The wrong account choice can trigger unexpected tax deductions, FEMA non-compliance under Section 13 of the Foreign Exchange Management Act (which allows penalties up to three times the sum involved), or repatriation restrictions at the worst possible moment. This guide breaks down exactly how NRE and NRO accounts work, where they differ, and how to decide which structure — or combination — fits your financial situation.

Key Takeaways

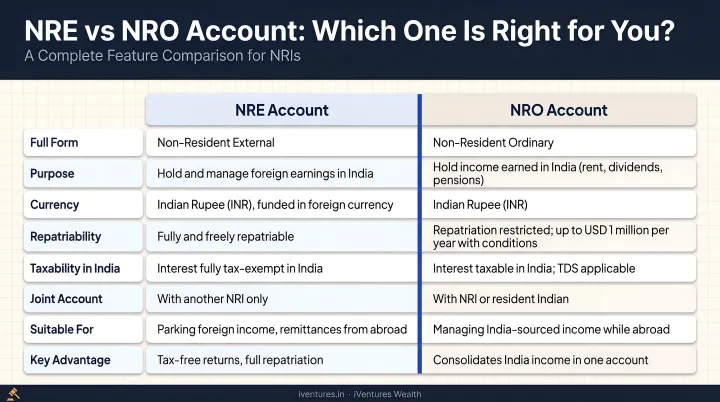

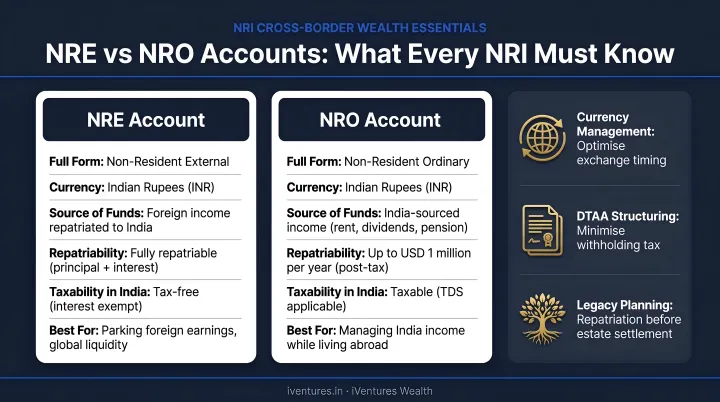

- NRE accounts hold foreign earnings converted to INR — interest is tax-free in India and funds are freely repatriable

- NRO accounts hold India-sourced income (rent, dividends, pensions) — interest attracts TDS at 30% plus surcharge and cess absent a DTAA

- Repatriation from NRO is capped at USD 1 million per financial year, with documentation and tax compliance required

- FEMA mandates that NRIs convert existing resident savings accounts to NRO accounts upon change of residential status

- Holding both accounts is permitted and practical — NRE for foreign earnings, NRO for Indian income

NRE vs NRO: Quick Comparison

| Feature | NRE Account | NRO Account |

|---|---|---|

| Source of funds | Foreign earnings/remittances only | Indian-source income; also accepts foreign remittances |

| Currency | INR (foreign currency converted on deposit) | INR |

| Interest taxation | Tax-exempt under Section 10(4)(ii) | Taxable; TDS at 30% + surcharge/cess (standard rate) |

| Repatriation | Fully repatriable, no limit | Up to USD 1 million per financial year, post-tax |

| Joint account | With another NRI or resident relative (former or survivor basis) | With any resident Indian |

| DTAA benefit | Not applicable (already tax-free) | Applicable with Tax Residency Certificate |

| Best for | Overseas salary, foreign business income | Rent, dividends, pension, property sale proceeds |

Both accounts are rupee-denominated and support the same core banking functions: internet banking, fund transfers, deposits, and withdrawals. For NRIs managing income from multiple sources, the real difference lies in how each account handles taxation and repatriation — factors that directly shape how wealth is structured and moved across borders.

What Is an NRE Account?

An NRE (Non-Resident External) account is a rupee-denominated bank account that allows NRIs to deposit and manage their foreign earnings in India. When you remit foreign currency, the bank converts it to INR at the prevailing exchange rate and credits your account.

The Tax-Free Advantage

The standout feature is the income tax exemption. As confirmed by the Income Tax Department, interest earned on NRE accounts is fully exempt from Indian income tax under Section 10(4)(ii) of the Income Tax Act, 1961 — provided the account holder qualifies as a person resident outside India under FEMA. Note that the Wealth-tax Act was abolished from 1 April 2016, so wealth tax is no longer a consideration for any account type.

Both principal and interest are fully repatriable — you can transfer funds back to your country of residence at any time, without restrictions on amount or documentation.

Use Cases of an NRE Account

The NRE account suits NRIs who earn abroad and want to remit money to India for savings, investments, or family support — while retaining complete freedom to move those funds back overseas.

Practical uses include:

- Park foreign salary in Indian fixed deposits or savings accounts at competitive, tax-free interest rates

- Link directly to mutual fund folios for SIPs or lump-sum investments

- Trade equities on a repatriable basis via the Portfolio Investment Scheme (PIS), routed through a designated bank

- Send funds for family support, with the flexibility to repatriate if your circumstances change

Eligibility: NRIs, Persons of Indian Origin (PIOs), and Overseas Citizens of India (OCIs) can open NRE accounts. A resident Indian can be added as a joint holder on a former or survivor basis, or appointed as a Power of Attorney.

What Is an NRO Account?

An NRO (Non-Resident Ordinary) account is a rupee-denominated account designed for NRIs to receive and manage income earned within India. Rental income, dividends from Indian stocks, pension payments, insurance proceeds, and proceeds from the sale of Indian property — all of these belong in an NRO account.

Tax Treatment and DTAA Planning

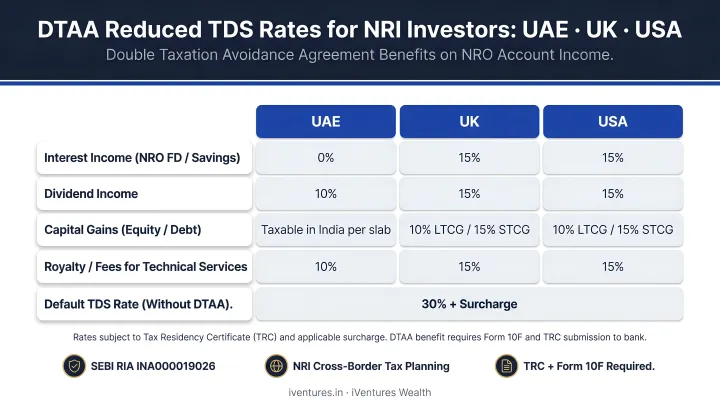

Interest earned in an NRO account is subject to Indian income tax. Under Section 195, the standard TDS rate for non-residents is 30% plus applicable surcharge and cess where no tax treaty applies.

However, NRIs residing in countries that have a Double Taxation Avoidance Agreement (DTAA) with India may be eligible for reduced withholding rates. For example:

- UAE: Generally 12.5% for individual interest income under the treaty

- UK: 15% of gross interest under Article 12

- USA: Generally 15% for individual interest income under Article 11

To claim these rates, you'll need a valid Tax Residency Certificate (TRC) and potentially Form 10F and other bank declarations. The reduced rate is not automatic — documentation must be submitted and the bank must process it accordingly.

For repatriation of NRO funds, Form 15CA and Form 15CB (where applicable) are required under Rule 37BB of the Income Tax Rules.

Use Cases of an NRO Account

- Receiving rental income from Indian properties

- Collecting dividends from Indian stocks or mutual funds

- Managing pension or annuity payments from Indian sources

- Holding proceeds from the sale of Indian real estate or assets

- Continuing to receive Indian income after moving abroad

Two practical aspects of NRO accounts that often catch NRIs off-guard:

- Joint holding: An NRO account can be held jointly with any resident Indian — not limited to close relatives — making it convenient for NRIs co-managing finances with family in India.

- Mandatory redesignation: Under RBI's Master Circular on NRO Accounts, a resident savings account must be redesignated as an NRO account once the holder moves abroad for employment, business, or any purpose indicating long-term non-resident status.

Continuing to operate a resident savings account after becoming an NRI is a FEMA contravention. Penalties under Section 13 can reach up to three times the amount involved, or ₹2 lakh where the sum isn't quantifiable, plus ₹5,000 per day as a continuing penalty.

NRE vs NRO: Which Account Is Right for You?

The decision comes down to one principle: where was the income earned?

- Money earned outside India → NRE account

- Money earned inside India → NRO account

That single rule resolves most of the confusion.

Situational Guidance

Choose NRE if you want to:

- Keep interest income tax-free in India

- Retain full repatriation rights with no annual cap

- Invest in Indian markets using foreign salary or business income

- Link investments to mutual funds, PMS, or equity trading on a repatriable basis

Choose NRO if you need to:

- Receive rent, dividends, pension, or property sale proceeds compliantly

- Co-manage accounts with resident family members

- Continue managing India-sourced income after relocating abroad

- Hold redesignated resident account balances

The Case for Holding Both

Many NRIs with diversified income benefit from maintaining both accounts simultaneously. Consider a UAE-based executive who earns a foreign salary and also owns two rental properties in Delhi — a profile iVentures Wealth works with regularly. Their overseas income flows into an NRE account (tax-free, fully repatriable), while rental income credits to an NRO account (taxable, managed with DTAA documentation to reduce TDS exposure). This keeps fund sources clearly separated — compliant, documented, and straightforward to audit.

Transfers from NRO to NRE are permitted within the USD 1 million annual facility, but only after applicable taxes have been paid and proper documentation has been submitted.

The Investment Dimension

That repatriation flexibility directly shapes investment decisions. For NRIs investing in Indian equity markets, NRE-linked investments are generally preferred — funds are tax-free and fully repatriable. However, dividends or capital gains from Indian investments may still need to flow into an NRO account, depending on the investment structure. Secondary market equity trading also requires PIS compliance before linking any account.

For NRIs managing significant Indian assets or complex income structures, getting this right means holding fluency in both Indian tax law and FEMA regulations — simultaneously. That's where a SEBI-registered wealth adviser adds practical value.

iVentures Wealth (SEBI RIA INA000019026) specialises in NRI and OCI cross-border wealth management — from account structuring and DTAA optimisation to consolidated reporting across NRE and NRO-linked portfolios. Advisory services are available to NRIs and OCIs with investable assets of ₹5 crore or more.

Conclusion

NRE and NRO accounts are not competing options. They serve distinct purposes determined by where your income originates — one handles foreign earnings with tax-free, freely repatriable convenience; the other manages Indian-sourced income within a compliant, documented framework.

Getting the structure right protects you from unnecessary tax exposure, repatriation delays, FEMA penalties, and compliance gaps. Account structure, though, is just the foundation. For NRIs building wealth across borders, the real opportunity is using these accounts as a gateway to tax-efficient investment in India — and that requires advice shaped around your specific income profile, residency status, and where you want to be financially in ten years.

Frequently Asked Questions

What is the main difference between an NRE and NRO account?

NRE accounts hold foreign earnings in India: interest is fully tax-free and funds are freely repatriable. NRO accounts manage India-sourced income (rent, dividends, pension), where interest is taxable and repatriation is capped at USD 1 million per financial year.

Which account is better, NRO or NRE?

Neither is universally better — the right choice depends on the source of income. NRE is better for foreign earnings with tax-free and full repatriation benefits; NRO is better for India-sourced income. Most NRIs with income from both sources hold both accounts simultaneously.

Is NRE or NRO account interest tax-free?

NRE account interest is fully exempt from Indian income tax under Section 10(4)(ii). NRO account interest is taxable at 30% TDS (plus surcharge and cess), though DTAA benefits can lower the effective rate with proper documentation.

Can I have both an NRE and NRO account at the same time?

Yes. The RBI framework permits eligible NRIs, PIOs, and OCIs to hold both account types simultaneously. This is common practice, allowing you to channel foreign earnings through NRE and India-sourced income through NRO within a compliant structure.

Can I transfer money from my NRO account to my NRE account?

Yes, but only within the USD 1 million annual repatriation limit. Applicable Indian taxes must be settled first, and Forms 15CA/15CB (where required) must be submitted before the transfer proceeds.

What happens to my regular savings account when I become an NRI?

Under FEMA, NRIs cannot continue operating a regular resident savings account. It must be redesignated as an NRO account upon change of residential status. Continuing to operate it as a resident account is a FEMA contravention and can attract significant penalties under Section 13.