Portfolio Management Services (PMS) sits at the centre of this shift. Yet despite growing adoption, PMS is frequently misunderstood — conflated with mutual funds, or evaluated purely on return figures rather than the full range of structural and strategic advantages it offers.

This article breaks down what PMS actually delivers in practice: from how portfolios are built and monitored, to how tax efficiency, risk management, and transparency work in an individually managed mandate.

Key Takeaways

- PMS is a SEBI-regulated mandate with a statutory ₹50 lakh minimum, governed by the SEBI Portfolio Managers Regulations, 2020

- Investors hold securities directly in their own demat account — not units in a pooled fund — giving full ownership and transparency

- Each portfolio is built around the investor's specific goals, risk tolerance, and time horizon — not a one-size-fits-all strategy

- Active rebalancing and tax-aware management improve after-tax returns, especially for investors in higher brackets

- SEBI-mandated qualification and reporting standards ensure accountability and investor protection across all registered managers

What Are Portfolio Management Services?

PMS is a contract-based, individually managed investment service. Under SEBI's regulatory framework, a portfolio manager is defined as a body corporate that, under contract, manages or administers a client's securities or funds — covering equities, fixed income, and other regulated asset classes.

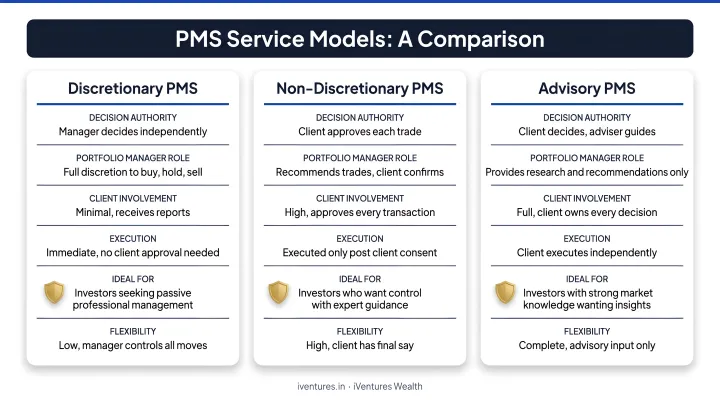

Three service models exist under SEBI's framework:

- Discretionary PMS — the manager independently makes investment decisions within the agreed mandate

- Non-discretionary PMS — the manager executes trades based on client directions

- Advisory PMS — the manager provides recommendations without execution authority

The key structural distinction from mutual funds: investors in PMS hold securities directly in their own demat account. There are no pooled units and no shared exposure with other investors.

SEBI mandates a minimum investment of ₹50 lakh per client — a threshold that positions PMS firmly for investors with substantial capital and defined wealth management objectives.

As of April 30, 2026, SEBI's statistics show 498 registered portfolio managers, 2,07,989 discretionary clients, and a stated total AUM of ₹42,36,467 crore across all PMS reporting categories.

Unlike a one-time investment decision, PMS is an ongoing relationship — one that adapts as markets shift, your financial situation changes, and your long-term goals come into clearer focus.

Key Benefits of Portfolio Management Services

The benefits below are not abstract. Each one translates into a measurable difference in how wealth is structured, protected, and grown over time.

Professional Expertise and Research-Driven Decision-Making

PMS gives investors access to qualified fund managers and dedicated research teams conducting continuous fundamental analysis, tracking macroeconomic indicators, and monitoring sector and company-specific developments. This depth of coverage is rarely replicable by an individual investor managing their own portfolio alongside professional and personal commitments.

SEBI mandates strict qualification standards for portfolio managers. Principal officers must hold professional qualifications in finance, law, accountancy, or business management, with a minimum of five years of securities market experience, and pass the NISM-Series-XXI-B Portfolio Managers Certification Examination.

These requirements ensure investors are working with credentialed professionals, not generalist advisors.

Professional managers act on research signals rather than market noise. During periods of volatility, they reposition defensively and structure recovery allocations based on analysis, rather than waiting for a loss to prompt action.

Behaviour plays a measurable role here. Morningstar India reported a negative investor return gap of 2.68% per year over a three-year period: investors in well-performing funds consistently underperformed the funds themselves due to poorly timed entry and exit decisions. Structured, process-driven management removes much of that emotional drag.

For clients working with iVentures Wealth, PMS evaluation and monitoring is led by the firm's CFA-led research team, which analyses risk-adjusted return ratios including the Sharpe and Sortino ratios — going beyond absolute returns to assess whether a PMS strategy is genuinely prudent and aligned with each client's specific risk profile.

Customised Portfolios Built Around Individual Goals

In a mutual fund, every investor holds identical underlying assets regardless of their age, tax situation, income sources, or investment horizon. PMS works differently. The portfolio is built specifically for the individual investor — shaped by:

- Financial goals (retirement, wealth transfer, capital preservation, liquidity needs)

- Risk appetite and time horizon

- Tax bracket and existing holdings

- Personal preferences, including any sector or industry exclusions

Customisation extends to position sizing, sector exposure, and geographic diversification. The result is a portfolio that reflects the investor's actual financial identity, not a generalised allocation model.

This matters most when financial complexity is high. A 45-year-old entrepreneur with a 10-year growth horizon, concentrated promoter equity, and business income structured differently from employment income has fundamentally different needs from a 62-year-old professional preserving capital ahead of retirement. Generic strategies cannot capture these distinctions — PMS is designed precisely for that gap.

Investors transitioning from direct equity management or mutual funds often find PMS most useful when they want greater customisation and dedicated research without the full administrative burden of self-management.

Active Risk Management, Portfolio Rebalancing, and Tax Efficiency

PMS is not a set-and-forget arrangement. Portfolio managers continuously monitor holdings, track performance against benchmarks, and rebalance when allocations drift from their targets — preventing unintended concentration risk from building up silently over time.

What ongoing management includes:

- Rebalancing when sector or asset weightings move outside target ranges

- Monitoring individual holdings against original investment thesis

- Adjusting positioning when macroeconomic or company-specific conditions change materially

- Reviewing portfolio alignment when the investor's personal circumstances shift

Tax efficiency is built into the management process from the outset. Because investors hold securities directly in their own demat account, tax liability is recognised at the individual level. Portfolio managers can time buy and sell decisions with the investor's specific tax situation in mind, structuring exits to optimise short-term versus long-term capital gains treatment and identifying tax-loss harvesting opportunities to offset gains.

For investors in higher tax brackets — which includes most HNI and UHNI investors — these decisions compound significantly over a multi-year investment horizon. The difference between a tax-aware and tax-unaware exit strategy can be material, even before considering the underlying investment returns.

Transparency and Reporting

SEBI requires portfolio managers to furnish client reports at intervals not exceeding three months, covering portfolio composition, transactions, expenses, and risks. Investors also maintain direct demat account visibility at all times: no pooled reporting, no opacity, no delays in understanding what they actually own.

iVentures Wealth's consolidated reporting integrates PMS holdings alongside all other asset classes — mutual funds, bonds, equities, AIFs — so clients see current value, daily changes, absolute gains, and CAGR in a single dashboard through the firm's Wealth Monitor App.

Who Should Consider Portfolio Management Services?

PMS is not suitable for all investors. The structure is designed for a specific profile:

- HNIs and UHNIs with ₹50 lakh or more available for investment, who want professional management of a significant capital base

- Founders and entrepreneurs managing post-liquidity wealth or concentrated equity positions that need systematic diversification

- CXOs and professionals with high income, limited time to manage their own portfolio, and financial complexity that warrants an individualised strategy

- NRI and OCI investors with cross-jurisdiction tax considerations, FEMA compliance requirements, and Indian securities market exposure

- Family offices seeking a consolidated, professionally managed approach across multiple investment mandates

NRI investors should confirm eligibility with their PMS provider, as participation in Indian securities markets involves NRE/NRO account structures, PIS permissions, and applicable SEBI and RBI rules.

Investors best positioned to benefit share a few common traits:

- A long-term horizon of at least three years

- A preference for transparency and active engagement with their portfolio manager

- Financial complexity that a customised strategy addresses better than a one-size-fits-all approach

What Happens Without Professional Portfolio Management?

Managing significant wealth without a structured framework carries risks that are easy to underestimate when markets are performing well, and costly to discover when they are not.

Common consequences of self-managed portfolios at scale:

- Portfolio drift — allocations shift away from intended targets, creating unintended concentration or exposure mismatches

- Emotional decision-making — during downturns, investors frequently exit positions at unfavourable prices, locking in losses that process discipline could have prevented

- Silent concentration risk — portfolios held by founders or executives often develop heavy sector or single-stock exposure without any systematic diversification applied

- Tax drag — without proactive planning, investors realise avoidable short-term gains or miss harvesting opportunities, compressing net returns over time

- Missed research depth — few individual investors have the analytical resources to monitor a complex portfolio in real time

None of these risks are exclusive to unsophisticated investors. They are structural problems that surface when the demands of managing significant wealth outpace the time, tools, or expertise available.

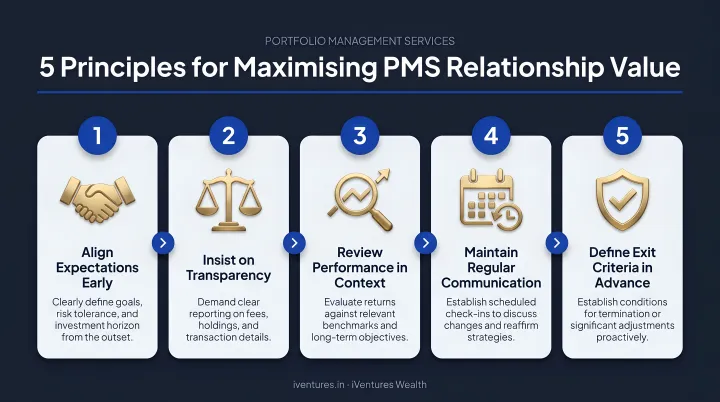

How to Get the Most from Your PMS Relationship

PMS delivers its full value when treated as a long-term partnership rather than a transactional arrangement. A few practical principles:

- Set clear objectives upfront. Document return expectations, liquidity requirements, investment restrictions, and tax considerations before the mandate begins — not mid-way through.

- Communicate financial changes promptly. Career transitions, business liquidity events, inheritance, or shifts in income structure should trigger a portfolio review conversation, not be handled in isolation.

- Participate actively in periodic reviews. Quarterly check-ins are a baseline; investors who engage with these conversations consistently extract more value from the advisory relationship.

- Choose a provider that operates on a fiduciary basis. A SEBI-registered advisor without distribution incentives recommends PMS strategies based on suitability, not product economics.

- Prioritize consolidated reporting. Viewing PMS holdings alongside all other assets gives a complete picture of portfolio risk and returns, rather than evaluating each product in isolation.

Working with a fee-only RIA like iVentures Wealth means recommendations are driven by client fit and performance criteria — not commission structures. That distinction matters most when selecting between PMS strategies where product economics can otherwise skew advice.

Frequently Asked Questions

What are the advantages of Portfolio Management Services?

PMS offers professional expertise, individually customised portfolios, active risk management, tax-efficient structuring, direct securities ownership, and SEBI-regulated oversight. This combination gives investors a more structured, transparent experience than self-directed investing or pooled fund alternatives.

What is the minimum investment required for PMS in India?

SEBI mandates a minimum investment of ₹50 lakh per investor for PMS. This keeps the product aligned with investors who have sufficient capital for individualised portfolio construction rather than pooled fund structures.

How is PMS different from mutual funds?

In PMS, investors hold individual securities directly in their own demat account rather than units in a pooled fund. This enables greater customisation, direct ownership visibility, and more personalised tax management — none of which are available in standard mutual fund structures where all investors hold identical underlying assets.

Is PMS suitable for NRI investors?

NRIs and OCIs can access Indian securities markets through PMS, subject to NRE/NRO account requirements, PIS permissions for repatriable trades, and applicable FEMA and SEBI rules. Confirm your eligibility and account structure with your PMS provider and a cross-border tax advisor before investing.

How do portfolio managers help with tax efficiency?

Managers time investment exits to optimise short-term versus long-term capital gains treatment, identify tax-loss harvesting opportunities to offset realised gains, and structure the portfolio with the client's individual tax bracket in mind. Because securities are held directly by the investor, these decisions are applied at the individual level rather than being averaged across a pooled fund.

What should I look for when choosing a PMS provider?

Key criteria include: SEBI registration and a current disclosure document, the investment team's qualifications and experience, a demonstrable performance track record evaluated on risk-adjusted metrics, a conflict-free fee structure with no undisclosed distribution income, transparent and regular client reporting, and the quality of ongoing communication between the portfolio manager and client.