Introduction

Consider a founder who spent 25 years building a business, accumulating ₹50 crore across promoter equity, real estate, and a few mutual funds. Then a regulatory change hits the sector, the promoter stock drops 40%, and a property deal falls through just when family expenses spike. Suddenly, a wealth-building story becomes a wealth-preservation crisis.

This scenario is more common than most affluent investors acknowledge. Building wealth and protecting it are different disciplines — the instincts that help someone accumulate assets (concentration, risk-taking, reinvestment) can actively destroy value when left unmanaged.

For HNIs, UHNIs, business owners, and promoters in India, risk management in financial planning is the systematic process of identifying, assessing, and mitigating financial threats before they cause damage. The stakes are higher here because the risks are more interconnected — a market correction can trigger a liquidity crisis, which forces a distressed asset sale, which creates an unexpected tax liability.

This article covers the major categories of financial risk, a practical five-step risk management process, concrete mitigation strategies, and the building blocks of a resilient financial plan.

Key Takeaways

- Risk management means proactively identifying threats — not reacting to losses after they occur

- The five major risk categories are market, credit, liquidity, operational, and legal/regulatory risk

- A structured process involves identifying, analysing, prioritising, mitigating, and continuously monitoring risks

- Core mitigation tools include diversification, insurance, liquidity reserves, and hedging

- A SEBI-registered fiduciary adviser aligns recommendations with your goals, free from commission conflicts

What Is Risk Management in Financial Planning?

Risk management in financial planning is the ongoing practice of identifying potential threats and developing strategies to reduce their impact before they derail your goals. Those threats fall into two broad categories: internal (job loss, health issues, business failure) and external (market downturns, inflation, regulatory changes).

Risk Tolerance vs. Risk Capacity

Two concepts are frequently confused here, and the distinction matters enormously.

The CFA Institute distinguishes between:

- Risk tolerance — how much volatility an investor is psychologically comfortable with

- Risk capacity — how much financial loss they can actually absorb without compromising their goals

- Risk perception — a subjective assessment of how risky a particular investment feels

A promoter might be highly risk-tolerant emotionally but have limited risk capacity if 80% of their net worth sits in a single listed stock. A retired UHNI might have high risk capacity on paper but very low risk tolerance after decades of capital preservation. Both dimensions must be assessed to build a sound plan.

SEBI mandates that registered Investment Advisers conduct risk profiling and suitability assessments before recommending any investments — this is the regulatory baseline, not optional.

Why This Is Especially Critical for HNIs

As wealth grows, risks become more interconnected. A market downturn can trigger a liquidity problem, which forces a distressed asset sale, which creates a tax event — each step amplifying the last. This cascade effect is rare for smaller portfolios but almost predictable at the HNI and UHNI level.

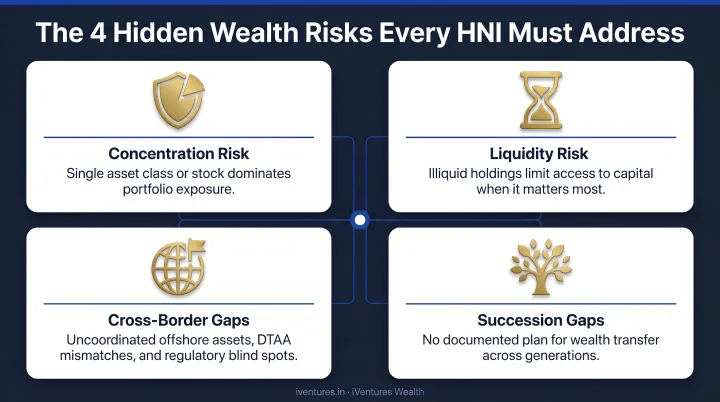

The risks that compound most destructively include:

- Concentration risk — excessive exposure to a single stock, sector, or promoter entity

- Liquidity mismatch — capital locked in illiquid assets (real estate, unlisted equity, AIFs) when cash is needed

- Cross-border complexity — NRI or OCI status introducing FEMA, DTAA, and multi-jurisdiction tax exposure

- Succession gaps — no documented estate or inheritance plan when a key wealth-holder is incapacitated

Each of these demands a coordinated response — not isolated product decisions — which is precisely where a structured risk management framework adds the most value.

Types of Financial Risk in Personal Wealth Management

Understanding the specific risk categories relevant to Indian HNI and UHNI investors is the foundation of any coherent risk plan.

Market Risk

Market risk is the potential for losses from movements in equity prices, interest rates, currency values, and inflation. The NIFTY 50 delivered a -9.88% 1-year price return as of May 2026, illustrating that even benchmark indices experience meaningful drawdowns. For investors with concentrated promoter holdings or sector-specific exposure, the impact of a correction is often far sharper than the index suggests.

SEBI's PMS investor guidance explicitly flags this: focused portfolios may amplify risks when specific investments underperform. For NRI investors, currency movements add another dimension: RBI's Liberalised Remittance Scheme allows residents to remit up to USD 250,000 per financial year, but cross-border portfolios carry ongoing rupee-dollar exposure that requires active management.

Credit Risk

Credit risk is the risk that a borrower or counterparty fails to meet their obligations. In fixed-income portfolios, this surfaces as issuer default risk on bonds and debt funds.

According to CRISIL's FY2024 default study, the overall annual default rate was 1.3% — a 16-year low — but this aggregate masks significant rating-grade variation:

| Credit Rating | Average 10-Year Default Rate |

|---|---|

| AAA | 0.00% |

| AA | 0.05% |

| BBB | 0.52% |

| BB | 3.01% |

| C | 24.20% |

For business-owning families who extend inter-corporate loans or invest in private credit, counterparty risk at lower credit grades is substantial. India's corporate bond market has grown over 50% in the past five years to ₹54 lakh crore as of March 2025. This expands the opportunity set, but also the complexity of credit assessment.

Liquidity Risk

Liquidity risk is the inability to access cash when needed without incurring significant losses. For HNI and UHNI investors, a disproportionate share of wealth is often locked in illiquid assets — real estate, private equity, promoter holdings, or alternative investments.

The Franklin Templeton episode in April 2020 is the clearest recent case study: six debt mutual fund schemes were wound up as COVID-19 froze credit markets, leaving investors unable to redeem for an extended period. The real planning error is assuming liquidity holds during market stress — not the instrument itself.

According to the Knight Frank Wealth Report 2025, direct real estate accounted for 22.5% of the typical family office portfolio, with more than four in ten family offices planning to increase exposure. Real estate's illiquidity profile means cash needs during emergencies or estate settlements often cannot be met without accepting distressed pricing.

Operational Risk

Particularly relevant for business-owning families and promoters, operational risk includes failed processes, key-person dependency, technology failures, or vendor concentration. When a business founder is the primary income earner and the business depends on that individual, incapacitation disrupts both the enterprise and the personal financial plan at once.

This is why key-person insurance and the structural separation of business cash flows from personal wealth are not optional extras; they are foundational risk controls.

Legal and Regulatory Risk

India's tax and regulatory landscape evolves regularly, and each change can materially alter a wealth plan. Examples include:

- Capital gains tax changes — LTCG was reintroduced at 10% under Section 112A in Budget 2018; subsequent amendments have continued to adjust rates and indexation treatment

- Estate planning gaps — outdated wills, unclear succession structures, and nominee vs. legal heir confusion create wealth transfer risks

- SEBI regulatory changes — AIF categorisation, PMS regulations, and investment adviser frameworks evolve

- Cross-border compliance — FEMA, DTAA application, FATCA/CRS reporting requirements for NRI/OCI clients

Each of these areas requires proactive monitoring. Reacting after a regulatory change has taken effect — rather than planning ahead of it — turns avoidable risk into real cost.

The Risk Management Process: A Step-by-Step Approach

Step 1 — Risk Identification

A holistic audit of all financial assets, liabilities, income sources, business interests, insurance coverage, and estate documents. For Indian HNI clients, this also means mapping family structures, joint holdings, trust arrangements, HUF assets, and any cross-border exposure.

In practice, this is an asset consolidation exercise — surfacing and unifying everything into a single family balance sheet. That means identifying:

- Dormant bank accounts and unclaimed mutual fund folios

- Scattered demat accounts and insurance policies

- Overseas holdings and cross-border assets

- Interests held across spouses, children, HUFs, and family trusts

Step 2 — Risk Analysis and Quantification

Each identified risk is assessed for its probability of occurrence and potential financial impact. A simple framework:

Expected Loss = Probability × Impact

This calculation helps prioritise. Inadequate term insurance for a 45-year-old primary income earner with ₹10 crore in family liabilities has both high probability of materialising at some point and catastrophic impact — it demands immediate action. An unlikely regulatory change affecting a minor investment has low expected loss and can be monitored.

Step 3 — Risk Prioritisation

Once quantified, risks are ranked by severity and urgency:

- Act immediately: High-impact, high-probability risks — concentrated promoter stock, absent or inadequate insurance, illiquid asset concentration with no liquidity buffer

- Act soon: Medium-impact risks — estate documents not updated post-marriage or business exit, cross-border tax structuring gaps

- Monitor: Low-severity risks that don't require immediate capital allocation but warrant annual review

Step 4 — Risk Mitigation

With risks ranked, mitigation strategies are matched to each priority. The approach varies by risk type:

- Rebalancing a concentrated portfolio through a structured multi-year glide path

- Purchasing adequate term, disability, or key-person insurance

- Establishing a liquidity buffer in high-quality fixed income

- Restructuring estate documents with experienced legal practitioners

- Using hedging instruments for large listed shareholdings or cross-currency exposure

Step 5 — Ongoing Monitoring and Review

Plans require revisiting as life evolves. At minimum, an annual review is essential — but certain events should trigger an immediate reassessment:

- Business exits, inheritance, or retirement that shift the asset base

- A child's marriage or major family structural change

- Significant regulatory changes affecting investments or tax structures

- Material market movements that alter portfolio concentration or liquidity

Between scheduled reviews, portfolios should be monitored continuously so that no single event catches the plan off-guard.

Proven Risk Mitigation Strategies for Affluent Investors

Diversification Across Asset Classes and Geographies

For Indian HNI investors, genuine diversification means moving beyond concentration in domestic equities or real estate toward a multi-asset allocation spanning:

- Equity — domestic and international

- Debt — bonds, fixed income, debt funds

- Alternatives — AIFs, private credit, select PMS

- Real assets — real estate (liquid REITs vs. direct property), gold

- Global — US, Europe, Asia exposures through regulated routes

A business founder described this well in practice: holding most net worth in promoter equity and a few properties, with minimal exposure to financial assets, left personal and family needs directly exposed to business cycles.

Carving out a portion of annual surplus into a diversified portfolio, with a clear drawdown rule so each profitable year automatically builds a ring-fenced personal corpus, reduces concentration risk and creates income streams independent of the operating business.

Insurance as a Foundational Risk Transfer Tool

India's insurance penetration remained at just 3.7% in 2024-25 according to the IRDAI Annual Report 2024-25, indicating that even at the HNI level, coverage is frequently inadequate relative to actual wealth and income exposure.

The insurance framework for an affluent household should cover:

- Term life insurance — sized to replace income and cover liabilities for dependants

- Health insurance — top-up or super top-up covers beyond employer policies

- Disability income protection — often overlooked, but a prolonged inability to work is more probable than death before 60

- Key-person insurance — for business owners and promoters, covering the enterprise's dependence on a specific individual

- Professional indemnity — for doctors, CXOs, and professionals with liability exposure

Maintaining a Structured Liquidity Reserve

Insurance transfers risk, but liquidity determines whether you ever need to act on it under duress. The standard recommendation of three to six months of expenses works for salaried employees with predictable income. For HNIs with business-linked income, irregular liquidity events, and complex asset profiles, the standard falls short.

The right framework here is a three-bucket approach:

| Bucket | Time Horizon | Instruments | Purpose |

|---|---|---|---|

| Safety | 5–7 years of expenses | High-quality fixed income | Immediate liquidity, capital preservation |

| Stability | 8–15 years | Balanced, asset-allocated portfolio | Moderate growth, planned expenditures |

| Growth | 15+ years | AIFs, PMS, private equity | Long-term wealth appreciation |

This structure ensures that a short-term cash need, whether a family emergency, estate settlement, or market dislocation, never forces a distressed sale of long-term holdings.

Hedging for Concentrated and Cross-Border Positions

Two distinct concentrations require active management at the HNI level:

- Promoter equity concentration — structured de-risking over a multi-year glide path is more practical than derivatives-based hedging. The goal is systematic diversification: reducing single-company concentration into a broader portfolio over defined timeframes, with clear rules governing how much is sold and reinvested each year.

- Cross-border currency exposure (NRI/OCI clients) — managed through GIFT City structures (which allow USD-denominated portfolio tracking), natural diversification across currency exposures, and selective hedging where the exposure justifies the cost.

Best Practices for Building a Risk-Resilient Financial Plan

Build Your Framework Before You Need It

The most effective risk management happens before losses occur. Setting up a risk framework during stable periods — not during a market crisis or a health emergency — gives you the time and clarity to make rational decisions.

Revisit Your Plan at Every Major Life Stage

A young founder's risk profile differs sharply from that of a retired UHNI. Financial plans must evolve as circumstances change. Key milestones that warrant a review include:

- A business IPO or liquidity event

- Receiving an inheritance or large windfall

- Approaching or entering retirement

- Children reaching financial independence

Schedule a comprehensive review at least annually with a qualified adviser — and an additional review after any material life or market event.

Work with a SEBI-Registered Fiduciary Adviser

As of mid-2026, there were only 1,044 registered Investment Advisers in India against more than 12 crore securities-market investors — making genuinely fiduciary advice genuinely scarce.

Unlike product distributors who earn trail commissions on recommendations, a SEBI-registered Investment Adviser is legally prohibited from accepting commissions or placement fees from product manufacturers. The fee-only model means every recommendation is based on your risk profile and suitability — not on what generates revenue for the adviser.

That distinction matters in practice. iVentures Wealth (SEBI RIA registration INA000019026) has operated on this fiduciary model since 2005, serving HNIs, UHNIs, family offices, and business-owning families across India.

With ₹1,200+ crore in assets under advice and a CFA-led research team, the firm's advisory framework covers risk profiling, asset consolidation, estate planning, and ongoing portfolio monitoring — built for the full scope of affluent wealth, not a single account in isolation.

Frequently Asked Questions

What is risk management in financial planning?

Risk management in financial planning is the process of identifying, assessing, and mitigating threats — internal (job loss, illness, business failure) and external (market downturns, inflation, regulatory changes) — that could derail your financial goals. The key distinction: it demands proactive planning, not reactive damage control.

What are the 4 types of financial risk?

The four core categories are market risk (price and rate movements), credit risk (borrower or counterparty default), liquidity risk (inability to access cash without loss), and operational risk (failures in processes or systems). A fifth — legal and regulatory risk — is especially relevant for Indian HNI investors navigating SEBI regulations and evolving tax laws.

What are the 4 types of risk management?

The four primary risk management responses are: avoidance (eliminating the risk entirely), reduction/mitigation (reducing the probability or impact), transfer (shifting the risk to another party, such as through insurance), and retention (consciously accepting a risk when the cost of mitigating it outweighs the potential loss). Most financial plans use a combination of all four depending on the risk category.

How does risk tolerance affect your financial plan?

Risk tolerance determines how much volatility you're comfortable accepting in pursuit of returns, directly shaping your asset allocation across equities, debt, and alternatives. It must always be assessed alongside risk capacity — being comfortable with volatility doesn't mean you can financially afford to absorb significant losses.

What is the difference between risk avoidance and risk mitigation?

Risk avoidance means eliminating exposure entirely — for example, not investing in highly speculative instruments. Risk mitigation reduces severity or likelihood without exiting the activity entirely — diversifying a concentrated portfolio rather than leaving the market. Most plans rely on mitigation, since eliminating all risk also eliminates the returns needed to meet long-term goals.

Why should high-net-worth individuals pay special attention to risk management?

HNIs and UHNIs face a broader, more interconnected set of risks — concentrated equity positions, illiquid real estate, business-linked income, complex estate structures, and cross-border exposure — meaning a single unmanaged risk event can trigger cascading consequences across the entire wealth ecosystem. The greater the wealth, the greater the complexity, and the greater the cost of a planning gap.