This guide explains what a Lower TDS Certificate is, why it matters, who qualifies, how to apply through the TRACES portal, and what factors determine approval.

Key Takeaways

- A Lower/Nil TDS Certificate (Form 13 / Section 197, or Form 128 under IT Act 2025) lets buyers deduct TDS on your actual tax liability — not the default rate

- Without it, TDS on a ₹1.5 crore sale is deducted on the full amount, not just your taxable gain

- Any NRI whose actual tax liability is lower than the default TDS rate is eligible to apply

- Applications go through the TRACES portal and require a Digital Signature Certificate (DSC)

- Apply at least 30–60 days before the expected sale date — processing typically takes 2–8 weeks

What Is a Lower TDS Certificate for NRIs?

A Lower/Nil TDS Certificate is an official approval issued by the Income Tax Department under Section 197 of the Income Tax Act, 1961 that authorises the buyer to deduct TDS at a reduced rate, or nil, instead of the standard default rate. Under the new Income Tax Act, 2025, the equivalent provision is Section 395(1).

The Problem It Solves

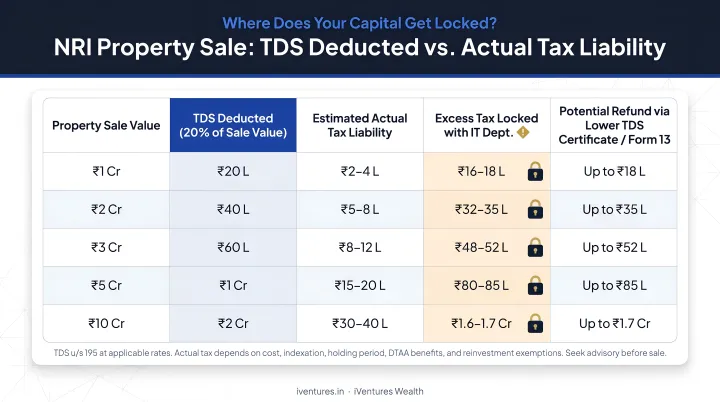

The default TDS mechanism doesn't account for exemptions, deductions, or treaty benefits. Consider this example:

| Scenario | Amount |

|---|---|

| Property sale consideration | ₹2,00,00,000 |

| Indexed cost of acquisition | ₹1,60,00,000 |

| Actual taxable capital gain | ₹40,00,000 |

| TDS without certificate (13% on full sale value) | ₹26,00,000 |

| Actual tax liability (13% on ₹40 lakhs gain) | ₹5,20,000 |

| Excess TDS locked up | ₹20,80,000 |

That excess sits with the tax department until you file an ITR and wait for the refund. The process can take months.

Why NRIs Can't Use Form 15G or 15H

Form 15G and Form 15H are available only to resident individuals below the taxable threshold. NRIs are excluded entirely. Instead, NRIs must apply directly to the Assessing Officer via Form 13 (current Act) or Form 128 (2025 Act).

Why NRIs Selling Property Need a Lower TDS Certificate

The Default TDS Rate Problem

Under Section 195 of the Income Tax Act, buyers must deduct TDS on payments to non-residents at the rates in force — with no automatic adjustment for exemptions, deductions, or DTAA benefits.

For long-term capital assets (property held more than 24 months), the applicable rate is 12.5% without indexation per the Income Tax Department's capital gains guidance. Add Health and Education Cess at 4%, and the effective rate reaches 13% at minimum — and up to approximately 14.95% with a 15% surcharge on larger gains.

Short-term gains (property held 24 months or less) are taxed at applicable slab rates, which can be higher.

The Refund Dependency Trap

Without a Lower TDS Certificate, excess TDS is deducted upfront. Getting it back means:

- Filing an Indian Income Tax Return

- Having it processed by the jurisdictional Assessing Officer

- Waiting for the refund to be credited

While the Ministry of Finance reported average ITR processing of 10 days for verified returns in AY 2023-24, NRI property sale cases typically attract additional scrutiny and take substantially longer. A Lower TDS Certificate removes this dependency entirely.

How DTAA Benefits Factor In

NRIs resident in treaty countries — including the USA, UAE, UK, Canada, and Singapore — may be entitled to reduced tax rates or exemptions under India's Double Taxation Avoidance Agreements. But these benefits don't apply automatically.

Under Section 90(4) and 90(5) of the Income Tax Act, treaty relief requires:

- A valid Tax Residency Certificate (TRC) from the foreign government

- Additional information filed electronically in Form 10F

The Lower TDS Certificate is how these DTAA benefits get formally recognised before the transaction closes, rather than pursued as a post-sale refund claim.

It Applies Across Property Types

DTAA treaty relief aside, the default TDS exposure applies regardless of how a property was acquired. NRIs selling inherited property, jointly owned property, or property received as a gift face the same withholding obligation. The acquisition type changes nothing — making the Lower TDS Certificate equally relevant across all scenarios.

Who Is Eligible and What Documents Are Required

Eligibility

Any NRI (individual or foreign company) receiving income from India subject to TDS may apply. For property sales specifically, eligibility hinges on demonstrating that actual tax liability — after exemptions, deductions, carry-forward losses, and DTAA benefits — is lower than the default TDS rate.

There is no minimum transaction size or income threshold to apply.

Core Documents Required

The following are typically required when filing Form 13 or Form 128:

- PAN card copy

- Passport and visa/OCI card details

- Capital gains computation for the current financial year (indexed cost, improvement costs, applicable exemptions)

- Previous 3 years' ITRs (where applicable — first-time filers or recent NRIs may need alternative documentation)

- Form 26AS and AIS (Annual Information Statement)

- Property purchase deed and proposed sale agreement copy

- Stamp duty valuation certificate

- Improvement cost proofs (invoices, receipts)

- Buyer's PAN and proposed payment schedule

- Tax Residency Certificate (TRC) and Form 10F — mandatory for DTAA claims

The TRACES system also requires a capital gains computation template and a note justifying the certificate issuance under Rule 28AA.

A Note on Completeness

Incomplete applications trigger additional queries from the Assessing Officer, extending processing timelines significantly. For NRIs managing this process from abroad, working with an advisor who handles capital gains computation and DTAA coordination can cut down on errors and back-and-forth with the department. iVentures Wealth's NRI advisory practice supports clients through both stages.

How to Apply for a Lower TDS Certificate: Step-by-Step

Applications are filed electronically through the TRACES portal. Under the current Income Tax Act, this is Form 13 at nriservices.tdscpc.gov.in. Under the new Income Tax Act, 2025 (effective 1 April 2026), this transitions to Form 128 at tdscpc.gov.in under Section 395(1).

Critical for NRIs: The TRACES NRI portal only accepts e-verification via Digital Signature Certificate (DSC). Aadhaar OTP and mobile OTP are not available for NRI applicants.

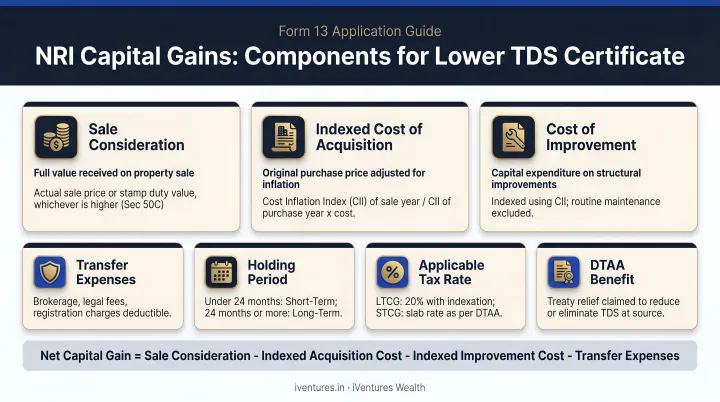

Step 1: Compute Capital Gains and Assess Eligibility

Before filing, prepare a detailed capital gains computation covering:

- Indexed cost of acquisition (for long-term assets)

- Indexed cost of improvement

- Applicable exemptions — Section 54 (reinvestment in residential property), Section 54EC (capital gain bonds up to ₹50 lakhs)

- Any DTAA relief applicable based on your country of residence

This computation is the foundation of your application and determines the requested lower TDS rate.

Step 2: File Form 13 / Form 128 on TRACES

Log in to the TRACES portal and navigate to Statements/Forms → File Forms → Form 13 (or Form 128 under the new Act). Select the relevant financial year, choose "Original" as the application type, and enter:

- Nature of income and payment

- Requested deduction rate

- Responsible deductor's TAN (buyers deducting TDS under Section 195 are required to hold a TAN under Section 203A)

- Basic taxpayer details (these auto-populate from your registered TRACES profile)

Step 3: Upload Supporting Documents

Upload the capital gains computation, property documents, past ITRs, Form 26AS, TRC and Form 10F for DTAA claims, and buyer details. Form 128 under the new Act includes real-time validation checks and structured annexures that guide the submission process.

Step 4: Assessing Officer Review

The jurisdictional Assessing Officer (TDS) reviews the application. They may request revised computations, seek clarifications, or ask for additional documents. Note that per CPC(TDS) Notification No. 02/2023, the system suggests an estimated rate based on Rule 28AA parameters — but the AO retains discretion to arrive at a different rate independently.

Step 5: Certificate Issued — Share with Buyer

Once approved, the certificate is issued electronically. It specifies:

- The approved TDS rate

- Period of validity (typically one financial year)

- TAN of the designated buyer/deductor

Share this certificate with your buyer immediately. Your buyer is then legally authorized to deduct TDS at the approved lower rate.

Key Factors That Affect Your Application — and Mistakes to Avoid

What Determines Approval (and the Rate)

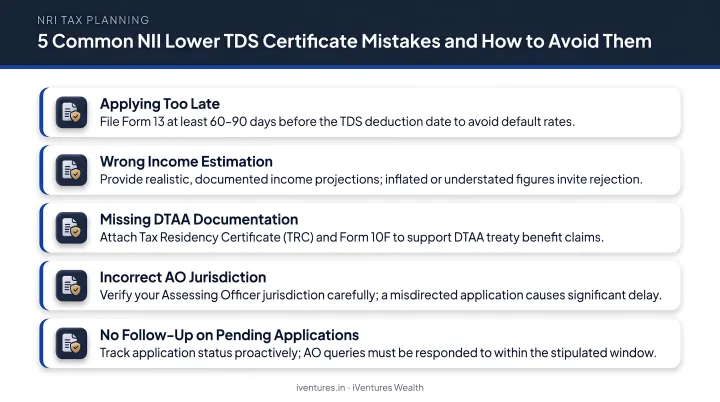

Capital gains computation quality is the single biggest factor. Common triggers for rejection or AO queries:

- Incorrect classification of asset as short-term vs. long-term

- Errors in indexation calculations

- Missing improvement costs

- Exemptions claimed without supporting documentation

DTAA documentation completeness matters if you're claiming treaty benefits. A missing, expired, or incorrectly filed TRC or Form 10F means the DTAA claim gets disregarded entirely during review.

Past tax compliance is reviewed. Consistent prior filing history strengthens applications; unfiled returns or prior TDS defaults can cause delays or rejection.

Application Timing

There is no statutory deadline for filing, but the certificate must be in hand before the sale transaction closes — because Section 195 requires deduction at credit or payment, whichever is earlier.

Processing typically takes 2–8 weeks, potentially longer in high-workload jurisdictions or complex cases. Apply at least 30–60 days before the expected sale date.

Common Mistakes to Avoid

- Waiting until after the sale agreement is signed to start the application

- Applying without a valid DSC — getting one from outside India requires advance planning

- Assuming the buyer doesn't need TAN — buyers deducting TDS under Section 195 require TAN under Section 203A, unlike the PAN-only rule that applies to resident property purchases under Section 194-IA

- **Overlooking FEMA and repatriation requirements** — Form 15CA/15CB compliance (or their equivalents under the 2025 Act) is separate from but interlinked with the TDS certificate process

- Not planning post-sale reinvestment before applying — Section 54EC bond investments or Section 54 reinvestment strategies must be factored into the computation before filing, not decided after

iVentures Wealth's NRI/OCI advisory practice covers capital gains optimisation — including LTCG structuring, indexation, Section 54EC, and Section 54F strategies — and works alongside tax advisors to integrate treaty benefit planning before the sale closes.

Frequently Asked Questions

How do I get a lower TDS deduction certificate as an NRI?

File an application in Form 13 (or Form 128 under the Income Tax Act, 2025) on the TRACES portal, supported by your capital gains computation, property documents, past ITRs, and other required documents. The Assessing Officer reviews the application and issues the certificate if satisfied with the documentation.

Who is eligible for a lower TDS deduction certificate?

Any NRI whose actual tax liability — after exemptions, deductions, carry-forward losses, and applicable DTAA benefits — is lower than the default TDS rate is eligible to apply under Section 197 of the current Act (or Section 395(1) of the 2025 Act), with no minimum transaction size required.

What is the typical processing timeline?

Processing generally takes 2 to 8 weeks from submission, depending on the jurisdiction, application complexity, and the Assessing Officer's workload. Apply at least 30–60 days before the expected sale date to avoid delays.

What documents are needed for an NRI property sale lower TDS application?

Key documents include your PAN card, passport/OCI details, capital gains computation, purchase and proposed sale deed copies, previous 3 years' ITRs (where applicable), Form 26AS, buyer's PAN, and — for DTAA claims — a Tax Residency Certificate with Form 10F.

Can TDS be reduced to nil for NRIs?

Yes. If your actual tax liability works out to zero after exemptions — for example, through full reinvestment under Section 54 or investment in Section 54EC bonds — the Assessing Officer can issue a Nil TDS Certificate, provided all claims are backed by documentary evidence.

What if excess TDS has already been deducted before I obtain the certificate?

File an Indian Income Tax Return to claim a refund through the standard process. This adds time and requires engagement with the Assessing Officer's jurisdiction, so securing the certificate before the transaction closes is the more practical approach.