The core distinction is this: in PMS, every trade your portfolio manager executes is a taxable event in your name. In mutual funds, internal portfolio activity is invisible to you from a tax perspective — your liability only arises when you redeem units. That single difference compounds significantly over a long investment horizon.

This guide covers the current tax rates (post-Finance Act 2024), how each structure is taxed in practice, where the real divergence lies, and how to think about tax efficiency when choosing between the two.

Key Takeaways

- In PMS, you directly own securities — every buy/sell triggers a capital gains event in your name that financial year

- Mutual fund investors pay zero tax on internal portfolio churn; taxes arise only at unit redemption

- Post-Finance Act 2024: equity STCG is 20% (Section 111A) and LTCG is 12.5% above ₹1.25 lakh (Section 112A) — the same rates apply to both PMS and mutual funds

- Frequent STCG events at 20% in high-churn PMS create a real tax drag compared to deferred mutual fund taxation

- Low-churn PMS strategies can match mutual funds on post-tax outcomes; tax efficiency depends heavily on portfolio turnover

PMS vs Mutual Funds: Quick Tax Comparison

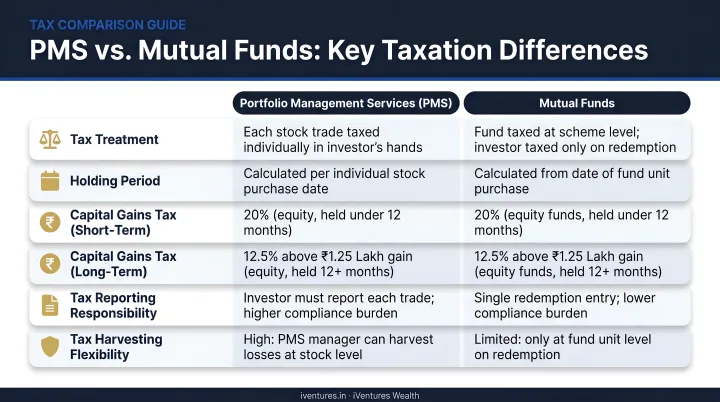

The table below captures the key taxation differences at a glance. For HNIs and UHNIs managing large portfolios, these distinctions have a direct impact on post-tax returns and annual compliance workload.

| Aspect | PMS | Mutual Funds |

|---|---|---|

| Ownership | Direct securities in investor's Demat | Fund units (pooled structure) |

| When taxes trigger | Each transaction (buy/sell) | At unit redemption/switch |

| STCG (equity) | 20% on each sale under 12 months | 20% only at redemption |

| LTCG (equity) | 12.5% above ₹1.25 lakh; same rate, but triggered more often | 12.5% above ₹1.25 lakh; deferred to redemption |

| Dividend/interest income | Added to investor's income; taxed at slab rate | Same — taxed at slab rate in investor's hands |

| Management fee deductibility | Under litigation; no definitive ruling yet | Not applicable |

| Section 80C benefit | Not available | Available via ELSS (up to ₹1.5 lakh) |

| ITR complexity | High — every transaction must be reported | Lower — consolidated statement sufficient |

The core distinction: PMS triggers taxes with each portfolio transaction, while mutual funds defer the tax event until you redeem. At scale, this timing difference compounds meaningfully over time.

How PMS Investments Are Taxed

PMS taxation is straightforward in structure but demanding in detail. Because investors hold securities directly in their own Demat account, every transaction the portfolio manager executes — buying, selling, or switching stocks — is treated as a personal capital transaction of the investor, taxable in that financial year.

Equity PMS Taxation

Post-Finance Act 2024, the applicable rates for listed equity are:

- STCG (held under 12 months): 20% under Section 111A, for transfers on or after 23 July 2024

- LTCG (held over 12 months): 12.5% under Section 112A, on gains exceeding ₹1.25 lakh per financial year

The ₹1.25 lakh LTCG exemption applies across all equity instruments combined for the year — not per stock, and not per PMS account separately.

Non-Equity and Debt PMS Taxation

The treatment varies by instrument type:

- Listed debt securities: 12-month holding period for long-term classification; LTCG taxed at 12.5% without indexation (transfers on or after 23 July 2024); STCG at applicable slab rates

- Unlisted bonds/debentures: Section 50AA applies — gains treated as short-term regardless of holding period, for transfers/redemptions on or after 23 July 2024

- Other non-listed assets: 24-month threshold for long-term classification

Dividends, Interest, and Other Income

Any dividend or interest income earned within a PMS portfolio is added to the investor's total income and taxed at their applicable slab rate. Section 194 requires 10% TDS on dividends at source.

For investors in the 30% bracket, this distinction matters: slab-rate income from a PMS portfolio carries a meaningful tax cost that flat-rate capital gains treatment does not.

Are PMS Management Fees Tax-Deductible?

This is unsettled territory. ITAT decisions conflict: the Devendra Motilal Kothari case (Mumbai, 2011) and C.M. Jain Impex (2012) disallowed PMS fees against capital gains under Section 48, while KRA Holding & Trading (Pune) and Joy Beauty Care (Kolkata, 2018) allowed deductions in specific fact patterns.

Where PMS activity qualifies as business income, Section 37 deductions have been permitted in more recent case law.

No CBDT circular has settled this question. Treat fee deductibility as fact-specific and verify with a qualified tax advisor before claiming it.

How Mutual Funds Are Taxed

Unlike PMS, mutual funds pool your capital with other investors — and that structure changes when taxes apply. Your tax liability arises only at the point of redemption. Until then, the fund manager can buy and sell securities freely, with the NAV adjusting internally for any gains or losses, creating no tax event for you.

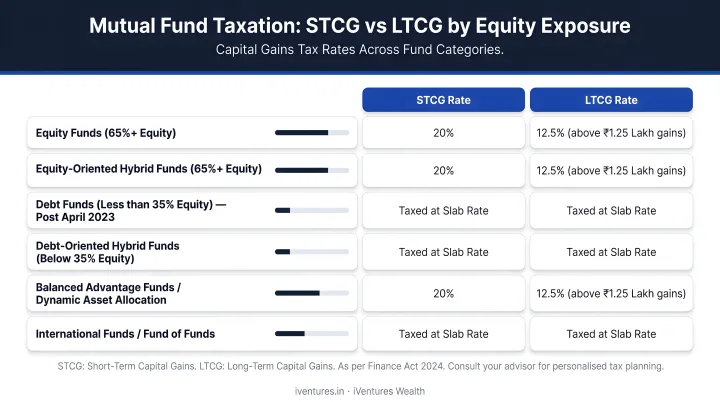

Taxation by Fund Category

| Fund Category | Holding Period for LTCG | STCG Rate | LTCG Rate |

|---|---|---|---|

| >65% domestic equity exposure | 12 months | 20% (Section 111A) | 12.5% above ₹1.25 lakh (Section 112A) |

| 35%–65% equity (hybrid) | Applicable holding period | Slab rate | 12.5% (post 23 July 2024) |

| ≤35% equity / debt-heavy (specified MF) | Section 50AA applies | Slab rate | Not applicable (Section 50AA) |

Note on Section 50AA (effective 1 April 2026): The amended definition covers funds investing more than 65% in debt or money market instruments. For FY 2026-27 onwards, confirm your fund's classification before assuming the tax treatment in the table above applies.

Key Tax Triggers to Be Aware Of

Internal rebalancing is tax-free for you. But these actions do trigger capital gains:

- Redemption of units (partial or full)

- Switching between fund schemes

- Systematic Withdrawal Plans (SWPs) — each withdrawal is a redemption

- Systematic Transfer Plans (STPs) — each transfer is treated as a redemption from the source fund

- SIP instalments — each SIP investment has its own purchase date, so LTCG/STCG classification is calculated separately per instalment at the time of redemption

ELSS and the Section 80C Benefit

Equity Linked Savings Schemes (ELSS) carry a 3-year lock-in and investments up to ₹1.5 lakh per year qualify for deduction under Section 80C of the Income Tax Act. PMS investments do not qualify for this deduction. For investors in higher tax brackets, this additional benefit makes ELSS a meaningful part of the equity allocation conversation.

The Critical Tax Difference Between PMS and Mutual Funds

The headline tax rates for equity — 20% STCG and 12.5% LTCG — are identical for PMS and mutual funds. The real difference lies in when you pay and how often — and that timing gap compounds into a material wealth gap over time.

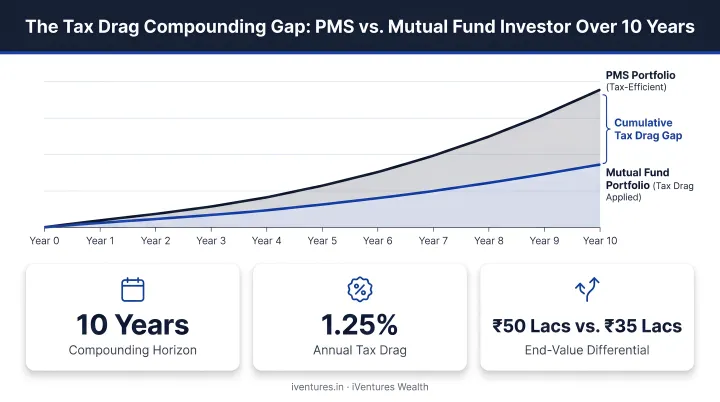

The Compounding Cost of Frequent Taxation in PMS

When a mutual fund investor's tax is deferred, their full corpus — including the amount that would have otherwise gone to taxes — stays invested and compounds. A PMS investor paying taxes year after year on realized gains is working with a shrinking base.

Consider an illustrative scenario: ₹1 crore invested over 10 years at a 12% gross annual return, with 40% annual portfolio churn generating primarily short-term gains.

- Mutual fund investor: Internal churn creates no tax drag. Taxes are paid only at redemption. The full corpus compounds for 10 years before tax.

- PMS investor: 40% of the portfolio turns over annually, generating STCG at 20%. Each year, a portion of returns leaves the portfolio as tax, reducing the compounding base.

The difference in terminal wealth is not marginal. CFA Institute research illustrates that in a 20-year simulation at 7% gross returns with annual taxation at 20%, tax drag ranges from 23% to 28% depending on the income mix — a material reduction in final wealth.

The Impact of Portfolio Churn on PMS Tax Drag

Not all PMS strategies carry the same tax burden. The difference between a buy-and-hold PMS and a high-frequency one is stark:

- Low-churn PMS (under 20% annual turnover): Most gains qualify as long-term; tax drag is modest and comparable to mutual funds

- High-churn PMS (40%+ annual turnover): Frequent sales under 12 months generate STCG at 20%, materially eroding post-tax returns

These numbers make due diligence non-negotiable. Before committing to any PMS strategy, ask for the historical portfolio turnover ratio alongside gross return data. A strategy showing 18% gross returns with 60% annual churn may deliver less post-tax wealth than a 14% gross return strategy with 15% churn.

Tax-Loss Harvesting: A PMS Advantage

PMS has a genuine edge here. Because you directly own each security, losses from specific stocks can be strategically harvested to offset gains within the same financial year — reducing your net taxable capital gains.

In mutual funds, this granular control does not exist. You can only redeem units of a scheme as a whole; you cannot selectively crystallize losses on individual holdings within the fund's portfolio.

For active PMS investors reviewing positions near year-end, this can be a meaningful lever. iVentures Wealth builds LTCG/STCG management into its advisory process and coordinates gain/loss documentation directly with clients' chartered accountants for accurate ITR filing.

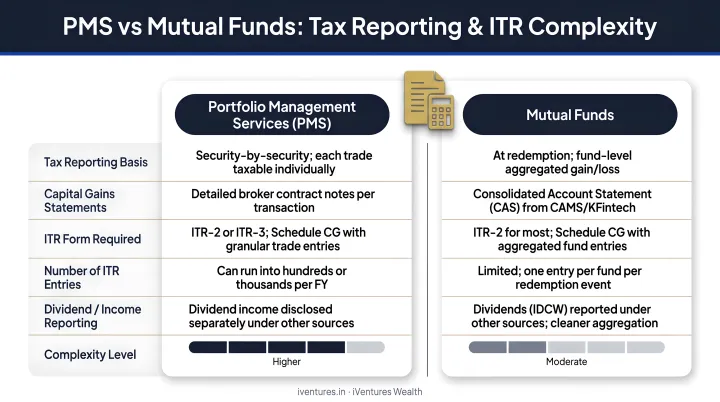

Tax Reporting and Documentation Complexity

PMS investors face considerably higher filing complexity:

- Every buy and sell transaction must be reported individually in the ITR

- PMS providers issue annual portfolio statements, realized gain/loss summaries, dividend/interest income reports, and audit-related certificates

- Depending on income characterization, investors may need ITR-2 (capital gains) or ITR-3 (business income)

Mutual fund investors receive a consolidated account statement and report far fewer line items. The difference in administrative burden is real — PMS investors should work with a tax advisor who understands capital markets, not just routine filings.

Which Is More Tax-Efficient: PMS or Mutual Funds?

The honest answer is: it depends on the strategy, not just the structure.

Mutual funds are generally more tax-efficient when:

- You want the compounding benefit of deferred taxation over a long horizon

- You are in a high income tax bracket, making slab-rate dividend income from PMS expensive

- The fund manager runs high turnover — you benefit from the tax shield the fund structure provides

- You want ELSS exposure for Section 80C benefits

PMS can be tax-comparable or advantageous when:

- The strategy is genuinely low-churn with most gains qualifying as long-term

- You actively use tax-loss harvesting across your portfolio to net gains and losses

- Your corpus is large enough (above the ₹50 lakh SEBI minimum, typically much more in practice) to warrant the customization and reporting overhead

- You need concentrated exposure that no mutual fund can replicate

PMS tax efficiency is strategy-specific, not structural. A disciplined, long-horizon PMS with 10–15% annual churn can deliver post-tax outcomes that rival or exceed certain mutual fund categories. A high-frequency PMS paying STCG on 50% of its portfolio every year is structurally disadvantaged — no alpha is large enough to fully offset that drag indefinitely.

For UHNIs and family offices managing ₹50 crore or more, the interplay of PMS taxation, income slab rates, loss harvesting, estate planning, and multi-generational structuring demands a bespoke approach — not a category-level answer.

iVentures Wealth, a SEBI-registered investment adviser, builds tax-aware portfolio design — across LTCG, STCG, indexation, and DTAA where applicable — directly into how it structures PMS and mutual fund allocations. The goal is optimised post-tax outcomes, not just competitive gross returns.

Frequently Asked Questions

Which is better for taxes: PMS or mutual funds?

Mutual funds have a structural advantage through tax deferral — taxes arise only at redemption, not on internal trades. PMS triggers taxes on every transaction. A genuinely low-churn PMS narrows this gap considerably, so the real comparison comes down to a specific strategy's churn rate and your holding horizon.

Are PMS investments tax-efficient? What about fee deductibility?

PMS tax efficiency tracks directly with churn: low-churn strategies generating mostly long-term gains can be reasonably competitive, while high-churn portfolios face meaningful drag from 20% STCG. On fee deductibility, ITAT rulings conflict and no CBDT circular has settled the matter — confirm your position with a tax advisor before claiming deductions.

What are the STCG and LTCG tax rates on equity PMS investments?

Post-Finance Act 2024 (effective 23 July 2024): STCG under Section 111A is 20% for listed equity held under 12 months; LTCG under Section 112A is 12.5% on gains exceeding ₹1.25 lakh for equity held over 12 months. These same rates apply to equity mutual funds at the point of unit redemption.

Does a mutual fund investor pay tax when the fund manager rebalances internally?

No. Internal rebalancing by the fund manager creates no tax event for the unit holder. NAV adjusts to reflect internal gains and losses, but your personal tax liability only arises when you redeem, switch, or withdraw units.

How does high portfolio churn in PMS affect my tax liability?

Frequent trading generates short-term capital gains taxed at 20%, eroding the compounding base year after year. A PMS with 50% annual churn and mostly STCG will almost always deliver weaker post-tax returns than a comparable low-churn strategy or mutual fund with equivalent gross returns.

What tax documents does a PMS provider issue for ITR filing?

Providers typically furnish an annual portfolio statement, a transaction-wise gain/loss report, dividend and interest income statements, and audit-related certificates. You need all of these to accurately report capital gains in your ITR — engage a CA familiar with securities taxation to file correctly.