This guide covers what PMS is, how it differs from mutual funds, the different types available, key benefits and real risks, SEBI regulations, and what to look for in a provider who genuinely acts in your interest.

Key Takeaways

- PMS is SEBI-regulated: a professional manages your portfolio while you retain direct ownership of all securities

- Minimum investment is ₹50 lakh, making PMS a product for HNIs and UHNIs

- Three mandate types — discretionary, non-discretionary, and advisory — give investors different levels of control

- Fees are higher than mutual funds; always demand the all-in cost schedule before committing

- Choosing a conflict-free, fiduciary advisor to guide PMS selection is as important as the PMS choice itself

What Is Portfolio Management Services (PMS)?

PMS is a professional investment service where a SEBI-registered portfolio manager manages your portfolio of equities, debt, and other securities. The manager operates under the SEBI Portfolio Managers Regulations, 2020, and tailors every decision to your financial goals, risk tolerance, and investment horizon.

How It Differs from Mutual Funds

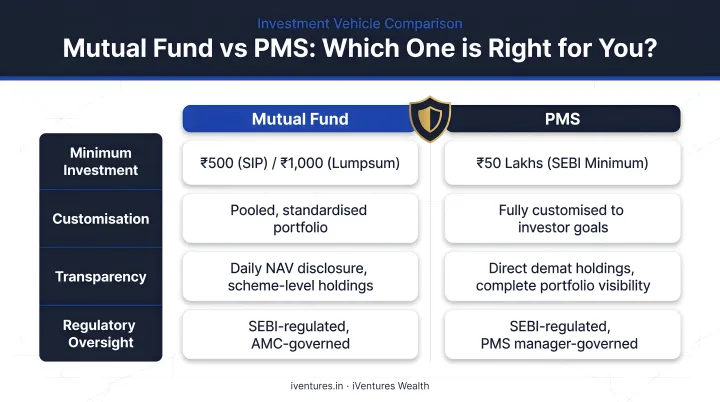

In a mutual fund, your money is pooled with thousands of other investors and managed under a single standardised strategy. In PMS, you retain **direct ownership of the underlying securities** in your own demat account. Nothing is pooled. The portfolio is built specifically for you.

| Mutual Fund | PMS | |

|---|---|---|

| Ownership | Units in a pooled fund | Direct securities in your demat account |

| Customisation | Standardised strategy | Tailored to your goals, tax position, liquidity needs |

| Minimum investment | As low as ₹500 (SIP) | ₹50 lakh (SEBI-mandated) |

| Sector/stock exclusions | Not possible | Can exclude sectors or stocks |

As the SEBI Investor portal confirms, PMS provides customised investment solutions with direct asset ownership in the investor's name.

How It Works in Practice

That direct ownership model shapes how PMS actually operates. Once you invest, you grant authority to the portfolio manager — either fully or within defined parameters. Their dedicated research team makes investment decisions executed directly in your demat account, and you receive regular reporting on holdings, performance, and activity.

As of April 30, 2026, SEBI reported 498 portfolio managers managing total AUM of ₹42,36,467 crore — though a large portion of this reflects institutional mandates from entities like EPFO. The HNI discretionary equity PMS segment is smaller but growing steadily.

Who PMS Is Designed For

PMS is built for:

- High-net-worth and ultra-high-net-worth individuals

- Family offices managing multigenerational wealth

- NRIs and OCIs with substantial India-linked portfolios

- Institutional investors and corporates

- Entrepreneurs and CXOs with concentrated wealth needing professional diversification

SEBI mandates a minimum investment of ₹50 lakh per client, which places PMS firmly outside the retail category and into structured, regulated wealth management.

Types of Portfolio Management Services

PMS mandates fall into two dimensions: the degree of manager autonomy, and the investment style. Both affect your day-to-day involvement and how the portfolio is managed.

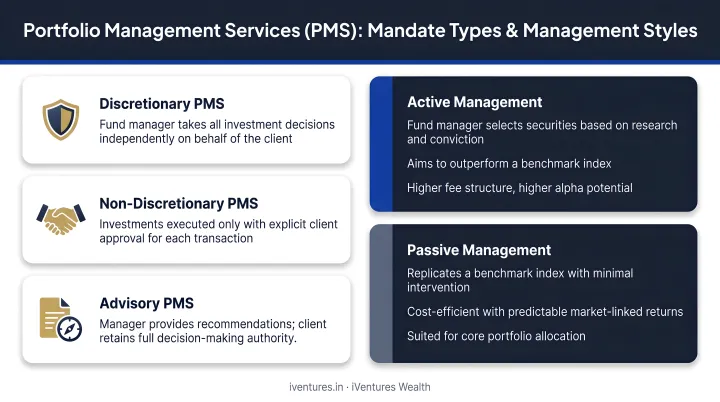

Discretionary PMS

The portfolio manager has full authority to buy, sell, and rebalance without seeking your approval on each transaction. This is the most common structure — SEBI data for April 2026 shows discretionary PMS accounts for roughly 84.9% of total reported PMS AUM, with 2,07,989 clients.

Best suited for: investors who want complete professional management with minimal day-to-day involvement.

Non-Discretionary PMS

The manager provides detailed recommendations, but every decision requires your approval before execution. You stay informed and in control; the manager does the research and advises.

Best suited for: investors who want expert guidance but prefer to retain final decision-making authority.

Advisory PMS

The manager's role is purely consultative — strategy and research input only. You execute all transactions yourself. Advisory PMS represented about 7.2% of total AUM in April 2026, with 1,216 clients.

Best suited for: experienced investors who can execute trades independently but value professional research and strategic input.

Active vs. Passive Management

Beyond the mandate type, how a manager approaches stock selection shapes both cost and return potential.

- Active PMS: The manager selects securities, attempts to outperform benchmarks, and adjusts the portfolio as conditions change. Expect higher fees and greater dependence on the manager's judgment.

- Passive PMS: The portfolio tracks an index, resulting in lower turnover and lower fees, with returns that mirror the market rather than beat it.

Key Benefits of Portfolio Management Services

Expert, Research-Backed Management

PMS gives you access to a dedicated portfolio manager and research analysts who track macroeconomic conditions, sector dynamics, and company fundamentals — making decisions that most individuals simply can't replicate while managing careers and businesses. That discipline — grounded in process rather than instinct — tends to show its value most clearly when markets turn volatile.

Fully Customised Investment Strategy

Unlike mutual funds, a PMS portfolio is built around your specific situation:

- Financial goals and investment timeline

- Risk appetite and liquidity requirements

- Tax position and income needs

- Personal preferences (for example, avoiding specific sectors)

The strategy evolves as your circumstances change — a liquidity event, a business exit, a change in income. Standardised fund products can't adjust to those shifts; a PMS mandate can.

Ongoing Monitoring and Proactive Rebalancing

A dedicated manager continuously tracks every position, monitors market conditions, and rebalances proactively — rather than waiting for you to notice something has drifted. For investors holding complex, multi-asset portfolios, this ongoing oversight has real value.

Transparency and Direct Ownership

Because you hold securities directly in your demat account, you can see exactly what you own at any point. This is meaningfully different from mutual funds, where you hold units of a pooled fund with no visibility into the underlying portfolio.

Direct ownership also enables more accurate consolidated reporting — particularly useful for family offices and investors tracking wealth across multiple entities.

A Note on Performance

PMS Bazaar data from May 2024 showed average 5-year equity PMS returns of 18.99% versus 15.27% for Nifty 50 TRI and 17.38% for BSE 500 TRI. That's encouraging — but not universal. Mint's analysis found only 30% of small-cap PMS funds in their sample beat the five-year small-cap mutual fund average. Performance is a due-diligence question, not a guaranteed benefit.

SEBI Regulations and Eligibility for PMS in India

All PMS providers in India must register with SEBI under the SEBI Portfolio Managers Regulations, 2020 (last amended August 18, 2023). The framework mandates custody separation, mandatory disclosures, and a ban on guaranteed returns — giving investors clear, enforceable safeguards before they commit capital.

Key SEBI Requirements

| Requirement | Detail |

|---|---|

| Registration | Mandatory SEBI registration; verifiable on SEBI's registered portfolio managers page |

| Minimum investment | ₹50 lakh per client (applies to new investments and top-ups from January 21, 2020) |

| Net worth | Portfolio manager must maintain minimum net worth of ₹5 crore |

| Independent custodian | Client assets must be held by an independent custodian, separate from the provider's own funds |

| Disclosure document | Must be provided before any agreement is signed, covering fees, risks, performance, related-party transactions, and three years of audited financials |

| Guaranteed returns | Prohibited — portfolio managers cannot offer assured or indicative returns |

Recent Regulatory Updates

SEBI has tightened PMS oversight significantly since 2022. Key changes include:

- December 2022: New performance benchmarking and reporting standards

- August 2023: Mandatory audit of firm-level performance data

- May 2024: Streamlined digital onboarding and enhanced disclosure requirements

- June 2024: Master circular consolidating all portfolio manager regulations

What to Verify Before Investing

Before committing capital, confirm that the provider:

- Appears on SEBI's registered portfolio managers list

- Provides a complete disclosure document covering fees, strategy, risks, and track record

- Can clearly explain who holds custody of your assets

- Has a designated compliance officer

These checks take under 30 minutes and can prevent costly mistakes — particularly when evaluating providers with similar-sounding strategies or fee structures.

Risks and Considerations Before Investing in PMS

Concentration Risk

PMS portfolios are typically more concentrated than mutual funds — most hold somewhere between 15 and 30 stocks, versus 40 or more in a diversified fund. Concentration can drive outperformance in favourable conditions, but it also amplifies volatility when positions move against you. That makes PMS best suited for investors with a long-term horizon of at least 3–5 years who can ride through short-term drawdowns without being forced to exit.

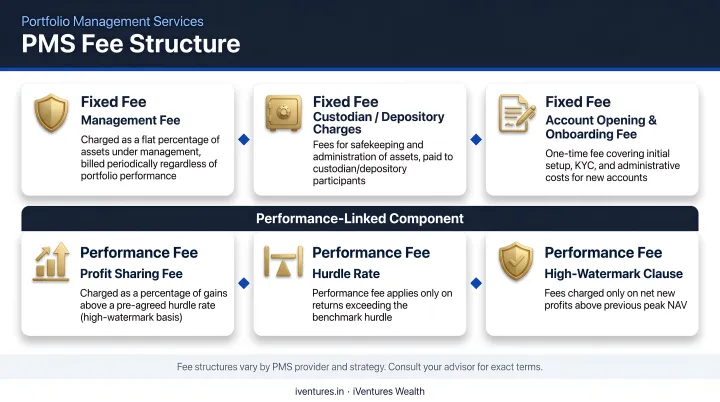

Costs and Fee Structures

PMS fees are higher than mutual funds and more variable. The typical structure:

- Fixed management fee: Commonly 1.5%–2.5% of AUM annually (PMS Bazaar cites a broader range of 0.25%–2.5%)

- Performance fee: Charged above a pre-agreed hurdle rate — for example, if the hurdle is 12% and the split is 80:20, gains above 12% are shared 80% to the investor and 20% to the provider

- Additional costs: Brokerage, custody charges, and applicable taxes

Always ask for the all-in fee schedule — not just the headline management fee. Total costs can look very different once all components are included.

Tax Drag

Fees are only part of the cost picture. Unlike mutual funds — where you're generally taxed only on redemption — PMS trades occur in your demat account and can trigger capital gains tax on each transaction. Frequent rebalancing in an active PMS strategy can create real tax drag over time. Ask any provider specifically how they approach tax-aware portfolio management.

Manager Dependency

PMS performance is closely tied to the individual portfolio manager's judgment and experience. If a key manager departs, the impact on your portfolio is more direct than with a large fund house. When evaluating providers:

- Assess whether the investment process is process-driven or personality-driven

- Review performance across multiple market cycles, not just recent bull runs

- Ask about team stability and succession arrangements

How to Choose the Right PMS Provider

Evaluate Credentials, Track Record, and Investment Philosophy

Start with the basics:

- Confirm SEBI registration on the official portal

- Look for professionally qualified teams — CFA charterholders indicate a rigorous analytical standard

- Ask for verified performance data across both bull and bear markets

- Assess whether the investment philosophy is clearly articulated and consistently followed, or shifts with market trends

Be cautious of providers who are primarily distributors of products rather than genuine advisors.

Prioritize Fiduciary Alignment

This is where many investors make their costliest mistake. A provider who earns distribution fees or trail commissions from the PMS products they recommend has an inherent conflict of interest — regardless of how they frame their advice.

A SEBI-registered Investment Adviser (RIA) is legally required to act in your interest, not earn product commissions. Asking whether your advisor holds an RIA registration — in addition to any other registrations — is one of the most important questions you can ask.

Firms like iVentures Wealth (SEBI RIA registration INA000019026) operate on exactly this model — fee-only, open-architecture, with no commissions from any PMS provider. With 20+ years of experience and ₹1,200 Cr+ in AUM, iVentures evaluates PMS options from the full SEBI-regulated universe. Each recommendation is assessed on:

- Performance track records across market cycles

- Risk-adjusted return metrics (Sharpe ratio, Sortino ratio)

- Fee structures and total cost of ownership

- Investment philosophy consistency over time

Demand Transparency in Reporting and Fees

A credible PMS provider should offer:

- Clear, regular performance reports with benchmark comparisons

- Full fee disclosure before you sign anything

- Direct access to your portfolio manager for questions

Ask for a sample report and the complete disclosure document before committing. If a provider is reluctant to share either, that's your answer.

Frequently Asked Questions

What do portfolio management services do?

PMS providers professionally manage an individual investor's portfolio of stocks and other securities, making research-backed investment decisions aligned with the investor's financial goals, risk profile, and time horizon. Unlike mutual funds, the investor retains direct ownership of all securities in their own demat account.

How much do portfolio management services charge?

PMS fees typically include a fixed management fee ranging from 1.5% to 2.5% of AUM annually, and often a performance fee charged above a pre-agreed hurdle rate. Additional costs include brokerage and custody charges. Always request a complete all-in fee schedule before investing.

What is the minimum investment required for PMS in India?

SEBI mandates a minimum investment of ₹50 lakh for all PMS clients in India. This threshold applies to all providers and reflects the product's complexity, higher fee structure, and concentration risk.

What is the difference between PMS and mutual funds?

The two most important differences come down to ownership and customisation. In PMS, you directly own the underlying securities in your own demat account; mutual fund investors hold units of a pooled fund. PMS also offers a fully customised portfolio built around your specific situation, while mutual funds follow a standardised strategy for all unitholders.

Is PMS regulated by SEBI in India?

Yes. All PMS providers must be registered with SEBI under the SEBI Portfolio Managers Regulations, 2020. SEBI mandates minimum investment thresholds, disclosure requirements, independent custodian arrangements, and regular compliance reporting.

Who should consider investing in PMS?

PMS suits HNIs and UHNIs who meet the ₹50 lakh minimum and have a long-term horizon of 3–5 years or more. It works best for investors who want a personalised, professionally managed portfolio but don't have the time or expertise to navigate complex, multi-asset strategies on their own.