIs with large lump sums sitting in NRO accounts (sale proceeds, inheritance, rental accumulation). If your India-source wealth exceeds USD 1 million, a multi-year repatriation plan becomes necessary, not just an FD strategy.

How to Choose the Right NRI FD for Your Financial Goals

A Simple Decision Framework

| Your Goal | Recommended Account |

|---|---|

| Park foreign income in India, earn INR returns, full repatriation flexibility | NRE FD |

| Manage rent, dividends, or pension income already in India | NRO FD |

| Earn returns in USD/GBP/EUR without rupee exposure | FCNR(B) FD |

| Planning to return to India within 1–2 years | Convert NRE to resident account on return — tax exemption ends at that point; review tenure carefully before locking in |

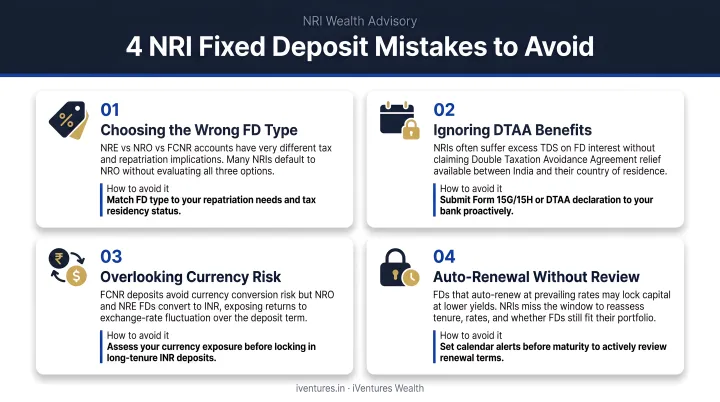

Common Mistakes to Avoid

NRIs regularly make four costly errors with FD selection:

- Using NRO for foreign income — deposits foreign earnings into an NRO account, triggering 30% TDS that a NRE account would have avoided entirely

- Treating nominal rate as effective rate — comparing a 7.5% NRO rate with a 7.0% NRE rate without calculating post-TDS yields

- Breaking FDs prematurely — penalties of 0.5%–1.0% interest reduction are standard across major banks; NRE and FCNR(B) FDs earn zero interest if withdrawn before the 1-year minimum tenure

- Ignoring currency risk on NRE accounts — NRE FDs are held in INR. If the rupee depreciates between deposit and repatriation, real returns in your home currency can be lower than the INR rate suggests, despite the tax exemption

Where FDs Fit in a Broader NRI Portfolio

FDs serve a specific function — capital preservation, predictable cash flow, and low volatility. They are not an investment strategy by themselves. For NRIs with significant India-linked wealth, FDs typically anchor the debt portion of a portfolio that also includes debt mutual funds, bonds, and equity exposure.

Calibrating that mix correctly — across tax status, repatriation timelines, currency exposure, and estate planning — is where most NRIs benefit from structured advisory. iVentures Wealth, a SEBI-registered adviser, integrates FDs with debt funds, bonds, and equity into a coordinated portfolio that is tax-efficient, repatriation-ready, and built around long-term goals from the outset.

Frequently Asked Questions

Can an NRI deposit in a fixed deposit (FD) in India?

Yes. NRIs, OCIs, and PIOs can open NRE, NRO, or FCNR(B) FDs with any authorised bank in India. The account type depends on whether the funds originate from overseas income or India-based earnings.

What is an NRI deposit?

An NRI deposit is a term deposit available to Non-Resident Indians under FEMA regulations. It comes in three forms: NRE, NRO, and FCNR(B), each suited to different income sources, tax preferences, and repatriation needs.

How much money can an NRI deposit in India?

RBI has not set an upper limit on NRE or FCNR(B) FD amounts. NRIs can hold multiple FDs across banks without a cap on the deposit amount itself. For NRO accounts, the repatriation of capital (not the deposit itself) is capped at USD 1 million per financial year.

Which NRI FD type offers the highest interest with a tax-free benefit?

NRE FDs typically offer the best combination: competitive INR rates that generally track domestic FD rates, with full tax exemption and free repatriation. FCNR(B) FDs may outperform in periods of elevated foreign currency interest rates, particularly for USD deposits when US rates are high.

Is TDS deducted on NRI fixed deposit interest?

NRE and FCNR(B) interest is fully tax-exempt in India — no TDS applies. NRO FD interest attracts TDS at 30% plus surcharge and cess. This rate can be reduced under an applicable DTAA by submitting a Tax Residency Certificate and Form 10F.

Can NRIs break an FD before maturity?

Yes, premature withdrawal is allowed for all NRI FD types, though banks apply a penalty of 0.5%–1.0% on the applicable interest rate. For NRE and FCNR(B) FDs, banks pay no interest at all if the deposit is closed before completing the 1-year minimum tenure.