The India-US Double Taxation Avoidance Agreement (DTAA) exists precisely to prevent this. Signed on September 12, 1989 and entering into force on December 18, 1990, the treaty governs how cross-border income between Indian and US residents is taxed — through reduced withholding rates, foreign tax credits, and specific exemptions by income type.

This guide covers everything NRIs, OCIs, and cross-border investors need to know: who qualifies, how residency is determined, what treaty rates apply to each income type, how to reduce TDS, and the exact steps to claim benefits and report them correctly in your ITR.

Key Takeaways

- The India-US DTAA prevents double taxation through reduced withholding rates and foreign tax credits — not blanket exemptions.

- Tax residency is determined separately in each country; Article 4 tie-breaker rules resolve dual-residency conflicts.

- Treaty rates vary by income type: 15%/25% on dividends, 10%/15% on interest, 10%/15% on royalties — all lower than the standard 30% US withholding rate.

- Claiming benefits requires a TRC, Form 10F, and ITR disclosures via Form 67 and Schedule FSI.

- The US Saving Clause bars US citizens and green card holders from using the treaty to avoid US tax on worldwide income.

Who Is Eligible for the India-US DTAA?

The treaty applies to residents of India and the United States — individuals, companies, partnership firms, trusts, and other entities earning income in both countries. Residents of third countries cannot invoke this treaty to reduce their taxes.

Understanding who qualifies is only half the picture — the treaty's scope also determines which taxes it actually covers.

Taxes Covered

| Covered | Excluded | |

|---|---|---|

| United States | Federal Income Tax (Internal Revenue Code) | Accumulated earnings tax, personal holding company tax, social security taxes |

| India | Income tax including surcharge and surtax | Penalties, taxes on undistributed corporate income |

The "Resident" Requirement

Under Article 4, a person qualifies as a resident of a contracting state if they are liable to tax there by reason of domicile, residence, citizenship, place of management, or incorporation. However, being taxed in a country only on income sourced from that country — without broader tax liability — does not meet this threshold. That distinction matters for NRIs who earn India-sourced income but remain domiciled abroad.

How the India-US DTAA Works: Residency and Relief

Double taxation arises when the same income is taxed in both countries. An Indian resident working in the US pays US federal tax on US-source employment income — but India also taxes that income because the person is an Indian resident.

The DTAA resolves this through the foreign tax credit method under Article 25. Tax paid in one country is credited against tax owed in the other, so the effective burden reflects the higher of the two applicable rates — not both combined.

Determining Tax Residency

US residency is established through two tests:

- Green Card Test — holding a lawful permanent resident card at any point during the calendar year automatically makes you a US tax resident

- Substantial Presence Test — requires at least 31 days in the current year, plus 183 days across three years using a weighted formula (all current-year days + one-third of prior-year days + one-sixth of second-prior-year days)

India residency under Section 6 of the Income Tax Act requires 182 or more days in India during the previous year, or 60 days in the current year plus 365 days in the preceding four years (subject to statutory modifications for certain categories).

Both tests can apply to the same individual at the same time — and that overlap is exactly what Article 4 addresses.

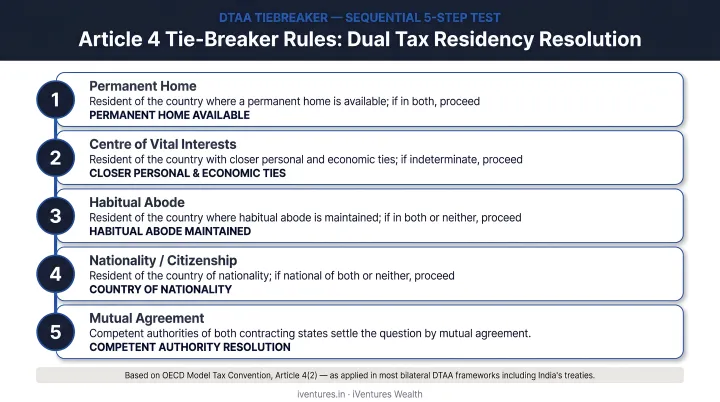

Tie-Breaker Rules Under Article 4

When a person qualifies as a tax resident of both countries simultaneously, Article 4 applies tie-breakers in this sequential order:

- Where does the person have a permanent home?

- If homes exist in both countries — where are personal and economic ties stronger (centre of vital interests)?

- If still inconclusive — which country is their habitual abode?

- Finally — nationality

- If unresolved — mutual agreement between the two governments

Practical example: An Indian citizen on an H-1B visa who meets the US Substantial Presence Test but maintains a permanent home in India and returns regularly may invoke these tie-breaker rules to claim Indian residency for treaty purposes. To claim this position, they must file Form 8833 with the IRS. Skipping this disclosure triggers a $1,000 penalty per occurrence under IRC Section 6712.

Key Treaty Provisions by Income Type

Each income category is governed by a specific treaty article. Here's what applies to NRIs, OCIs, and cross-border investors.

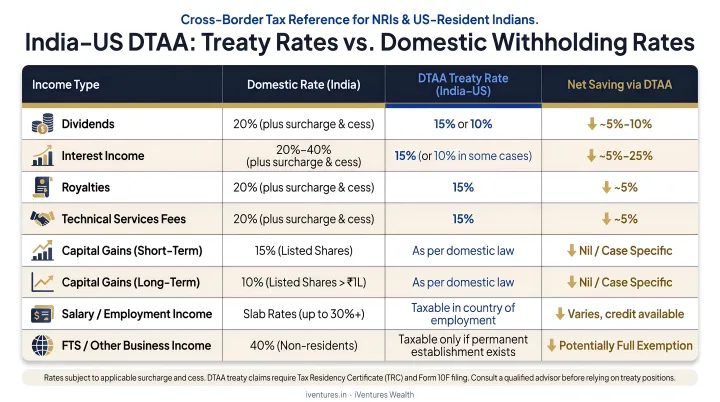

Dividends (Article 10)

Dividends paid by a company in one contracting state to a resident of the other may be taxed in the recipient's country. The source country can also tax, but at a capped rate:

- 15% if the beneficial owner is a company holding at least 10% of the voting stock

- 25% in all other cases

The standard US withholding rate on dividends is 30% under IRC Sections 1441 and 1442 — so the treaty reduces this meaningfully for qualifying Indian resident shareholders.

Interest Income (Article 11)

Interest arising in the US and paid to an Indian resident is primarily taxable in the recipient's country. The source country may also tax, capped at:

- 10% for interest on loans from banks or similar financial institutions

- 15% in all other cases

Against the default 30% US FDAP withholding rate, Indian residents receiving US-source interest can see a reduction of up to 20 percentage points — a significant difference at meaningful investment scales.

Royalties and Fees for Included Services (Article 12)

Article 12 covers not just royalties (payments for use of patents, trademarks, and software) but also Fees for Included Services — technical or consultancy services that transfer knowledge, processes, or know-how. IT professionals, consultants, and technology firms are most commonly affected by this provision.

Current treaty rates:

- 15% for royalties and fees for included services generally

- 10% for payments for use of industrial, commercial, or scientific equipment

Capital Gains (Article 13)

Capital gains sit outside the treaty's unified rate structure. Article 13 preserves domestic-law taxation, meaning each country applies its own rules.

For Indian residents selling US real estate, FIRPTA (Foreign Investment in Real Property Tax Act) applies under IRC Section 1445. Because Article 13 preserves domestic-law treatment of capital gains, FIRPTA withholding is not overridden by the treaty.

Employment Income (Article 16) and Special Categories

Moving from investment income to earned income: employment wages are taxable where the work is physically performed. A short-term exception applies only if all three conditions are met simultaneously:

- Presence in the other state does not exceed 183 days in the relevant taxable year

- Remuneration is paid by an employer not resident in that other state

- Remuneration is not borne by a permanent establishment in that other state

Two additional exemptions worth noting:

- Article 21 (Students/Apprentices): Payments from outside the host state for maintenance, education, or training of a student or business apprentice temporarily present for full-time study are exempt

- Article 22 (Teachers/Researchers): Remuneration for teaching or research at a recognised educational institution is exempt for up to 2 years from first arrival, provided the research is in the public interest

How DTAA Reduces TDS on NRI Income

Without DTAA, NRI income from Indian sources is subject to standard withholding rates. The treaty reduces these significantly. Here's the comparison:

| Income Type | Domestic Rate (India) | Treaty Rate (India-US) |

|---|---|---|

| NRO deposit interest | 30% (Section 195) | 15% (10% for bank loans) |

| Dividends from Indian companies | 20% (Section 115A) | 15% (qualifying corporate) / 25% (others) |

| Royalties / FTS | 20% (Section 115A) | 15% / 10% for equipment |

These rates aren't fixed in practice. Under Section 90 of the Income Tax Act, taxpayers may choose whichever rate is more beneficial — domestic or treaty. For dividends, the domestic 20% rate is actually lower than the treaty's 25% non-qualifying cap, so non-qualifying holders often find the domestic rate more advantageous.

The US Saving Clause: A Critical Exception

The Saving Clause (Article 1(3)) allows the US to tax its citizens and residents as if the treaty had not come into force. This means:

- US citizens living in India cannot use the treaty to escape US taxation on worldwide income

- Dual US-Indian citizens face the same limitation

- Green card holders are treated as US residents under this clause

Only certain articles are protected from the Saving Clause — notably Article 25 (Relief from Double Taxation) and Article 26 (Non-Discrimination). This is frequently misunderstood and has significant implications for dual citizens managing income across both jurisdictions.

For dual citizens and US-connected NRIs, the interplay between the Saving Clause and treaty protections requires careful structuring — particularly around tax residency certificates, foreign tax credits, and PFIC or GILTI exposure. iVentures Wealth's cross-border advisory covers exactly this ground as part of its NRI/OCI wealth management engagements.

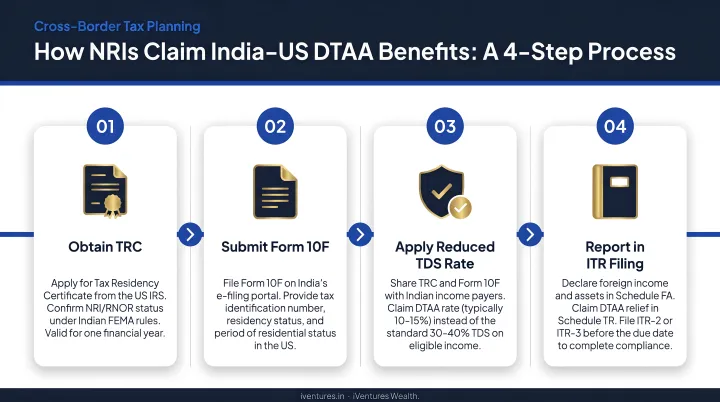

How to Claim DTAA Benefits

Step 1: Obtain a Tax Residency Certificate (TRC)

A TRC is mandatory under Section 90(4) of the Income Tax Act. Indian residents apply using Form 10FA with Indian tax authorities. US residents obtain a certificate of US tax residency (Form 6166) from the IRS.

Step 2: Complete the Required Forms

For Indian residents claiming benefits in India:

- Submit Form 10F electronically to the deductor, along with TRC and a self-declaration

- Provide PAN card copy, passport copy, visa copy, and OCI/PIO proof if applicable

For US residents claiming reduced withholding on US-source income:

- Submit Form W-8BEN (individuals) or Form W-8BEN-E (entities) to US payers

For anyone asserting a treaty override of the IRC:

- File Form 8833 with the IRS — failure to disclose carries a $1,000 penalty

All documentation must be submitted to the deductor before payments are made to ensure withholding at DTAA rates.

Step 3: Calculate Using DTAA Rates

For each income stream, work through this sequence:

- Identify the applicable treaty article and the DTAA rate for that income type

- Compare it against the domestic withholding rate under Indian or US tax law

- Apply whichever rate is more beneficial — the treaty never forces a higher tax than domestic law

Step 4: File Form 67 for Foreign Tax Credit

Once taxes are calculated and paid abroad, Indian resident taxpayers must file Form 67 to claim the foreign tax credit under Rule 128. It must include details of foreign income and taxes paid abroad.

Under amended Rule 128 (CBDT Notification No. 100/2022), Form 67 can be filed any time before the end of the relevant assessment year — it no longer needs to strictly precede ITR submission. That said, filing it alongside or before your ITR reduces the risk of processing delays.

Reporting DTAA Income in Your ITR

Three schedules are critical for cross-border investors filing Indian ITRs:

Schedule FSI (Foreign Source of Income) List each income stream by country code, taxpayer identification number, income earned outside India, taxes paid abroad, tax payable in India, relief available, and the DTAA article invoked.

Schedule TR (Tax Relief) Auto-populates from Schedule FSI. Shows the double taxation relief deducted from your total tax calculation.

Schedule FA (Foreign Assets) Mandatory disclosure for Indian residents who are beneficial owners, beneficiaries, or legal owners of overseas accounts, investments, or property. Non-residents and RNOR individuals are exempt from this requirement.

Non-disclosure or inaccurate disclosure can attract penalties and prosecution under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015.

A common filing error: submitting the ITR without completing Schedule FSI or TR correctly, or delaying Form 67 beyond the assessment year. A recent ITAT Chennai ruling (Shri Rajiv Ramesh Lulla, April 2026) confirmed that delayed Form 67 should not automatically deny foreign tax credit — but filing on time reduces the risk of disputes.

Frequently Asked Questions

What is the DTAA agreement between India and the USA?

The India-US DTAA is a bilateral tax treaty signed on September 12, 1989 (effective December 18, 1990). It prevents the same income from being taxed twice for residents earning cross-border income — through reduced withholding rates and foreign tax credits applicable in both countries.

How do I avoid double taxation in India?

Two routes are available. First, claim the credit method at filing — report foreign taxes via Form 67 and Schedules FSI and TR in your ITR. Second, apply for reduced TDS at source by submitting a valid TRC and Form 10F to the deductor before payment.

What is the 30% US withholding tax?

Under IRC Sections 1441 and 1442, the US withholds 30% on passive income (dividends, interest, royalties) paid to nonresident aliens. The India-US DTAA reduces these to 15%/25% on dividends, 10%/15% on interest, and 10%/15% on royalties — upon submission of a valid Form W-8BEN to the US payer.

Is a TRC mandatory for claiming DTAA benefits in India?

Yes. A Tax Residency Certificate is mandatory under Section 90(4) of the Indian Income Tax Act. It must be submitted to the deductor along with Form 10F to claim reduced TDS rates. Without a valid TRC, the deductor must withhold at standard domestic rates.

When was the India-US DTAA signed, and does it still apply?

The treaty was signed on September 12, 1989, and entered into force on December 18, 1990. It remains fully in effect today — though domestic law amendments in either country can interact with specific provisions, so verify current rates against the latest Finance Act each year.

What is the Saving Clause in the India-US DTAA?

The Saving Clause (Article 1(3)) allows the US to tax its citizens and residents as if the treaty had not come into force — meaning US citizens living in India, dual US-Indian citizens, and green card holders generally cannot use treaty benefits to escape US taxation on worldwide income. Articles 25 and 26 are among the provisions protected from the Saving Clause.