Investing in India as a US-based NRI is entirely legal and accessible, but it requires navigating two regulatory systems simultaneously: India's SEBI/RBI/FEMA framework and US obligations under FATCA, FBAR, and IRS reporting rules. Getting either side wrong is expensive.

This guide covers exactly what you need: who qualifies as an NRI, the step-by-step account setup process, the best investment options available, how Indian capital gains taxes interact with US reporting requirements, and the mistakes that consistently cost NRIs money.

Key Takeaways

- Open an NRE or NRO bank account and a PINS-enabled Demat/trading account before investing in Indian equities

- Choose between stocks, mutual funds, FDs, REITs, bonds, NPS, and PMS — each carries distinct repatriation rules and tax treatment

- US-based NRIs face FATCA/CRS restrictions that block access to several major Indian AMCs

- Indian capital gains are taxed in India, but the India-USA DTAA prevents double taxation — active filing in both countries is required

- NRIs are barred from intraday trading, currency derivatives, and commodity derivatives — only delivery-based equity trades are permitted

How to Start Investing in India from the USA: Step-by-Step

Step 1: Confirm Your NRI Status and Get a PAN Card

Under FEMA, an NRI is an Indian citizen residing outside India. The Income Tax Act defines residency separately: you're a resident if you spend 182 days or more in India in a financial year, or 60+ days in the current year plus 365+ days across the preceding four years.

Test your status every financial year. It determines which accounts you can open and how your investment income is taxed.

A PAN card is mandatory for all investment transactions in India. US-based NRIs can apply online through Protean (NSDL) or UTIITSL. Indian citizens use Form 49A; OCI/foreign nationals use Form 49AA. No physical presence in India is required.

NRI vs. OCI at a glance:

- NRIs — Indian citizens residing abroad

- OCIs — persons of Indian origin holding foreign citizenship

Both can invest in most Indian instruments under similar rules, but documentation requirements differ between the two categories.

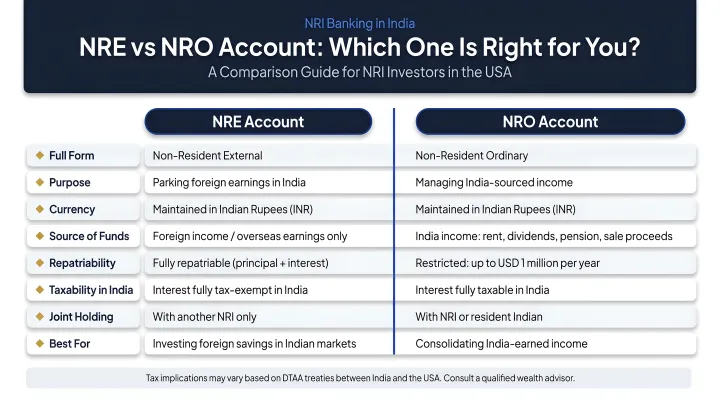

Step 2: Open an NRE or NRO Bank Account

These are the two primary account types, and choosing the wrong one for the wrong purpose creates repatriation problems later.

| Feature | NRE Account | NRO Account |

|---|---|---|

| Funds source | Foreign-earned income | India-sourced income (rent, dividends) |

| Tax in India | Tax-free | Taxable |

| Repatriation | Fully repatriable, no cap | Up to USD 1 million per financial year |

| Best for | Investments you'll bring back to USA | Managing India-based income |

Once you've chosen the right account type, gather these documents to open one:

- Passport and valid US visa/work permit

- US address proof

- PAN card

HDFC Bank, ICICI Bank USA, and SBI all offer NRI account opening with US-specific processes.

Step 3: Set Up a PINS Account for Stock Market Investment

The Portfolio Investment NRI Scheme (PINS) is the RBI-approved route for buying and selling listed shares on NSE and BSE. Key rules:

- Linked exclusively to your NRE account

- Only one designated PINS bank is permitted at a time

- Required for secondary market share trades only; IPOs, mutual funds, ETFs, and bonds are exempt

According to SEBI's NRI investor material, don't over-apply PINS. Mutual fund and IPO investments flow directly through NRE/NRO accounts without a PINS permission letter.

Step 4: Open an NRI Demat and Trading Account

Once your bank issues a PINS permission letter, you can open a Demat account (to hold securities digitally) and a trading account with a SEBI-registered broker.

Important: A resident Demat account cannot be used once you acquire NRI status. Continuing to use one is a FEMA violation.

Maintain separate Demat accounts for repatriable and non-repatriable securities — NSDL rules require this distinction.

Standard documents brokers require:

- Passport copy and overseas address proof

- PAN card

- PINS permission letter

- Recent photograph

- NRE/NRO bank account details

Step 5: Fund the Account and Begin Investing

Transfer funds from the US to your NRE account via wire transfer or remittance platforms. FCNR(B) deposits are another option: held in USD, GBP, EUR, or other freely convertible currencies for tenures of 1–5 years, they are fully repatriable and shield you from INR depreciation.

Once funds are in your NRE/NRO account, you can place delivery-based buy orders through your trading account.

Critical rule: SEBI explicitly prohibits intraday trading and short selling for NRIs. All equity trades must be delivery-based. Currency derivatives and commodity derivatives are also restricted.

Best Investment Options for NRIs in India

No single investment type works for every NRI. Your choices hinge on how much risk you can absorb, how long you plan to stay invested, and whether you'll eventually need to move money back to the USA — each factor points toward a different set of instruments.

Equity Shares and ETFs

NRIs can invest in listed Indian equities through the PINS route and in index ETFs (Nifty 50, Sensex-based) directly through NRE/NRO accounts without PINS.

Nifty Indices data shows a 10-year return of 12.55% for the Nifty 50, while Bajaj AMC cites approximately 12.44% 20-year TRI CAGR based on NSE whitepaper data. These are historical figures, not forward-looking guarantees — but the long-run compounding case for Indian equities is hard to ignore.

Delivery-based trades only. Equity ETFs are permitted; verify currency and commodity derivative restrictions with your broker before investing.

Mutual Funds

NRIs can invest in Indian equity, debt, and hybrid mutual funds through NRE/NRO accounts as lump sums or SIPs.

US-based NRIs face a significant access problem here. Several major AMCs block US persons entirely due to FATCA/CRS compliance costs — HDFC MF Online explicitly states its platform is not available to US persons, and UTI MF's website notes its content is not intended for US investors.

AMCs that do accept US-based NRI investments include:

- PPFAS Mutual Fund

- SBI Mutual Fund

- Nippon India MF

Acceptance can vary by scheme and transaction mode. Always verify directly with the AMC before investing.

A separate concern: Indian mutual fund units may be classified as PFICs (Passive Foreign Investment Companies) under US tax law, triggering punitive tax treatment on redemption. This is covered in the tax section below.

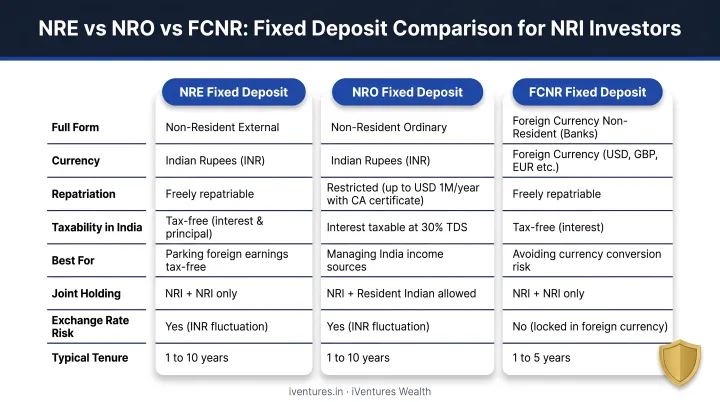

Fixed Deposits: NRE, NRO, and FCNR(B)

Three distinct FD structures, each suited to different needs:

- NRE FD: Tax-free in India, fully repatriable. SBI's current NRE FD rates (effective March 2026) range from 6.05% to 6.45%; HDFC Bank offers up to 6.50% for select tenures. Rates change frequently — verify before committing.

- NRO FD: Interest is taxable in India (TDS at 30% plus surcharge and cess, with DTAA relief possible). Use for India-sourced income only.

- FCNR(B) FD: Held in foreign currency (USD, GBP, EUR, etc.), so no INR depreciation risk. Tenure 1–5 years, fully repatriable.

REITs, Bonds, and PMS

- Government bonds, PSU bonds, NCDs: NRIs can invest per RBI foreign investment circulars. SEBI's NRI material lists government dated securities, PSU bonds, and listed NCDs as accessible routes.

- REITs: Provide commercial real estate exposure without property management. Verify current FEMA non-debt instrument rules for repatriation eligibility before investing.

- Portfolio Management Services (PMS): For NRIs wanting professionally managed equity portfolios, SEBI mandates a minimum ticket size of ₹50 lakh. PMS managers create customized, concentrated portfolios — different in structure from mutual funds. iVentures Wealth provides open-architecture PMS manager selection for NRI/OCI clients, screening across strategies without commission conflicts.

National Pension System (NPS)

NRIs and OCI cardholders can contribute to NPS under the All Citizen Model for retirement planning in India. It's tax-efficient as a long-term vehicle but carries repatriation restrictions on the corpus. Factor this in before committing capital you may need to access or repatriate within a defined timeframe.

Tax and Regulatory Considerations for USA-Based NRIs

For US-based NRIs, investing in India means navigating two tax jurisdictions. The intersection is where most expensive mistakes happen.

Capital Gains Taxation in India

Post-Budget 2024 rates (effective 23 July 2024), per AMFI's tax regime note:

| Asset Type | Holding Period | Tax Rate |

|---|---|---|

| Listed equity (STCG, Section 111A) | Under 12 months | 20% |

| Listed equity (LTCG, Section 112A) | Over 12 months | 12.5% above ₹1.25 lakh |

| Debt mutual funds (acquired after 1 Apr 2023) | Any | Slab rate |

TDS is deducted by AMCs on mutual fund redemptions for NRIs at applicable capital gains rates plus surcharge and 4% health and education cess. NRO FD interest is subject to 30% TDS plus surcharge and cess, with DTAA relief possible.

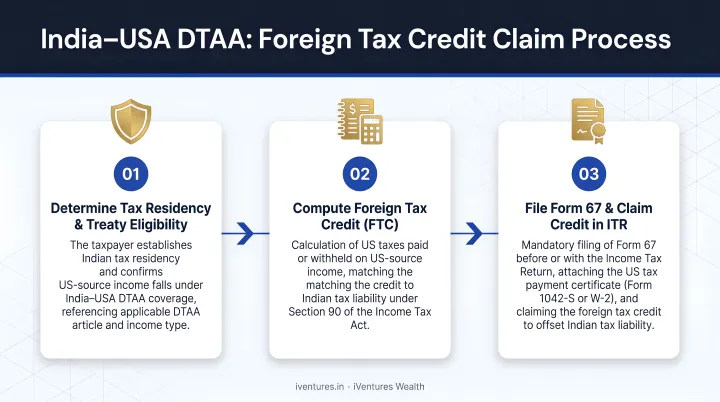

Leveraging the India-USA DTAA

The India-US income tax treaty (signed 12 September 1989) prevents the same income from being taxed twice. Article 13 of the treaty allows both countries to tax capital gains under their domestic law. In practice, India taxes Indian equity gains, and the US may also assess tax on the same gains.

The relief mechanism works in three steps:

- Identify Indian tax paid: Gather TDS certificates and tax computation records for the year

- File IRS Form 1116: Claim a foreign tax credit for taxes already paid in India

- Document everything: The credit does not apply automatically — active filing and supporting records are required

A cross-border tax advisor who understands both Indian and US filing requirements is critical here. iVentures Wealth (SEBI RIA INA000019026) provides DTAA structuring as a core service, helping NRIs plan investment structures that minimize dual-tax exposure before transactions occur.

FATCA, FBAR, and the PFIC Problem

Three US reporting obligations that most NRIs underestimate:

- FBAR (FinCEN Form 114): Required if aggregate foreign financial accounts exceed USD 10,000 at any point in the calendar year. Indian NRE, NRO, and Demat-linked cash accounts all count.

- Form 8938 (FATCA): Thresholds for US residents — USD 50,000 on the last day or USD 75,000 at any point (single filers); USD 100,000 / USD 150,000 for married joint filers.

- PFIC (IRS Form 8621): Indian mutual funds are foreign pooled investment vehicles. Most qualify as PFICs (where 75%+ of income is passive or 50%+ of assets produce passive income). Under the default Section 1291 regime, gains face punitive tax treatment, including interest charges on deferred gains. Elections like Qualified Electing Fund (QEF) or mark-to-market can reduce this burden, but require careful annual filing.

The PFIC issue is the single most overlooked US tax trap for NRIs investing in Indian mutual funds. It can sharply cut net returns on redemption.

Repatriation Rules

- NRE accounts: Fully repatriable with no annual cap. Principal and interest can be transferred to the US without restriction.

- NRO accounts: Repatriable up to USD 1 million per financial year after paying applicable taxes. Form 15CA/15CB is required for NRO remittances.

Deciding upfront which investments sit in NRE vs. NRO accounts avoids repatriation bottlenecks later — and can mean the difference between freely moving funds and waiting months to clear tax certificates.

Common Mistakes NRIs Make When Investing in India from the USA

Cross-border investing creates compliance complexity that catches many NRIs off guard. These four errors show up repeatedly in initial client reviews — and each one carries real financial or regulatory cost:

Using a resident demat or savings account after acquiring NRI status. This violates FEMA regulations, and penalties under FEMA Section 13 can reach 3x the sum involved (or ₹2 lakh where the amount is not quantifiable). Resident savings accounts must be re-designated to NRO, and resident demat accounts converted to NRI demat accounts — without delay.

Ignoring PFIC classification risk on Indian mutual funds. US-based NRIs who invest through Indian AMCs often don't realize the PFIC (Passive Foreign Investment Company) tax regime can apply to all gains at redemption. Without the right elections filed, the tax cost on exit can far exceed what was anticipated.

Not claiming DTAA benefits. NRIs routinely pay full taxes in both countries because they don't file the required forms or work with an advisor who understands both jurisdictions. The credit does not apply automatically — it requires active documentation and filing on both sides.

Putting foreign-earned income into an NRO account instead of NRE. This limits future repatriation to USD 1 million per year with tax deduction, when the same money in an NRE account would have been fully and freely repatriable. The account type decision at investment entry determines repatriation flexibility at exit.

Frequently Asked Questions

Can NRIs from the USA invest in Indian mutual funds?

Yes, but with restrictions. Several major AMCs — including HDFC MF Online and UTI MF — do not accept US-based NRI investments due to FATCA/CRS compliance requirements. AMCs like PPFAS MF, SBI MF, and Nippon India MF do accept NRI investors, though eligibility varies by scheme and transaction mode. Verify directly with the fund house before investing.

What is the difference between NRE and NRO accounts for investment purposes?

An NRE account holds foreign-earned income, is tax-free in India, and is fully repatriable — best for investments you plan to bring back to the USA. An NRO account holds India-sourced income like rent and dividends, is taxable in India, and caps repatriation at USD 1 million per financial year after taxes and documentation.

Do NRIs need to pay tax in both the USA and India on Indian investment income?

India will deduct TDS on investment income and capital gains. The India-USA DTAA allows NRIs to claim a foreign tax credit in the US (via IRS Form 1116) for taxes already paid in India, preventing true double taxation. Claiming this credit requires filing the appropriate forms in both countries — it does not apply automatically.

Can NRIs do intraday trading in Indian stock markets?

No. Intraday trading — buying and selling the same stock within the same trading day — is prohibited for NRIs under RBI/FEMA regulations. NRIs are restricted to delivery-based equity trades only and are also barred from currency derivatives and commodity derivatives.

How do NRIs typically target 12% returns from Indian investments?

Nifty Indices data shows a historical 10-year return of 12.55% for the Nifty 50, with a 20-year TRI CAGR of approximately 12.44%. NRIs targeting this range typically invest in diversified equity mutual funds or direct equity through PMS, while accepting associated market risk and a longer investment horizon. These are historical figures — not guarantees.

What happens to my existing Indian investments when I become an NRI?

Existing investments (stocks, mutual funds) remain intact, but linked accounts must be redesignated. Savings accounts become NRO accounts and resident Demat accounts must be converted to NRI Demat accounts. Holding a resident account after becoming an NRI is a FEMA violation — address this as soon as your residency status changes.