That's where goals-based investing (GBI) changes the conversation. Rather than measuring success against the Nifty 50 or a blended benchmark, GBI measures success by one thing: whether your capital funds each specific goal, on time, with high confidence.

This article explains what GBI is, how it differs from traditional portfolio management, the five-step process for implementing it, and the factors that determine whether it works.

Key Takeaways

- Goals-based investing builds separate sub-portfolios for each life goal, each with its own timeline, target corpus, and risk level.

- Success means funding each goal on time, not outperforming a market index.

- A "bucket" structure matches investment instruments to goal timelines and priority levels.

- Essential goals (retirement, education) get conservative allocations; aspirational goals can carry more risk.

- Annual reviews track progress against goal-funding milestones, not market benchmarks.

What Is Goals-Based Investing?

Morningstar defines goals-based investing as a framework that maximises the probability of achieving personal financial goals rather than beating a benchmark. Academically, the Journal of Banking & Finance frames it more precisely: risk in GBI is defined as the probability of not meeting a financial goal — not portfolio volatility.

In practice, this shifts the central question from "Is my portfolio up this year?" to "Am I on track to fund my retirement / my child's education / my business succession?" The portfolio is built to answer the latter.

How GBI Differs from Related Concepts

GBI is sometimes confused with two adjacent frameworks:

- Liability-driven investing (LDI): Used by pension funds to match assets against institutional liabilities. GBI applies similar logic to personal financial goals — but the goals are yours, not a fund's obligations.

- Simple goal-setting in financial planning: Stating goals is not the same as integrating them into portfolio construction. In GBI, each goal's timeline, required corpus, and priority level directly shape the investment mix — not the other way around.

That distinction becomes consequential when wealth is spread across personal accounts, family trusts, corporate entities, and NRI portfolios. A single blended portfolio cannot simultaneously serve:

- A 3-year liquidity need

- A 12-year education goal

- A 25-year legacy objective

Each requires a different risk posture — which is exactly what GBI is structured to address.

Goals-Based Investing vs. Traditional Portfolio Management

Goals-based investing (GBI) and traditional portfolio management diverge at a fundamental level — in how risk is defined, how success is measured, and how capital is allocated. For affluent investors with real obligations, that divergence has direct financial consequences.

Risk Is Defined Differently

Traditional investing measures risk as portfolio volatility — standard deviation of returns. GBI redefines risk as the probability of failing to fund a specific goal. For an affluent investor with real obligations — a child's overseas education in four years, a retirement target in twelve — the traditional definition is an abstraction. Goal-failure is not.

Ashvin Chhabra's 2005 framework in the Journal of Wealth Management makes this explicit: for individual investors, risk allocation should precede asset allocation. Three distinct risk tiers drive that allocation: personal risk (lifestyle protection), market risk (wealth growth), and aspirational risk (legacy, philanthropy).

Success Is Measured Differently

A benchmark-relative investor who loses 15% while the market falls 30% may feel satisfied. A goals-based investor approaching retirement who loses 15% has suffered a real setback — regardless of what the index did.

This is particularly consequential for founders and families who have concentrated wealth tied to a business exit, property sale, or liquidity event. In those situations, sequence-of-returns risk is personal, not statistical.

Asset Allocation Is Goal-Specific

| Goal Horizon | Typical Allocation Approach |

|---|---|

| 0–4 years (near-term) | Liquid funds, short-duration debt, fixed deposits |

| 5–10 years (medium-term) | Balanced mix of debt and equity |

| 10+ years (long-term) | Higher equity allocation for compounding |

This is structurally different from building one portfolio around an abstract risk-tolerance score and applying it uniformly. That structure, however, only holds if investors stay invested long enough for it to work — which is where behavior becomes as important as allocation.

The Behavioral Advantage

Richard Thaler's mental accounting research — published in Marketing Science (1985) and Journal of Behavioral Decision Making (1999) — shows that people who mentally label money for specific purposes make more disciplined decisions about it. Applied to investing, goal-specific buckets reduce the temptation to exit long-horizon positions during short-term market stress.

This behavioral pattern holds across markets. Vanguard's 2020 study during the COVID crash found that fewer than 0.5% of investors moved fully to cash between February and May 2020 — and more than 84% of those who did exit were worse off by May 31. Goal-labeled buckets gave investors a reason to stay put when volatility peaked.

How Goals-Based Investing Works: A Step-by-Step Process

GBI works by breaking a single portfolio into multiple goal-specific sub-portfolios. Each is optimised for its own timeline and required probability of success. Together, they constitute the investor's total wealth strategy.

Step 1: Identify and Articulate Your Financial Goals

The process begins with structured goal-mapping. Goals are classified into a three-tier hierarchy:

- Essential needs — retirement corpus, emergency reserves, income replacement

- Lifestyle wants — children's education, vacation property, business continuity funds

- Aspirational wishes — legacy wealth, philanthropic endowments, intergenerational trusts

A rigorous goal-mapping exercise also captures what you want to avoid — business illiquidity at exit, wealth erosion during a career transition, children inheriting complexity without structure. These downside priorities shape conservative allocations just as much as upside aspirations.

Morningstar's Goal Bridge research found that 76% of investors changed at least one of their top three goals after completing a structured goal-discovery exercise — suggesting that what investors initially state as priorities often shifts once goals are mapped systematically.

Step 2: Assign Timelines and Probability of Success

Each goal gets two parameters: a time horizon (e.g., 3 years, 12 years, 25 years) and a required probability of success — the confidence level with which it must be funded. Higher-priority goals demand higher confidence: an education corpus due in four years warrants a near-certain outcome, meaning a conservative, low-volatility allocation. An aspirational legacy goal at a 25-year horizon can accept a lower probability threshold — and therefore a more aggressive investment mix.

These thresholds aren't standardised across the industry — they depend on the individual's financial position, life stage, and the consequence of shortfall for each specific goal.

Step 3: Calculate the Inflation-Adjusted Corpus Required

Each goal's required capital is calculated in today's terms and then inflation-adjusted to its future value. Underestimating this figure is where most plans quietly break down.

MoSPI's January 2026 CPI data shows headline CPI at 2.75% — but education-specific inflation runs higher:

- Secondary education: 4.14%

- Higher education: 3.59%

- Education services overall: 3.35%

A family planning for a child's undergraduate education abroad in 10 years cannot use headline CPI to estimate the corpus. The real cost gap compounds significantly over a decade.

Step 4: Allocate Assets to Goal-Specific Buckets

Once the corpus and timeline are defined, each bucket gets an instrument-matched allocation.

In India's regulated investment universe, this typically includes:

- Short-term buckets (0–4 years): Liquid funds (securities maturing within 91 days per AMFI), ultra-short duration funds, short-duration corporate bond funds, fixed deposits

- Medium-term buckets (5–10 years): Balanced allocation across debt and equity mutual funds, corporate bonds

- Long-term buckets (10+ years): Equity-oriented portfolios including direct equity, ELSS (minimum 80% in equities with 3-year lock-in), and AIF/PMS allocations

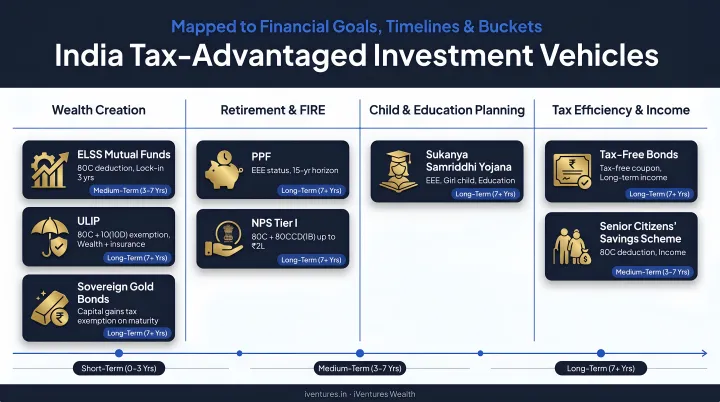

Tax-advantaged vehicles can be mapped to appropriate goals for enhanced efficiency:

- PPF (15-year maturity) for long-horizon wealth accumulation with tax-exempt returns

- ELSS for equity exposure with Section 80C benefit on contributions up to ₹1.5 lakh

- NPS for retirement corpus with additional deduction under Section 80CCD(1B)

- Sovereign Gold Bonds (8-year tenor, exit from year 5) for inflation protection within a goal bucket

- GIFT City-domiciled funds for NRI/OCI clients who want USD-denominated allocations without complex currency hedging

For clients with multi-entity wealth — personal, corporate, trust — this allocation step becomes significantly more complex. Goal-buckets need to be mapped across entities, post-tax returns optimised (LTCG at 12.5% above ₹1.25 lakh and STCG at 20% for equity transfers after July 23, 2024), and instruments selected without the product-distribution conflicts that distributors or bank relationship managers typically carry. This is where an independent, SEBI-registered adviser like iVentures Wealth provides a structurally different kind of guidance.

Step 5: Monitor Progress and Rebalance Periodically

Once allocations are in place, the work shifts to monitoring — because both life and markets move. A business exit, an inheritance, a new dependent, or a career transition can fundamentally alter the capital picture, and market movements continuously affect each bucket's funding status.

Each goal-bucket is reviewed against its funding milestone, not against a market benchmark. A bucket that was 85% funded toward its target corpus two years ago and is now 78% funded requires a different response than a bucket that's ahead of schedule.

Vanguard's research supports an annual rebalancing schedule as an optimal baseline, with additional out-of-cycle reviews triggered by significant life changes or portfolio drift beyond defined thresholds.

Key Factors That Influence a Goals-Based Investment Strategy

Several variables determine whether the framework delivers on its promise.

Four factors carry the most weight:

- Timeline and priority level: The shorter the horizon and the higher the stake, the more conservative the allocation must be. A 15% market correction in year 3 of a 3-year goal can permanently impair that goal. The same correction in year 3 of a 20-year goal is a rounding error.

- Inflation-adjusted required returns: Each bucket must generate a return that covers goal-specific inflation, not just CPI. The gap between headline CPI and education inflation is material over 10–15 years — and that gap compounds.

- Competing goals against finite capital: When the total capital required to fund all goals simultaneously exceeds available assets, intuition is a poor guide. A structured prioritisation framework — essential goals protected first, aspirational goals sized to residual capital — is the only way to make these trade-offs objectively.

- Tax efficiency by vehicle: Using the right instrument for the right goal directly affects the corpus available at the target date. After the Finance Act 2023, specified mutual funds (those with 35% or less in domestic equities under Section 50AA) are taxed as short-term capital gains regardless of holding period. For HNIs in higher tax brackets, this changes the instrument calculus for medium-term debt allocations meaningfully.

Common Misconceptions About Goals-Based Investing

Three beliefs about goals-based investing tend to hold investors back — or lead them to apply it poorly.

"GBI Means Accepting Below-Market Returns"

This gets the framework backwards. GBI matches risk to timeline and priority; it doesn't cap returns. A long-horizon aspirational bucket may hold a predominantly equity portfolio with aggressive growth targets. J.P. Morgan Private Bank's growth bucket, for example, includes private equity, public equity, hedge funds, and levered strategies. Indian UHNI portfolios structured on the same logic similarly run Category III AIFs, PMS equity sleeves, and offshore fund allocations in their long-horizon buckets — all positioned for growth, not capital preservation.

"GBI Is Only for Retirement Planning"

Retirement is often the largest goal, but the framework applies equally to education funding, business succession, estate planning, and philanthropic objectives.

For UHNI families managing assets across personal accounts, family trusts, and operating businesses, a systematic goals-based allocation across the entire wealth structure — not just the retirement account — produces coherent decisions at the whole-balance-sheet level. That is where the real structural advantage sits.

"GBI Works for Every Investor"

Not quite. It is best suited to investors with multiple distinct goals, different time horizons, and genuine trade-off decisions to navigate. A single-goal investor with a straightforward financial profile may find simpler portfolio management sufficient.

One limitation is also worth naming directly: aspirational goals with very short timelines and insufficient capital are not fundable within GBI. They must be deferred, resized, or accepted as high-risk bets — and a good advisor will say so plainly rather than paper over the gap.

Frequently Asked Questions

How is goals-based investing different from traditional portfolio management?

Traditional investing uses a single portfolio optimised for market-relative returns, measured against a benchmark. Goals-based investing splits assets into goal-specific sub-portfolios, each designed to fund a particular objective within a defined timeline and probability of success. Risk is defined as goal-failure, not portfolio volatility.

Can I pursue multiple financial goals simultaneously with this approach?

Yes — GBI is specifically designed for investors with multiple goals. Each goal receives an appropriately matched investment strategy rather than forcing a single allocation to serve purposes with conflicting timelines and risk requirements.

What happens to my goals-based portfolio during a market crash?

Short-term goal-buckets are structured in low-volatility instruments and are largely insulated from equity market crashes. Long-horizon buckets carry higher equity exposure but have sufficient time to recover, reducing the behavioural pressure to exit at market lows — typically the most damaging decision an investor can make.

How often should I review and rebalance a goals-based portfolio?

An annual formal review aligned to significant life events (salary change, business exit, new dependent, tax-law changes) is an appropriate baseline. Each goal-bucket should be assessed against its funding milestone, not against a market benchmark.

Is goals-based investing suitable for NRIs and investors with complex multi-entity financial structures?

GBI is particularly well-suited to NRIs and UHNI families with assets across multiple entities. The framework accommodates different regulatory, tax, and repatriation constraints — NRE/NRO structures, FEMA compliance, DTAA optimisation, and GIFT City allocations — across jurisdictions within a single goal-mapped plan.

Do I need a SEBI-registered investment adviser to implement goals-based investing?

For complex multi-goal situations, a fiduciary adviser without product-selling incentives is the right choice. Under Regulation 15 of the SEBI Investment Adviser Regulations 2013, a registered adviser cannot earn commissions on recommendations — removing the conflicts that make goal-bucket construction through distributors unreliable.