SEBI's introduction of the Specialized Investment Fund (SIF) framework, effective April 1, 2025, created a genuine new choice. SIF fills the gap between regular mutual funds and Portfolio Management Services (PMS) — but the two structures differ sharply on minimum investment, portfolio ownership, tax treatment, and customisation levels. Picking the wrong one can mean unnecessary tax drag, locked capital, or simply paying for flexibility you don't need.

This article breaks down exactly how SIF and PMS compare, who each structure suits, and how to think about using them together.

Key Takeaways

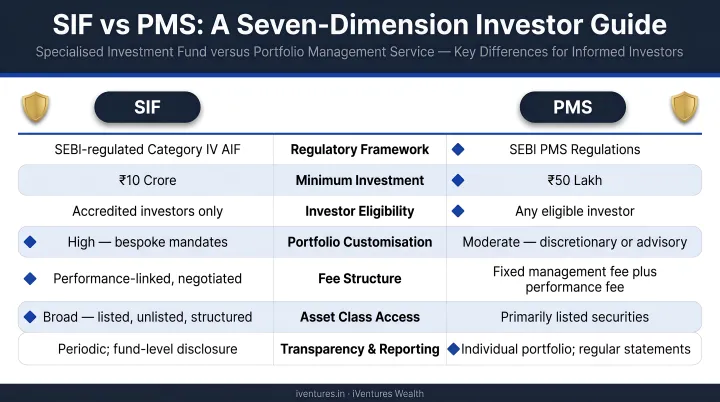

- SIF requires ₹10 lakh minimum per PAN; PMS requires ₹50 lakh as per SEBI regulations

- SIF is a pooled, NAV-based vehicle — PMS gives you direct demat ownership of every security

- SIF enables unhedged derivative exposure up to 25% of net assets; standard mutual funds cannot do this

- Tax efficiency favours SIF: capital gains apply at redemption, not on individual portfolio trades

- Both are SEBI-regulated; the right choice depends on your capital size, customisation needs, and tax position

SIF vs PMS: Quick Comparison

The table below maps the seven most decision-relevant dimensions side by side — from entry thresholds and ownership structure to tax treatment and regulatory oversight.

| Feature | SIF | PMS |

|---|---|---|

| Minimum Investment | ₹10 lakh per PAN (across all strategies) | ₹50 lakh per client* |

| Portfolio Structure | Pooled, unitised — investors hold NAV-based units | Segregated — investor directly owns securities in their demat account |

| Tax Treatment | Capital gains apply only at unit redemption | Each trade by the portfolio manager triggers a capital gains event for the investor |

| Strategy Flexibility | Long-short strategies; unhedged derivatives up to 25% of net assets | Concentrated, bespoke mandates; stock exclusions permitted |

| Liquidity | Open-ended: redemption with up to 15 working days notice; close-ended SIFs listed on exchanges | Depends on underlying securities and PMS agreement terms |

| Transparency | NAV published; ISID offer documents; dedicated SIF website required | Periodic statements (typically monthly); no pooled NAV |

| Regulatory Framework | SEBI Mutual Funds framework (Chapter VI-C) | SEBI (Portfolio Managers) Regulations, 2020 |

*PMS minimum per SEBI (Portfolio Managers) Regulations, 2020.

The sections below unpack each of these dimensions in detail — starting with where the two structures diverge most sharply: ownership, tax treatment, and investment minimums.

What Is a Specialized Investment Fund (SIF)?

SEBI created SIF under the mutual fund regulatory framework through the SEBI (Mutual Funds) (Third Amendment) Regulations, 2024, with detailed operating rules issued on February 27, 2025 and the framework made effective from April 1, 2025. SEBI's rationale: a gap had emerged between mutual funds and PMS in terms of portfolio flexibility.

What Makes SIF Different from a Regular Mutual Fund

The single most important distinction is derivative flexibility. SIF strategies can take unhedged positions in permissible exchange-traded derivatives up to 25% of net assets — for purposes beyond hedging or rebalancing. This enables:

- Equity long-short strategies — profiting from both rising and falling positions

- Sector rotation strategies with derivative overlays

- Hybrid long-short approaches combining equity and derivative exposure

No standard mutual fund category permits this. For investors, that translates to access to return strategies previously available only through PMS or AIFs.

Who Can Launch a SIF

SEBI's eligibility criteria act as a quality filter. AMCs can qualify through two routes:

- Route 1: Mutual fund operating for at least 3 years with average AUM of at least ₹10,000 crore in the preceding 3 years

- Route 2: Appoint a SIF CIO with at least 10 years' fund management experience and ₹5,000 crore average AUM, plus an additional fund manager with 3 years' experience and ₹500 crore AUM

In practice, only established AMCs with a verifiable track record can offer SIF products — the eligibility bar itself serves as a quality filter for investors.

Investor Protections Built In

SIF operates under the same oversight framework as mutual funds:

- Investment Strategy Information Document (ISID) required for each strategy

- Mandatory separate brand name, logo, and dedicated website or webpage

- Redemption notice periods capped at 15 working days

- SEBI oversight under the mutual fund regulatory umbrella

Who Should Consider SIF

Those protections make SIF a credible option for investors who want exposure to sophisticated strategies without stepping into PMS territory. The ideal SIF investor has ₹10–50 lakh in investable surplus and wants access to strategies like long-short or derivatives-based hedging — within a familiar regulated structure, at a lower capital commitment than PMS requires.

SIF works well as a satellite allocation: a tactical layer added on top of a core mutual fund portfolio to access alpha strategies, without requiring ₹50 lakh or the bespoke mandate of PMS.

Accredited investors are exempt from the ₹10 lakh minimum, making the entry point even more flexible for qualifying individuals.

What Is Portfolio Management Services (PMS)?

PMS is a personalised investment service where a SEBI-registered portfolio manager constructs and manages a portfolio — stocks, bonds, or other securities — directly in the investor's own demat account. There is no pooling. Each investor's portfolio is segregated, independently operated, and built around a tailored mandate. SEBI mandates a minimum investment of ₹50 lakh.

Three Types of PMS Mandates

- Discretionary: Portfolio manager has full authority to buy and sell — the most common and actively managed form

- Non-Discretionary: Manager recommends; investor approves before execution

- Advisory: Manager advises only; investor executes independently

Discretionary PMS dominates the market and is what most HNIs engage with when they seek a "managed portfolio" experience.

The Core Benefit: Direct Ownership

Direct demat ownership is what structurally separates PMS from every pooled product. It means:

- Exclude specific stocks from your portfolio (competitor holdings, sector conflicts, promoter-held shares)

- Pledge holdings as collateral for other financial needs

- Full estate transparency — portfolio is visible in your own demat account, not wrapped inside a fund structure

This level of personalisation is structurally impossible in a pooled vehicle.

Tax Complexity in PMS

Because the investor directly owns the securities, every buy or sell decision by the portfolio manager triggers a capital gains computation in the investor's hands. Each transaction carries a tax event — short-term gains taxed at 20% under Section 111A and long-term gains (after 12 months for listed equities) taxed at 12.5% under Section 112A above ₹1.25 lakh, per post-Budget 2024 rates.

PMS investors typically deal with far more complex annual tax filings than mutual fund or SIF investors. Working with a tax adviser and using a consolidated capital gains statement is a practical necessity, not an afterthought.

At iVentures Wealth, we help PMS clients navigate this complexity — providing capital gains summaries, dividend tracking, and guidance on working with their chartered accountants — so the reporting burden doesn't overshadow the investment strategy.

Who Should Consider PMS

Once you understand the reporting demands, the question becomes whether the structural benefits justify them. For the right investor, they do. PMS suits HNIs with ₹50 lakh or more who need a concentrated, bespoke portfolio built around specific goals, risk preferences, and exclusion requirements — and who can manage the tax complexity that direct ownership brings.

Scenarios where PMS adds distinct value that SIF simply cannot replicate:

- Business founders wanting to avoid competitor stock exposure

- CXOs with compliance-driven restrictions on certain sector securities

- Investors who prefer 15–25 high-conviction names without dilution from pooled diversification constraints

- Situations where pledging portfolio holdings as collateral is operationally necessary

SIF vs PMS: Which Should You Choose?

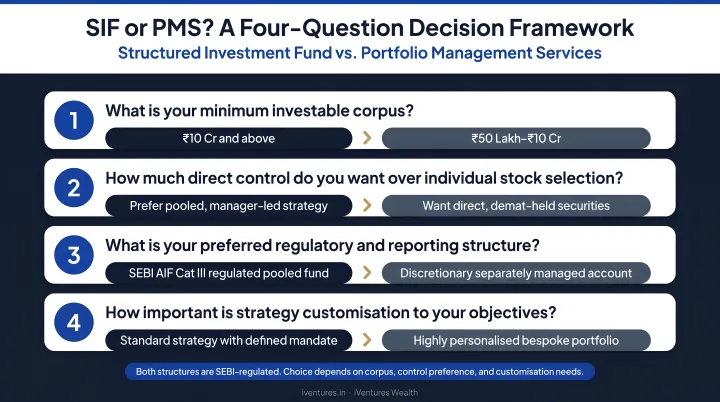

The choice comes down to four honest questions:

- What is my investable surplus? ₹10–50 lakh points toward SIF. Above ₹50 lakh opens both options.

- How much customisation do I need? Advanced-but-standardised strategies work in SIF. Fully bespoke mandates require PMS.

- How tax-sensitive am I? SIF's tax deferral to redemption is meaningfully more efficient than PMS's per-trade gains.

- What transparency format do I prefer? Daily NAV reporting versus periodic portfolio statements.

Choose SIF When:

- Investable amount is ₹10–50 lakh

- Advanced strategies (long-short, derivatives) are desired without a ₹50 lakh commitment

- Tax efficiency and pooled diversification are priorities

- The regulatory safety net of the mutual fund framework is important

Choose PMS When:

- Investable amount is ₹50 lakh or above

- A fully customised, concentrated portfolio is required

- Direct demat ownership matters — for pledging, estate transparency, or stock exclusions

- The investor has advisory support to manage per-trade tax implications

Can You Hold Both?

For HNIs and UHNIs managing larger portfolios, the answer is yes. SIF works well as a tactical, strategy-diversified component; PMS handles the bespoke core allocation. Each serves a distinct purpose — and a portfolio structured around both can be more resilient than one built around either alone.

This is where a SEBI-registered, conflict-free investment adviser adds real value. A fiduciary adviser evaluates both SIF and PMS against your overall portfolio, wealth stage, and goals — without being commercially steered toward either.

iVentures Wealth takes this approach across its open-architecture advisory for UHNIs, family offices, CXOs, and corporates. Product selection is driven by suitability, not distribution incentives.

Conclusion

Choosing between SIF and PMS comes down to where you are in your wealth journey — your capital size, customisation requirements, tax situation, and how much transparency you need from your portfolio manager.

SIF democratises institutional strategies for mass-affluent investors. PMS delivers genuine bespoke ownership for committed HNIs. Both are SEBI-regulated, both serve sophisticated investors, and in many portfolios, they work well in combination rather than competition.

The right answer depends on an honest assessment of capital, goals, and complexity tolerance. That assessment is best made with a fiduciary adviser — one who holds SEBI registration, operates on an open-architecture model, and has no incentive to favour one structure over the other. The structure that fits your situation is the right one; finding it just requires the right conversation.

Frequently Asked Questions

Which is better, SIF or PMS?

Neither is universally superior. SIF suits investors with ₹10–50 lakh who want advanced strategies within a tax-efficient, pooled structure. PMS is better suited to those with ₹50 lakh+ who need full portfolio customisation and direct demat ownership. Your investable surplus and need for customisation are the two most practical deciding factors.

Is SIF a good investment?

SIF can be a strong choice for eligible investors who want access to sophisticated strategies — such as equity long-short — within the regulatory safety of the mutual fund framework. Whether it fits your portfolio depends on your risk tolerance and how much you have available to invest beyond standard mutual funds.

What is the minimum investment for SIF vs PMS?

SEBI mandates a minimum of ₹10 lakh per PAN for SIF investments, while PMS requires a minimum of ₹50 lakh per client under the SEBI Portfolio Managers Regulations, 2020. This ₹40 lakh gap makes SIF the practical first step for investors who have outgrown standard mutual funds but aren't yet at PMS thresholds.

How is taxation different between SIF and PMS?

SIF follows mutual fund taxation rules — capital gains apply only when the investor redeems units. PMS triggers capital gains on every trade the manager executes within the investor's portfolio, creating more frequent and complex tax obligations.

Can I hold both SIF and PMS in my portfolio?

Yes. HNIs and UHNIs often hold both — using SIF for tactical strategy diversification alongside a core PMS allocation. The two products complement each other well when sized according to your liquidity needs and customisation requirements.

Who manages a SIF vs a PMS?

SIFs are managed by SEBI-registered AMCs that meet strict eligibility criteria — operating within the mutual fund framework with institutional-grade oversight. PMS is managed by a SEBI-registered portfolio manager who runs a segregated, individualised portfolio specifically for each client.