Introduction

Indian investors, NRIs, and OCIs earning income from U.S. stocks, interest, or royalties face a frustrating reality: the same money gets taxed twice — once by the IRS, and again by Indian tax authorities. The Foreign Tax Credit, claimed via Form 1116, directly addresses this by letting you offset your U.S. tax liability with taxes already paid to a foreign country on a credit basis.

That said, the credit you actually recover depends on far more than just how much foreign tax you paid. Income categorisation, deduction apportionment, treaty rate ceilings, and carryover tracking all interact in ways that can either maximise or significantly reduce your benefit. A single miscategorisation can distort the credit in both directions.

This article covers:

- Who qualifies and which foreign taxes are eligible

- How to complete Form 1116, step by step

- The key variables that affect your final credit amount — and the three mistakes that most commonly eliminate it

Key Takeaways

- Form 1116 reduces U.S. tax liability dollar for dollar for qualifying foreign income taxes paid or accrued

- Only income taxes (or taxes in lieu of income taxes) qualify — VAT, social insurance, and penalties do not

- The credit cannot exceed your U.S. tax on the same foreign income, with the limitation formula built directly into Form 1116

- Claiming the Foreign Earned Income Exclusion on income bars you from also applying the Foreign Tax Credit to that same income

- Unused credits carry back one year and forward up to ten years through Form 1116 Schedule B

What Is the Foreign Tax Credit and When Does Form 1116 Apply?

The Foreign Tax Credit (FTC) is a non-refundable U.S. tax credit that eliminates or reduces double taxation when the same income is taxed by both a foreign country and the U.S. Unlike a deduction, which merely lowers taxable income, the FTC reduces tax owed dollar for dollar, making it a considerably larger benefit.

Form 1116 is required when an individual, estate, or trust claims this credit. The one exception: you can bypass Form 1116 and claim the credit directly on Form 1040 only when all three of the following conditions apply:

- Total creditable foreign taxes are below $300 (single) or $600 (married filing jointly)

- All foreign-source income is passive category

- All income and foreign tax are reported on a qualified payee statement such as Form 1099-DIV or 1099-INT

If any one of those conditions fails, Form 1116 is mandatory. (Corporations filing for the same credit use Form 1118, which is outside the scope of this guide.)

Form 1116 vs. Form 67: Which Form Goes Where

For Indian tax residents — including NRIs earning U.S.-source income — both forms may come into play, but they serve opposite directions of the same double-taxation problem.

| Form | Filed With | Purpose |

|---|---|---|

| Form 1116 | U.S. tax return | Credits foreign taxes paid against U.S. tax liability |

| Form 67 (India Rule 128) | Indian tax return | Credits foreign taxes (including U.S. withholding) against Indian tax liability |

These are separate obligations. Filing one does not satisfy the other, and the applicable form depends on which country's return is being filed and the taxpayer's residential status for that year.

Eligibility: Who Can Use Form 1116 and What Foreign Taxes Qualify?

Who Is Eligible

According to IRS Publication 514, the following taxpayers may claim the FTC:

- U.S. citizens — regardless of where they live

- Resident aliens — generally for taxes on income received during their period of resident-alien status

- Nonresident aliens — only in specific circumstances: bona fide Puerto Rico residents for the full tax year, or NRAs paying foreign tax on income effectively connected with a U.S. trade or business

NRIs and OCIs holding U.S. investments as non-resident aliens typically do not file Form 1116 themselves. The exception applies when they are also subject to U.S. income tax on that same income — through treaty positions or effectively connected income (ECI).

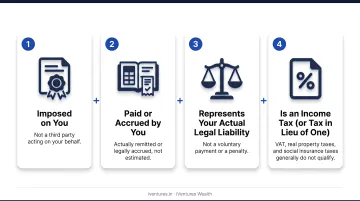

Four Tests a Foreign Tax Must Pass

The IRS requires every qualifying foreign tax to meet all four of the following conditions:

- Imposed on you — not a third party acting on your behalf

- Paid or accrued by you — actually remitted or legally accrued, not estimated

- Represents your actual legal liability — not a voluntary payment or a penalty

- Is an income tax or a tax in lieu of an income tax — VAT, real property taxes, and social insurance taxes generally do not qualify

Treaty Rate Ceiling Under the India-US DTAA

This matters for Indian investors receiving U.S.-source income. Under the India-US Double Tax Avoidance Agreement, the maximum withholding rates are:

| Income Type | Treaty Rate (India-US DTAA) | U.S. Statutory Rate (No Treaty) |

|---|---|---|

| Portfolio dividends (individual investor) | 25% | 30% |

| Direct dividends (10%+ voting stock) | 15% | 30% |

| Interest (general) | 15% | 30% |

| Interest (bank/financial institution loan) | 10% | 30% |

| Equipment royalties | 10% | 30% |

| Copyright and other royalties | 15% | 30% |

Only the treaty-permitted portion is creditable. If more was withheld than the treaty allows, the excess is refundable from the source country — not eligible as a foreign tax credit.

The FEIE Interaction

The FEIE interaction is a separate eligibility hurdle from the treaty rules above. If you have already excluded income under the Foreign Earned Income Exclusion (FEIE) or Foreign Housing Exclusion, no FTC is allowed on that excluded income. Attempting to claim both triggers IRS scrutiny and can result in revocation of the exclusion election, which generally cannot be re-elected for five years without IRS approval.

NRIs and OCIs managing cross-border portfolios across India and the U.S. often benefit from working with a specialist adviser before filing. Determining residency status, treaty applicability, and the right credit strategy across jurisdictions is where firms like iVentures Wealth — focused on DTAA structuring and cross-border investment advisory — provide the most value.

How to Claim the Foreign Tax Credit Using Form 1116

Form 1116 has four parts and must be completed separately for each income category. If you have both passive income (dividends) and general category income (wages from foreign employment), you need two separate copies of the form.

Step 1: Gather Documents and Identify Qualifying Foreign Tax Paid

Collect proof of foreign tax paid:

- Form 1099-DIV — Box 7 shows foreign tax paid on dividends

- Form 1099-INT — for foreign tax withheld on interest

- Brokerage year-end tax statements — typically summarize total foreign tax across positions

- TDS certificates or Form 26AS equivalents — for Indian-source income

Convert all foreign currency amounts to U.S. dollars at the exchange rate in effect on the date the tax was paid or withheld, not the year-end rate.

Step 2: Determine Your Income Category (The "Basket")

Form 1116 requires income to be separated into specific categories. Most individual investors use two:

- Passive Category — dividends, interest, royalties, and most capital gains from foreign sources

- General Category — foreign wages, self-employment income, and most other business income

Each category gets its own Form 1116, and the credit limitation is calculated independently per basket. Losses in one category cannot offset income in another. Placing income into the wrong basket is one of the most common errors that inflates or deflates the final credit.

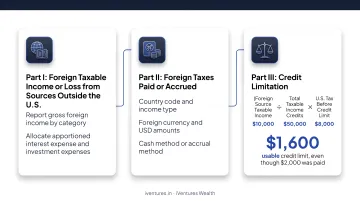

Step 3: Complete Parts I–III of Form 1116

Note: The current 2025 Form 1116 sequences the parts as follows — Part I covers foreign income and deductions, Part II covers foreign taxes paid or accrued, Part III computes the credit limitation.

Part I — Foreign Taxable Income or Loss from Sources Outside the U.S. Report gross foreign income in the applicable category and allocate related deductions (such as apportioned interest expense and investment expenses) against foreign-source income. This step reduces your net foreign income used in the credit limitation formula, and filers frequently underestimate it.

Part II — Foreign Taxes Paid or Accrued For each country, enter:

- Country code and income type

- Foreign tax paid in both foreign currency and USD

- Whether you're using the cash method (taxes actually paid) or accrual method

Once the accrual method is elected, it applies to that year and all future years unless the IRS consents to a change.

Part III — Credit Limitation The IRS limits the credit to U.S. tax attributable to foreign income, calculated as:

(Foreign Source Taxable Income ÷ Total Taxable Income) × U.S. Tax Before Credits = Credit Limit

Example: If your foreign-source taxable income is $10,000 (converted from foreign currency at the payment-date exchange rate) and total taxable income is $50,000, and your U.S. tax before credits is $8,000:

($10,000 ÷ $50,000) × $8,000 = $1,600 credit limit

Even if you paid $2,000 in foreign taxes, only $1,600 is usable in the current year.

Step 4: Calculate the Allowable Credit in Part IV and Handle Any Excess

Part IV computes the final allowable credit as the lesser of the foreign tax paid and the credit limitation from Part III. That credit flows to Form 1040 Schedule 3, reducing your U.S. tax liability directly.

If foreign tax paid exceeds the credit limitation, you don't lose the excess:

- Carry it back to the prior tax year by filing a Form 1040-X (amended return)

- Carry it forward for up to 10 years

Form 1116 Schedule B is used to track these carryover amounts. It must be completed and attached for any year with a prior-year or current-year carryover.

Key Variables That Affect Your Foreign Tax Credit Amount

Two taxpayers with identical gross foreign income can end up with meaningfully different credits. These four variables explain why.

Income Category Separation Because the limitation is computed per basket, placing income in the wrong category can reduce or eliminate the credit for that basket. Passive income inadvertently reported in the general basket distorts both calculations simultaneously.

Deduction Apportionment The IRS requires interest expenses and certain other deductions to be apportioned between U.S. and foreign-source income. This reduces the net foreign income figure in the limitation formula. In practice, filers with significant mortgage interest often find their foreign income basket reduced well before the credit limit is calculated — sometimes by more than they anticipate.

Treaty Rate vs. Statutory Rate Under the India-US DTAA, only the treaty-permitted tax qualifies as creditable — not the full amount withheld. Consider a common scenario:

- U.S. broker withholds 30% on dividends

- NRI qualifies for the 25% treaty rate under the India-US DTAA

- Only the 25% is creditable on Form 1116

- The remaining 5% must be reclaimed from the IRS as a refund — not a credit

Carryover Position Taxpayers with accumulated prior-year unused credits can apply them in the current year if the credit limit permits. The 10-year carryforward window means strategic timing of foreign income recognition can unlock large accumulated credits. Timing a liquidity event or lump-sum foreign income in a year when the credit limit is high enough to absorb carryovers can meaningfully reduce overall tax liability across both jurisdictions.

Common Mistakes When Filing Form 1116

Claiming Both the FTC and the FEIE on the Same Income

Many U.S. citizens living abroad exclude income under the Foreign Earned Income Exclusion and then attempt to also claim a foreign tax credit on that same excluded income. The IRS explicitly prohibits this. Worse, claiming the credit can cause the exclusion election to be considered revoked — and you generally cannot re-elect the exclusion for five tax years without IRS approval.

Skipping Form 1116 When the Simplified Election Doesn't Apply

Some filers assume they can always bypass Form 1116 and claim the credit directly on Form 1040. The simplified election is only valid when all three conditions are met: taxes below $300/$600, only passive income, all reported on a qualified payee statement. If you don't qualify and claim it anyway, you've understated your tax liability — and the IRS may issue a CP2000 notice or disallow the credit entirely.

Missing Income Category Separation or Ignoring Schedule B

Two errors consistently appear together:

- Single Form 1116 for all income categories — mixing income baskets distorts the credit limitation calculation for each category

- Skipping Schedule B when carryovers exist — IRS instructions for Schedule B are clear that it must be completed and attached whenever any prior-year or current-year carryover exists

Omitting Schedule B leaves the IRS unable to verify your carryover position, which complicates future claims and can result in the credit being disallowed.

Frequently Asked Questions

What is the foreign tax credit?

The Foreign Tax Credit is a non-refundable U.S. tax credit that allows individuals to offset U.S. income tax liability by the amount of qualifying income taxes paid or accrued to a foreign country on the same income. It reduces tax owed dollar for dollar, rather than simply lowering taxable income.

Who is eligible for foreign tax credit relief?

U.S. citizens and resident aliens who paid qualifying income taxes to a foreign country or U.S. possession — and are subject to U.S. tax on that same income — are generally eligible. Nonresident aliens qualify only in narrow cases, such as bona fide Puerto Rico residents or those with income effectively connected to a U.S. trade or business.

How is the foreign tax credit calculated?

The credit equals the lesser of: (1) foreign tax actually paid, and (2) the IRS credit limitation — calculated as (Foreign Source Taxable Income ÷ Total Taxable Income) × U.S. Tax Before Credits. Any excess over the limit carries back one year or forward up to ten years.

What is the foreign tax credit in India?

In India, the Foreign Tax Credit is claimed via Form 67 under Rule 128 of the Income Tax Rules. It allows Indian tax residents to offset Indian tax liability by the amount of tax paid abroad on the same income. Indian residents with U.S.-source income may need to navigate both Form 67 and U.S. Form 1116 as entirely separate processes.

Can I claim Form 1116 if I also claim the Foreign Earned Income Exclusion?

No. You cannot claim a foreign tax credit on income you have already excluded under the FEIE. Claiming both on the same income is explicitly prohibited, and doing so can trigger revocation of the exclusion election — which cannot generally be re-elected for five years without IRS consent.

What happens to unused foreign tax credits on Form 1116?

When foreign tax paid exceeds the current-year credit limitation, unused credits can be carried back to the prior tax year via an amended Form 1040-X, or carried forward for up to ten years. All carryover amounts must be tracked on Form 1116 Schedule B, which is required whenever any prior-year or current-year carryover exists.