Traditional advisory arrangements — a CA here, a wealth manager there, a private banker somewhere else — were never built to handle this kind of complexity. They handle their piece, but no one handles the whole.

That's the gap a family office fills. Yet most affluent families aren't sure what a family office actually is, whether they qualify for one, or whether the structure justifies itself. This article answers those questions directly: what a family office is, what it concretely does, and when it makes sense to pursue one.

Key Takeaways

- A family office coordinates financial, tax, legal, and legacy management under one roof — free from product mandates or advisor conflicts.

- India's family offices grew from 45 (2018) to ~300 by 2024, managing ~$30B, per EY's Indian Family Office Playbook.

- Three models exist (SFO, MFO, VFO); MFO suits most Indian families with ₹50–500 Cr in investable assets.

- The right trigger is complexity — multiple entities, cross-border assets, or next-generation stakeholders — not a specific number.

- Without coordination, families risk tax leakages, contradictory advisor guidance, and preventable succession crises.

What Is a Family Office?

A family office is a private advisory structure — whether a dedicated entity or a coordinated arrangement — that manages the financial, investment, tax, legal, and legacy affairs of one family (Single Family Office) or multiple families (Multi-Family Office), operating exclusively in the family's interest.

That last part matters. A private bank earns from products it distributes. A retail wealth manager works within a defined product shelf. A family office has no such mandate — it functions as a financial command centre, coordinating everything from asset allocation and tax planning to succession and philanthropy through a single, accountable structure.

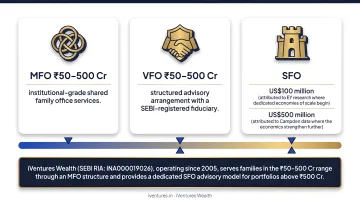

SFO, MFO, and VFO: The Three Models

| Structure | Who It Serves | Cost Profile | Practical Threshold |

|---|---|---|---|

| Single Family Office (SFO) | One family exclusively | High fixed overhead | ₹500 Cr+ in investable assets |

| Multi-Family Office (MFO) | Multiple families, shared infrastructure | Significantly lower per family | ₹50–500 Cr in investable assets |

| Virtual Family Office (VFO) | Technology-enabled, lean setup | Minimal fixed costs | Families in early formalisation |

For most Indian families, the SFO model only becomes economically rational at significant scale. EY's research identifies approximately US$100 million in investable assets as the threshold where a dedicated family office begins to achieve economies of scale — and Campden's global operating cost data suggests the economics strengthen further above US$500 million.

For families with ₹50–500 Cr in investable assets, an MFO or a structured advisory arrangement with a SEBI-registered fiduciary typically provides the most practical path to institutional-grade family office services.

Matching the model to the mandate: iVentures Wealth (SEBI RIA: INA000019026), operating since 2005, serves families in the ₹50–500 Cr range through an MFO structure and provides a dedicated SFO advisory model for portfolios above ₹500 Cr.

Key Benefits of a Family Office

Each benefit below maps to a specific operational failure that affluent families hit when complex wealth grows without a coordinated structure — tax leakages, fragmented reporting, succession disputes, and missed allocation decisions. These aren't hypothetical risks. They're the default outcome when wealth management stays siloed.

Benefit 1: Consolidated Oversight Across All Entities and Accounts

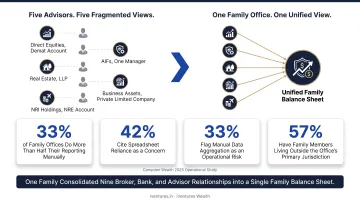

Without a family office, most affluent families have their wealth scattered — direct equities in one demat account, AIFs with one manager, real estate held in an LLP, business assets in a private limited company, and NRI holdings in an NRE account. Each advisor sees their slice. No one sees the whole.

A family office solves this by creating a single, unified view across all holdings. Consolidated reporting tracks performance and risk across asset classes and entities. No advisor is giving contradictory guidance, because all advisors coordinate through one accountable structure.

Why fragmentation is expensive:

Campden's 2025 operational study found that:

- One-third of surveyed family offices still perform more than half their reporting manually

- 42% cite spreadsheet reliance as a concern

- 33% flag manual data aggregation as an operational risk

- 57% have family members living outside the office's primary jurisdiction — adding coordination complexity at every level

Fragmentation creates concrete problems: capital sitting idle while one advisor waits for information another holds, overlapping exposures no single party can see, and no ability to act on opportunities with full financial context.

Consolidated oversight fixes this. It enables proactive asset allocation, real-time risk management, and faster decision-making during critical events like a business exit or market dislocation.

This benefit matters most when:

- Holdings span multiple legal entities (LLPs, trusts, private limited companies)

- The family includes NRI or OCI members with cross-border assets

- Business wealth and personal investable assets are managed separately

An example from iVentures' practice: one family had assets spread across nine separate broker, bank, and advisor relationships. Consolidating these into a unified family balance sheet — paired with a formal governance framework — eliminated redundant positions and created a single source of truth for every financial decision.

Benefit 2: Tax Optimization and Estate Planning

Tax in India is not neutral for high-income families. Under the old regime, the surcharge alone reaches 25% for income between ₹2–5 Cr and 37% above ₹5 Cr, pushing effective individual tax rates as high as 42.74% according to PwC's India Tax Summaries. LTCG on listed equities is taxed at 12.5% on gains exceeding ₹1.25 lakh. Cross-border transactions carry FEMA compliance obligations, including the LRS limit of US$250,000 per individual per financial year.

A family office doesn't treat tax as an afterthought. It builds tax strategy into the investment process — selecting holding structures (LLP, trust, private limited, AIF), managing LTCG/STCG timing across financial years, coordinating advance tax across all family entities, and ensuring FEMA compliance for NRI members.

In practice, this means:

- Choosing the right structure before a liquidity event, not after

- Managing distribution timing to control surcharge exposure

- Coordinating across entities so no CA is optimising in isolation

- Planning ahead for estate transfers to avoid compounding tax leakages

One concrete example: iVentures restructured a third-generation family trust for a textile manufacturer, resulting in savings of over ₹2 crore in inheritance tax and ensuring clean wealth transfer to the next generation. In a separate engagement, a business-owning client was guided to deploy surplus funds from within their private limited company rather than extracting higher salaries — deferring taxation meaningfully over multiple years.

Who needs this most:

- After a major liquidity event — business sale, PE exit, or IPO proceeds

- When the family includes NRI members with cross-border holdings and FEMA exposure

- When multiple generations are beginning to share or receive assets

Benefit 3: Multigenerational Wealth Preservation and Legacy Governance

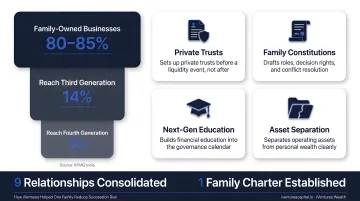

KPMG India reports that family-owned businesses account for 80–85% of incorporated Indian businesses — but only 14% reach the third generation, and just 5% the fourth. The culprit isn't market cycles. It's the absence of governance.

A family office creates the formal structure that makes multigenerational continuity possible: private trusts, legally sound wills, family constitutions that define decision-making authority, and structured processes for bringing next-generation members in as active participants, not passive heirs.

Without this, succession is treated as a legal formality rather than a governance exercise — and the consequences play out publicly. The Kalyani family, the Oberois following PRS Oberoi's 2023 death, and the KK Modi family disputes all illustrate what happens when succession is reactive rather than planned. The Godrej family required five years of negotiation to achieve an amicable 2024 division; others have not been as fortunate.

What a family office does differently:

- Sets up private trusts before a liquidity event, not after

- Drafts family constitutions that define roles, decision rights, and conflict resolution

- Builds next-generation financial education into the governance calendar

- Separates operating business assets from personal investable wealth cleanly

iVentures has helped families formalise this structure — including one case where a family with parents and two adult children consolidated across nine relationships and simultaneously established a family charter, substantially reducing succession risk.

When to prioritise this:

- Adult children with different financial priorities are approaching inheritance age

- A business sale or IPO is imminent and proceeds need a governance framework

- The family spans multiple generations with different risk appetites

What Happens Without a Family Office Structure

The pattern is consistent across affluent Indian families without coordinated oversight:

No unified accountability. Each advisor works within their own silo. No one is responsible for the family's full picture — which means contradictory positions, missed rebalancing, and no single source of truth.

Tax leakage compounds silently. Without cross-entity tax planning, surcharges accumulate and structuring opportunities are missed. Year-end tax management becomes reactive rather than strategic — often after the damage is done.

Succession gaps turn into legal battles. Without a family constitution or trust structure in place, a sudden liquidity event or the death of the patriarch can trigger disputes that drag on for years. Landmark Indian family business disputes — including some of the country's most prominent business families — show how quickly decades of wealth creation can unravel.

The next generation inherits assets, not governance. Younger family members receive wealth before they understand the responsibilities attached to it. That gap compounds with every passing generation.

Each of these gaps is addressable — but only when someone is looking at the whole picture. That is precisely what a family office structure provides.

How to Get the Most Value from a Family Office

The structure has to match the family's actual complexity. Over-engineering with a full SFO when the wealth and operational need doesn't justify it creates unnecessary fixed cost. Under-structuring by relying on fragmented advisors leaves the family exposed to every consequence described above.

A family office produces its strongest outcomes when:

- The family has a clear investment policy — defining risk appetite, asset allocation principles, and decision-making authority before capital is deployed

- All advisors coordinate through one accountable point — tax, legal, and investment professionals working with shared context, not in silos

- Next-generation members are brought in early — as informed participants in governance, not passive recipients of wealth

For Indian families with investable assets of ₹50 Cr and above, the practical alternative to a standalone SFO is a SEBI-registered, fiduciary advisory firm that covers the same service stack — portfolio management, tax coordination, succession planning, and consolidated reporting — without the fixed cost of building and staffing a dedicated office.

iVentures Wealth operates this way: 20+ years of family office advisory experience, ₹1,200 Cr+ in assets under advice across 150+ client families, and SEBI RIA registration. Families get coordinated advice across investments, tax, and succession — through one accountable team, not a roster of disconnected specialists.

Conclusion

A family office — in whatever form suits the family's scale and complexity — is about three things: control over how wealth is invested and structured, clarity across all entities and accounts, and continuity across generations.

Its benefits compound when applied consistently. Tax efficiency preserved this year becomes a larger estate next decade. A governance structure put in place before a liquidity event prevents the family dispute that would have followed. Coordinated oversight catches the risk that fragmented advice misses altogether.

A family office is an ongoing practice — one that evolves as the family's wealth, relationships, and objectives shift over time. The families that preserve wealth across generations understand this. They treat the office not as a structure they built once, but as something they actively maintain and adapt.

Frequently Asked Questions

What is a family office in investing?

A family office is a private advisory structure that manages a wealthy family's investments, taxes, legal affairs, and succession planning, operating exclusively in the family's interest. Unlike a bank or fund manager, it carries no product mandates or distribution incentives.

Are family offices profitable?

The family office itself is typically a cost centre, not a profit centre. Its return is measured in preserved wealth, optimised taxes, avoided estate disputes, and better investment outcomes. For families with sufficient complexity, these gains consistently outweigh the cost of running the structure.

What is the minimum wealth for a family office?

A full Single Family Office becomes economically rational above ₹500 Cr in investable assets, per industry consensus. Families with ₹50–500 Cr are typically better served by a Multi-Family Office or a SEBI-registered advisory firm providing comprehensive family office services.

What is the difference between a single family office and a multi-family office?

An SFO serves one family exclusively with fully customised services and higher fixed costs. An MFO provides institutional-grade family office services to multiple families through shared infrastructure, making it a cost-efficient alternative for families not yet at the ₹500 Cr threshold.

How is a family office different from a private wealth manager?

A private wealth manager typically recommends products from a defined shelf and earns distribution commissions. A family office, or a true fiduciary advisory firm, operates exclusively in the client's interest, coordinating all financial and non-financial functions without product-driven conflicts of interest.