That conversation is harder than it sounds. Research from John Ward at Northwestern University's Kellogg School of Management found that only about 30% of family businesses survive to the second generation, and just 13% make it to the third. Those aren't abstract numbers — they represent real businesses where the transition simply wasn't planned.

This guide covers what succession planning actually involves, the specific risks of delaying it, and a practical roadmap your family can act on now — not when the founder eventually decides it's time.

Key Takeaways

- Succession planning means transferring both leadership and ownership in a structured way — two separate decisions that require separate frameworks

- Skipping a plan risks family conflict, business disruption, eroded enterprise value, and avoidable tax costs

- Start 5–10 years before any anticipated transition — not when retirement feels near

- Effective succession runs governance, legal structuring, successor development, and wealth planning in parallel — not one after another

Why Family Business Succession Planning Cannot Wait

According to PwC's 12th Global Family Business Survey, 36% of Indian family businesses have no clear succession plan — worse than the global average of 28%. At the same time, 52% face senior generation resistance to transitioning leadership, nearly double the global rate of 29%.

That gap between ambition and preparation is where businesses break down.

The Founder Syndrome Problem

The delay is rarely strategic. The Kellogg School of Management describes "founder's syndrome" as a condition where decision-making and organisational identity are so tied to one person that the business's sustainability is compromised. Common patterns include:

- Believing the business cannot run without them

- Tying personal identity so deeply to the role that stepping back feels like loss

- Avoiding succession conversations because they feel uncomfortably close to questions of mortality or irrelevance

The result: the conversation keeps getting deferred, the timeline compresses, and when a transition eventually happens — planned or not — the business is unprepared.

Risks of Inaction

When a founder exits without a plan — whether through retirement, incapacitation, or sudden loss — the consequences arrive fast and compound across multiple fronts:

- Operations stall. Vendors, clients, and employees lose confidence quickly. Decisions slow, and the business starts losing ground before anyone has a plan.

- Enterprise value erodes. Research published by Harvard Business Review found that poorly managed leadership transitions destroy nearly $1 trillion in S&P 1500 market value annually. Buyers and institutional partners systematically discount private businesses without clear leadership continuity.

- Family conflict becomes structural. Without documented guidelines, succession decisions turn into emotional battles fought in real time. The Murugappa Group's dispute over board representation — involving a ₹9 billion enterprise — shows how absent governance converts a family disagreement into years of legal and reputational damage.

- Tax exposure compounds. Unstructured ownership transfers in India can trigger capital gains obligations and stamp duty costs that erode the value being passed on. Most of these costs are avoidable — but only with advance planning.

Key Elements of a Strong Family Business Succession Plan

Ownership vs. Management: Two Separate Decisions

The most common and costly error in family succession is treating ownership and management as one decision. They are not.

A family member can hold equity without running operations. A non-family professional can lead the business without owning a stake. Keeping these decisions separate — each with its own criteria and documentation — prevents the ambiguity that becomes a source of conflict later. Two clear decisions, made independently, are easier to defend to every stakeholder in the room.

Governance Structures

Family governance is the backbone of any durable succession plan. Three components carry the most weight:

- Family constitution — sets shared values, employment standards, and succession rules in writing, so expectations are documented before disputes arise

- Family council — bridges family and business, giving members a structured forum to shape policy without disrupting day-to-day operations

- Shareholder agreement or partnership deed — defines ownership rights and what happens under triggering events: death, exit, incapacitation, or dispute

Firms like iVentures Wealth, which provides family office advisory to 150+ affluent Indian families, include family-charter and family-constitution drafting as a core service — working in coordination with senior legal counsel to ensure these documents hold up under scrutiny and are enforceable when it matters most.

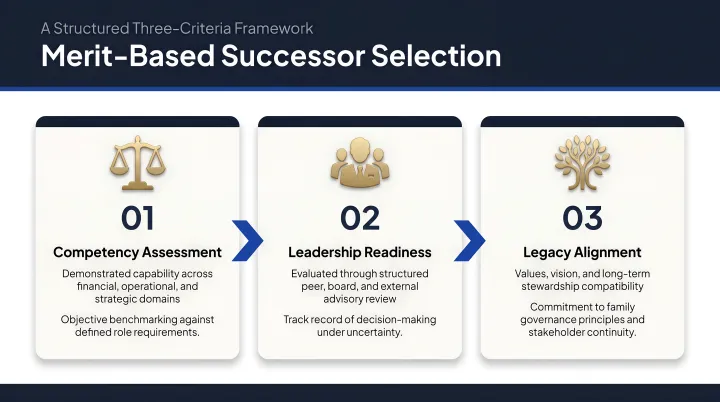

Successor Identification: Merit Over Birth Order

Research published in the Strategic Management Journal (Calabro et al., 2018) found that reliance on primogeniture — defaulting to the eldest child — reflects an emotional rather than strategic choice, and demonstrably undermines firm performance. A structured selection framework looks different:

- Define the competencies the leadership role actually requires

- Set transparent eligibility criteria: education, external experience, tenure inside the business

- Apply these criteria consistently, regardless of family position

Legal Components

Every succession plan needs these legal instruments in place:

- Wills — clearly documenting intent and asset distribution

- Private family trusts — particularly relevant for Indian families managing complex, multi-entity wealth

- Buy-sell agreements — governing what happens to ownership stakes under various triggering events

- Shareholder arrangements — defining transfer restrictions and dispute mechanisms

How to Build Your Family Business Succession Plan: A Step-by-Step Guide

Step 1: Assess the Business and the Owner's Goals

Planning starts with honest answers to basic questions: What is the business actually worth, and what are its operational vulnerabilities? What does the owner want post-transition — a full exit, an advisory role, retained financial benefit? What does financial security look like for the founder's household independent of the business?

These questions often surface uncomfortable truths. A common pattern iVentures encounters: business owners whose household expenses are entirely dependent on business cash flows, with no separation between company capital and family income. That dependency needs to be resolved before transition, not after.

Step 2: Define Succession Objectives and Set a Timeline

Document specific goals. Is the intent to transfer full control to the next generation? Bring in a professional CEO while family retains ownership? Position the business for eventual sale? Vague intentions produce vague plans.

Set a realistic timeline — the Family Business Institute recommends 5–10 years as the appropriate planning window. That timeframe allows for successor development, governance formalisation, legal structuring, and a gradual handover — all of which take longer than families expect.

Step 3: Identify and Develop Potential Successors

Development is not a brief conversation. It is a multi-year process:

- Identify candidates early — ideally while they are still forming professional identities

- Require external work experience — 3–5 years outside the family business builds independent credibility and perspective that internal exposure alone cannot provide

- Expose them progressively — board meetings, cross-functional roles, P&L responsibility

- Use structured mentorship — pair candidates with experienced operators inside and outside the family

A 2021 qualitative study of multi-generational family businesses confirmed that next-gen members who worked outside the firm developed broader perspectives and stronger credibility when they eventually joined. Only 39% of family businesses currently have a formal development plan for future leaders — which means most are navigating succession without structured guidance.

Step 4: Address Legal, Tax, and Estate Planning in Parallel

While successors are being developed, the legal and financial architecture needs to be built alongside them. Succession planning and estate planning must run simultaneously. Key elements include:

- Structuring private family trusts with documented distribution and governance rules

- Updating wills to reflect current intent and asset distribution preferences

- Planning ownership transfers with an eye on capital gains, gift tax exemptions, and stamp duty

- Reviewing the tax efficiency of each transfer mechanism before executing it

These decisions have long lead times. Engaging a wealth advisory firm like iVentures Wealth early ensures tax-efficient structures are in place well before the transfer occurs — not pieced together under time pressure.

Step 5: Implement, Communicate, and Review Regularly

Execution has two dimensions that families consistently underestimate: communication and continuity.

Communication means telling every relevant stakeholder — including family members who will not take leadership roles — what the plan is and why decisions were made. Unexplained decisions become resentments.

Continuity means the plan must be a living document. Business conditions shift, tax laws are revised, and family circumstances evolve — the plan must keep pace with all of it.

iVentures Wealth structures ongoing succession monitoring as part of its family office mandates, treating succession plans as frameworks that adapt over time rather than documents filed away after signing.

Succession Options: Which Transition Model Fits Your Family?

Four main paths exist for family business transition:

| Model | Description | Best Fit When |

|---|---|---|

| Internal family succession | Next-gen family member becomes CEO | Qualified successor exists; family wants to retain operational control |

| Professional external management | Hired non-family CEO runs operations | Business complexity exceeds next-gen readiness; family wants ownership not operations |

| Hybrid model | Family holds board/ownership; professionals manage operations | Strong family governance exists; business requires specialist leadership |

| Sale or merger | Full or partial exit | No suitable internal successor; optimal exit conditions exist |

Many Indian families default to assumption-based succession — the eldest son takes over — without evaluating whether that person is actually suited to the role. The PwC finding that 52% of Indian family businesses face senior generation resistance to transition suggests this default is often driven by the incumbent's reluctance to seriously evaluate alternatives, not by genuine confidence in the successor.

The right model rarely announces itself. Start by asking whether the next generation has demonstrated leadership outside the family context, whether the business has outgrown family management capacity, and whether a clean exit would serve the family's long-term financial interests better than continued operational involvement. Those answers — not family tradition — should drive the decision.

Tax and Wealth Planning in Family Business Succession

Ownership transfer is a taxable event in most scenarios. The structure of that transfer determines how much value actually reaches the next generation.

Key Tax Provisions for Indian Families

Gift of shares between relatives: Under Section 56(2)(x) of the Income Tax Act, gifts of shares to defined relatives — spouse, siblings, lineal ascendants and descendants — are fully exempt from tax, regardless of value. No capital gains tax applies to the donor at the point of gifting.

Capital gains on subsequent transfers: Post-July 2024 Budget changes introduced the following rates:

| Asset Type | STCG Rate | LTCG Rate | LTCG Threshold |

|---|---|---|---|

| Listed equity shares | 20% | 12.5% | Above ₹1.25 lakh/year |

| Unlisted shares | Slab rate | 12.5% | No basic exemption |

Stamp duty: Transfer of demat shares attracts stamp duty of 0.015% on the consideration amount.

Inheritance: India has no inheritance or estate tax. Transfers through a will are exempt. When heirs eventually sell, capital gains apply using the original owner's acquisition cost.

How the transfer is taxed is only half the equation — the structure used to execute it determines what's actually retained. Three approaches are most commonly deployed:

Commonly Used Structures

- Private family trusts — protect assets, document distribution rules, and provide continuity. Determinate trusts are taxed at individual beneficiary rates; discretionary trusts face the Maximum Marginal Rate (~39–42%), so the choice of trust type carries real tax consequences

- Holding company structures — centralise family ownership, separate operating businesses from the ownership layer, and allow structured buyout provisions

- Phased share gifting — spreads transfers across multiple years to stay within exempt thresholds and limit capital gains exposure in any single year

For families managing multi-entity, complex wealth structures, coordinating business succession with broader personal wealth planning is where most value is either preserved or lost. iVentures Wealth's family office advisory works with families at ₹100 Cr+ in investible assets, bringing succession structuring, private trust establishment, estate planning, and tax-efficient wealth transfer under one coordinated plan — so these decisions reinforce each other rather than create gaps.

Common Mistakes to Avoid in Family Business Succession

Three mistakes derail more succession plans than any others:

Procrastinating on documentation. Many families begin conversations but never formalise them. Verbal understandings collapse under pressure — when stakes are high and relationships are strained, a handshake agreement provides no protection. A written, legally binding plan is not optional.

Confusing fairness with equality. Giving every heir an equal ownership stake is not the same as being fair. If one child has worked in the business for fifteen years and another has not, equal equity distribution creates resentment — from the contributor who feels undervalued and from the passive owner who holds influence without accountability. Roles and assets allocated by capability and contribution are fairer in practice, even when uncomfortable to discuss.

Neglecting non-business assets. Succession planning typically focuses on the operating business while ignoring real estate, investment portfolios, and liquid assets. This leaves the wealth transfer plan incomplete. For many Indian families, these non-business assets — property holdings, mutual fund portfolios, fixed deposits — can exceed the company's value. A clear business succession plan means little without an equally clear plan for everything else.

Frequently Asked Questions

How do you plan succession in a family-owned business?

Begin with a clear-eyed review of the business's financial health, ownership goals, and potential successors. From there, build out governance structures, address tax and estate planning, and communicate the plan to all family stakeholders — ideally starting 5–10 years before the intended transition.

What is succession in a family-owned business?

Succession is the planned transfer of leadership and ownership from one generation to the next — covering both who will run the business and who will own it. A well-structured plan keeps the business running without disruption while protecting the family's long-term legacy.

What are the 4 types of succession?

The four main types are: internal family succession (a family member takes over leadership), external management succession (a hired professional leads while family retains ownership), a hybrid model (family holds governance while professionals manage operations), and business sale or merger as an exit path.

What is the difference between succession and continuity?

Succession is the transfer of leadership and ownership to a new person or generation — it is an event. Continuity is the business's ability to keep operating without disruption during and after that transfer — it is the outcome. Good succession planning is designed to produce continuity.

What are the 5 D's of succession planning?

The 5 D's are the five events that can force an unplanned transition: Death, Disability, Divorce, Disagreement (among partners or family members), and Departure (voluntary exit). A robust succession plan addresses all five scenarios, not just planned retirement.

What are the 4 C's of a family business?

The 4 C's — Competence, Commitment, Control, and Culture — represent the pillars of a healthy family business. Succession planning must ensure the next leader is capable, genuinely committed, clear on governance responsibilities, and aligned with the family's core values.