This tension—high earning potential compressed into a short runway—defines the financial lives of most Indian physicians. The training path is long: MBBS plus a 12-month compulsory internship, then a 3-year MD/MS, and for super-specialists another 3-year DM/MCh. According to NMC regulations, that's potentially over a decade before you draw a full attending salary.

This guide walks through a structured, India-specific financial roadmap—from managing education debt to building generational wealth—at every stage of a medical career.

Key Takeaways

- Start small investments during residency; even ₹2,000/month SIPs matter over 30 years

- Use the loan moratorium period to build an emergency fund, not spend freely

- Max out Section 80C (₹1.5 lakh) and 80CCD(1B) (₹50,000) every financial year

- Supplement employer group health cover with a personal policy and malpractice insurance

- Treat real estate as one component of a diversified wealth plan, not the whole strategy

Why Physicians Face Unique Financial Challenges

The Delayed Earnings Problem

Most engineering or commerce graduates begin earning at 22–23. A physician completing super-specialisation may not draw a full attending salary until their mid-30s. That gap isn't just a delay—it's compounding time lost permanently.

Those lost years matter more than most physicians realize—and the delayed start is only part of the problem.

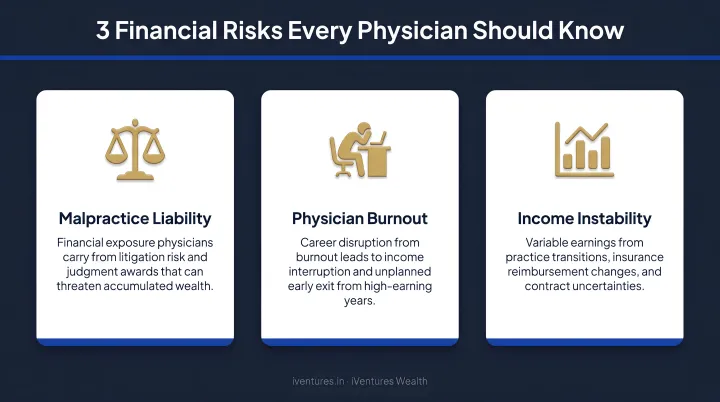

A Profession with Specific Financial Risks

Beyond the delayed start, a 2023 study published in a peer-reviewed Indian journal found that only 34% of healthcare professionals in India had basic financial literacy, and just 12% had invested in mutual funds or stocks. This isn't surprising—financial planning has never been part of the medical curriculum.

Other profession-specific risks include:

- The IMA's National Professional Protection Scheme covers up to ₹10 lakh per case and ₹20 lakh per year—amounts that can fall well short of actual malpractice litigation costs

- Burnout prevalence among Indian doctors ranges from 20.7% to 86% (2025 scoping review), often forcing career pauses or specialty changes with no financial buffer in place

- Private practitioners and locum physicians routinely face months of unpredictable earnings, particularly in the early years of practice

Managing Medical Education Debt

The Moratorium Period Strategy

Most education loans under the IBA Model Education Loan Scheme include a repayment holiday covering the course period plus a buffer after completion. Banks like SBI, ICICI, and Axis typically structure this moratorium into their loan terms.

The mistake many early-career physicians make: treating the moratorium as free money. It isn't. Use this window to build your emergency fund—3 to 6 months of essential expenses in a liquid instrument. When EMIs begin, you want to be paying from a position of security, not scrambling.

Debt Avalanche vs. Debt Snowball

Two repayment strategies, both legitimate—but they suit different personalities:

| Strategy | Method | Best For |

|---|---|---|

| Debt Avalanche | Tackle highest-interest loan first | Minimises total interest paid; mathematically optimal |

| Debt Snowball | Clear smallest loan first | Psychological wins; motivates consistent repayment |

For physicians whose income will grow significantly over time, the Debt Avalanche is generally more efficient. But if staying motivated is the challenge, starting with a smaller loan and clearing it quickly is better than the "optimal" strategy you abandon after six months.

The Parallel Investing Dilemma

Should you invest while still repaying loans? The answer depends on the interest rate.

SBI currently charges 8.90% on collateralised education loans above ₹7.5 lakh, while ICICI ranges from 9% to 13%. If your loan rate is below 8–9%, running debt repayment and equity SIPs simultaneously often makes more sense than waiting until the loan is fully cleared.

Here's a simple illustration:

- ₹5,000/month SIP started at age 28 vs. age 33

- At a 12% assumed CAGR over 30 years vs. 25 years

- The 5-year head start can generate a corpus roughly 40–60% larger. Compounding punishes delay more than most people expect.

A Practical Budget for Early-Career Physicians

For a resident or junior attending earning ₹80,000–₹1,00,000/month:

- ₹40,000–50,000 — EMI + essential expenses (rent, food, transport)

- ₹20,000–25,000 — Loan prepayment or additional EMI acceleration

- ₹5,000–10,000 — SIP (equity mutual fund or ELSS)

- ₹5,000–10,000 — Emergency fund build-up

It feels tight—and that's the point. Physicians who hold this structure through their early years typically enter their peak earning years with both a debt-free balance sheet and an SIP portfolio already 5–7 years into compounding.

Building the Financial Foundation

Budgeting Rules That Actually Work

Two popular frameworks, with different use cases:

50-30-20 Rule — 50% needs, 30% wants, 20% savings. Works well for established physicians with cleared debt and stable income.

70-10-10-10 Rule — 70% expenses, 10% short-term savings, 10% long-term investments, 10% giving or discretionary. Better suited to debt-heavy early-career phases where the savings allocation feels more achievable.

Neither rule is perfect. The point is to have a structure at all, which most physicians don't.

Emergency Fund and Insurance

Emergency fund targets:

- Salaried hospital physician: 4 months of essential expenses

- Private practitioner or locum: 6 months minimum, given income variability

Keep this in a liquid mutual fund or high-yield savings account—not locked away in fixed deposits with penalties for early withdrawal.

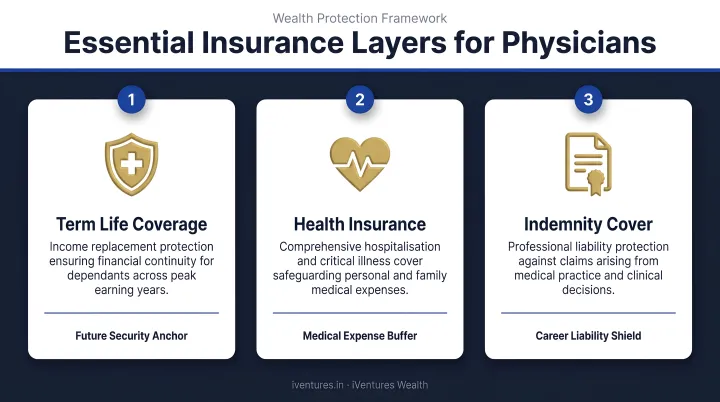

The three insurance layers every physician needs:

- Term life insurance — Cover of 10–15x annual income. Buy it young; premiums can run 40–60% lower in your 30s than in your 40s

- Comprehensive health insurance — Do not rely on employer group health cover alone. Coverage gaps and portability issues make a personal policy non-negotiable

- Professional indemnity insurance — The IMA's NPPS scheme has coverage limits; standalone malpractice insurance provides broader protection

One additional layer often overlooked: own-occupation disability cover. A hand tremor or neurological condition can end a surgeon's or specialist's career even if they can still work in a limited role. For a specialist earning ₹30–50 lakh annually, that lost income is rarely replaced by general practice or administrative work.

Estate Planning Isn't for Later

Many physicians assume estate planning is a retirement concern. It isn't. The moment you accumulate meaningful assets—investments, a vehicle, savings—you should have:

- A will drafted and registered

- Nominations updated across every financial account, PF, and insurance policy

- A conversation about trust structuring if you have dependents

Without these in place, even a well-built portfolio can become a legal dispute during a family's most difficult moment.

Tax Planning Every Physician Should Use

Section 80C and Beyond

The ₹1.5 lakh annual 80C limit is well known. Less known is how to use it well:

- ELSS mutual funds — Equity-linked, 3-year lock-in, best for wealth creation within 80C

- PPF — Safe, long-term, tax-free maturity; illiquid but excellent for the conservative portion of a portfolio

- NPS contributions — The additional ₹50,000 deduction under Section 80CCD(1B) is over and above the ₹1.5 lakh 80C ceiling, making the total potential deduction ₹2 lakh

Most physicians leave the 80CCD(1B) deduction unused — because no one told them it exists.

Section 80D for Health Insurance

- Up to ₹25,000 deduction for premiums paid for self, spouse, and children

- Additional ₹25,000–₹50,000 for parents (₹50,000 if parents are senior citizens)

- Preventive health check-up costs covered up to ₹5,000 within these limits

Private Practitioners: Profession-Specific Deductions

Physicians filing under "Profits and Gains from Business or Profession" — governed by Section 44AA of the Income Tax Act — can claim deductions beyond the standard 80C/80D options:

- Clinic operating expenses — rent, staff salaries, consumables

- Equipment depreciation under Section 32

- CME costs and professional subscriptions — deductible under the general business expense provision in Section 37

Verify CME and subscription deductibility with your CA, as applicability can vary. Taken together, these deductions can meaningfully lower a private practitioner's tax outgo — provided expenses are tracked and documented. Most aren't.

Building Long-Term Wealth

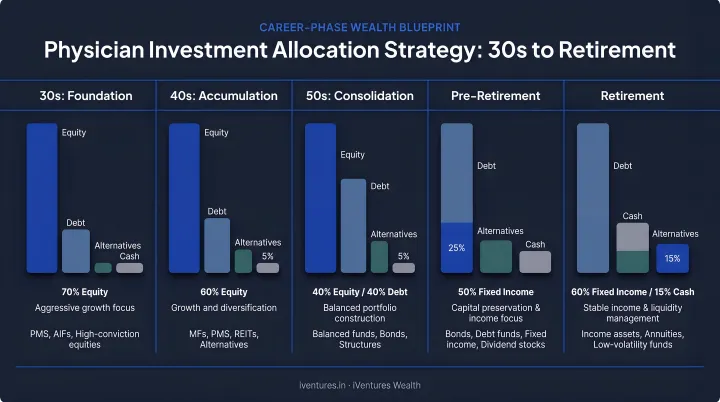

Investment Approach by Career Phase

Because physicians begin serious investing later than most professionals, the equity allocation needs to be more aggressive in the early years:

| Career Phase | Allocation Focus |

|---|---|

| 30s (Early Career) | 70–80% equity (mutual funds, ELSS, NPS equity tier) |

| 40s (Mid-Career) | Balanced: add real estate exposure and debt instruments |

| 50s+ (Pre-Retirement) | Capital preservation; gradual shift to lower-volatility instruments |

The NPS Equity Tier I has delivered a 10-year CAGR of 12.92% historically, according to the NPS Trust Annual Report 2022-23. Past performance isn't a guarantee, but it illustrates the long-term compounding potential of staying invested through market cycles.

Retirement Corpus Planning: A Practical Illustration

Goal-based planning starts with a number. Here's a simple framework:

- Assume you want ₹2,00,000/month in today's money after retirement at 60

- Over a 25-year retirement, adjusted for inflation (RBI's medium-term CPI target is 4%), that monthly need grows substantially

- Using a corpus depletion model, many financial planners estimate you need roughly 20–25x your annual retirement expenses as a corpus at retirement

The specific number will depend on your lifestyle, dependents, healthcare costs, and income sources. Calculate it now. Waiting until 55 leaves far less room to course-correct.

Real Estate: A Component, Not a Strategy

RBI Household Finance Committee data shows Indian households hold 77% of their assets in real estate and less than 5% in equities, mutual funds, and bonds. Physicians often mirror this pattern, partly from cultural preference and partly from distrust of financial markets.

That concentration is a risk, not a strategy. Real estate has a place in a diversified portfolio, but as the primary wealth vehicle, it carries serious drawbacks:

- Illiquidity — you can't sell 20% of your flat to fund a goal

- Maintenance drag and tenant risk for rental properties

- Single-city concentration that ties your wealth to one market

iVentures Wealth, which has advised medical professionals and HNIs since 2005, maps real estate as one component within a broader wealth plan. Equity, debt, and alternative assets are structured around each physician's career stage and risk profile—so no single asset class dominates the portfolio.

Common Financial Mistakes Physicians Must Avoid

Lifestyle Inflation After Residency

The jump from a resident stipend to an attending salary is dramatic. The temptation to upgrade everything — car, apartment, holidays — all at once is real and understandable.

The problem: every ₹50,000/month spent on lifestyle instead of investments at age 32 is not just ₹50,000. At 12% CAGR over 25 years, that monthly amount becomes roughly ₹94 lakhs in corpus. Delay wealth-building by 5 years through lifestyle inflation, and the retirement corpus gap becomes enormous.

Upgrade gradually — one major change at a time, not all at once.

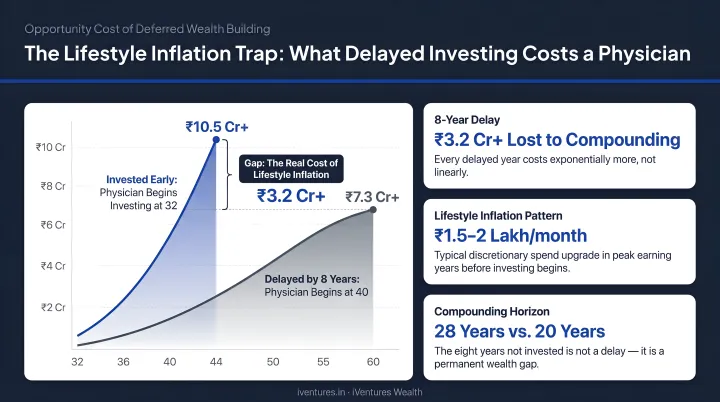

Waiting Until Debt Is Cleared to Invest

This is the most costly mistake physicians make. Waiting until an education loan is fully paid before starting SIPs or NPS contributions means sacrificing the most powerful variable in wealth creation: time.

If your loan interest rate is moderate (sub-9%), running parallel debt repayment and investments is almost always the better strategy. The compounding you miss during a 5-year "wait until debt is gone" phase is not recoverable.

Underbuying Insurance

Many physicians rely on employer group health policies and assume malpractice insurance is unnecessary because "it won't happen to them." Both assumptions create significant financial exposure.

A single malpractice claim (even one eventually settled or dismissed) can involve legal costs, lost time, and reputational damage that no group policy will cover. Key gaps to address:

- The IMA NPPS scheme helps, but per-case limits may fall short in complex litigation

- A private indemnity policy fills what employer cover leaves unprotected

- A standalone health policy with adequate sum insured is a baseline requirement, not an optional extra

Frequently Asked Questions

What are common budgeting rules for financial planning for physicians?

The 50-30-20 rule (needs/wants/savings) works well for established physicians with stable income and cleared debt. Early-career physicians managing EMIs typically do better with the 70-10-10-10 structure, which keeps the savings target more realistic during the high-debt phase and builds the discipline to invest consistently even when margins are thin.

What are the key steps in financial planning for physicians?

The sequence matters: assess total debt and build an emergency fund first, then secure term life, health, and malpractice insurance, then set a budget, then maximise tax-saving instruments (80C, 80CCD(1B), 80D), and finally invest systematically through SIPs and NPS. Reordering these steps in the early career phase creates gaps that are expensive to fix later.

What are the 5 P's of physician financial planning?

The 5 P's cover: Planning (goal-based roadmap), Protection (life, health, disability, and malpractice insurance), Portfolio (structured allocation across asset classes), Practice finances (cash flow, tax structuring, and expense tracking for private practitioners), and Philanthropy/Legacy (estate planning, nominations, and wealth transfer).

How should physicians manage education loan debt in India?

Use the moratorium period to build a 4–6 month emergency fund, then follow the Debt Avalanche method (highest-interest loans first) once repayment begins. If your loan rate is below 8–9%, starting small parallel SIPs often makes more financial sense than waiting for full repayment — early compounding typically outweighs the interest saved through aggressive prepayment.

When should a physician start investing for retirement in India?

As early as residency, even if it's ₹1,000–₹2,000/month in a SIP. The compounding horizon for a 28-year-old physician extends over 30+ years, and small amounts invested consistently over that period grow to significantly larger sums than larger amounts started a decade later. Waiting until the loan is cleared and income is high is the most common and most expensive retirement planning mistake physicians make.