Introduction

Markets move. That's expected. What catches many investors off guard is how quietly those movements reshape their portfolio's risk profile — without a single deliberate decision.

Portfolio rebalancing is the process of realigning a portfolio's asset weights back to their original target allocation after market movements cause them to drift. A portfolio designed as 60% equity and 40% debt doesn't stay that way after a sustained bull run. Vanguard's long-horizon data shows that a 60/40 portfolio started in December 1989 would have reached 80% equity by December 2021 — a risk exposure shift that accumulated gradually, across three decades of unattended drift.

For HNIs, UHNIs, and affluent Indian investors managing diversified portfolios spanning equity, debt, gold, REITs, and alternatives, this drift is not a minor nuisance. It fundamentally alters the risk-return profile of a portfolio built around specific goals and a specific life stage.

This guide covers the five main rebalancing strategies professional advisors use, how to time those decisions, and the Indian tax context that shapes every execution call.

Key Takeaways

- Portfolio rebalancing restores a portfolio's original asset allocation after market-driven drift changes its risk profile

- The main approaches — calendar-based, threshold-based, constant mix, CPPI, and cash flow rebalancing — each involve different trade-offs in cost, responsiveness, and tax efficiency

- Annual reviews are a useful baseline; life stage and portfolio complexity should shape actual rebalancing frequency

- In India, equity gains held under 12 months attract 20% STCG tax; gains held over 12 months attract 12.5% LTCG tax above ₹1.25 lakh — so when you sell during rebalancing affects your tax outgo

- No single strategy is universally best; the right approach depends on goals, risk tolerance, portfolio size, and tax situation

What Is Portfolio Rebalancing?

Portfolio rebalancing is the deliberate process of buying and selling assets to bring a portfolio back to its intended allocation. If strong equity performance pushes a 60/40 portfolio to 75% equity and 25% debt, rebalancing would involve trimming equity and adding to debt until the original weights are restored.

Understanding Portfolio Drift

As equities outperform bonds during a bull run, their share of a portfolio grows automatically. The investor hasn't made a single active choice — but their exposure has shifted meaningfully. A portfolio designed for moderate risk has quietly become aggressive.

The reverse also holds. After a sharp correction, a growth-oriented portfolio can drift toward excessive conservatism — precisely when recovery-phase returns are most valuable. Vanguard's research found that a 60/40 portfolio's equity weight could range between roughly 50% and 80% without rebalancing over a multi-decade period — a 30-percentage-point swing in risk exposure.

What Rebalancing Is Not

Rebalancing is not a market timing move or a change in strategy — it is a maintenance process that keeps the existing strategy intact.

It's worth distinguishing rebalancing from two related but different activities:

- Portfolio optimisation — changing the target allocation itself (for example, shifting from 60/40 to 50/50 as retirement approaches). This updates the destination.

- Rebalancing — restoring the portfolio to its current target allocation. This keeps you on the path to wherever you've already decided to go.

One revises the plan; the other executes it.

Why Portfolio Rebalancing Is Essential for Long-Term Investors

Risk Control

An unexamined portfolio can drift substantially over a few years. The Vanguard 60/40 study illustrates this clearly: three decades of unmanaged drift moved equity exposure from 60% to 80%. For a retiree or pre-retiree, that 20-percentage-point excess equity exposure is not a theoretical concern — it directly affects downside risk during withdrawals.

A Vanguard simulation covering 2005–2014 found the non-rebalanced portfolio trailed the rebalanced portfolio by 5 percentage points after tax over that 10-year period.

Behavioural Discipline

Rebalancing enforces a systematic buy-low, sell-high behaviour without requiring the investor to predict markets. Trimming equity during a bull run and adding to debt or gold during a correction feels counterintuitive — but that is precisely what disciplined rebalancing mandates.

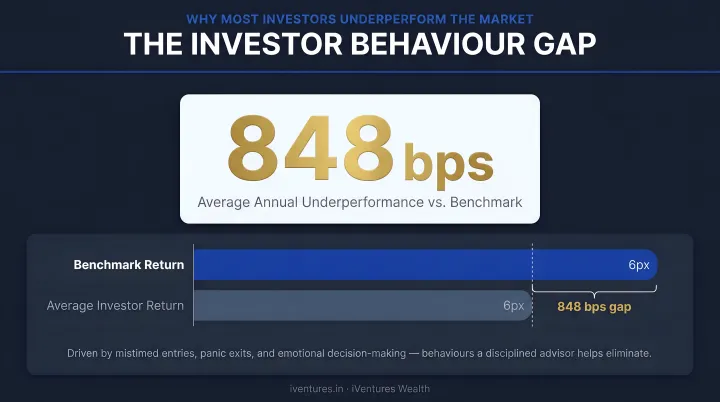

The alternative — letting emotion guide allocation — is costly. DALBAR's 2024 investor behaviour data shows that globally, the average equity investor earned 16.54% against the S&P 500's 25.02% — an 848 basis point gap driven largely by poor timing decisions.

Even more conservative estimates from CFA Institute research suggest poor timing costs investors around 1.2% per year over a decade. Across a ₹10–50 Cr portfolio, that drag compounds into a significant erosion of wealth.

The behavioural cost of inaction is consistent across markets. Key data points bear this out:

- Average investor underperforms benchmarks by 848 bps annually (DALBAR 2024)

- Poor timing costs approximately 1.2% per year over a decade (CFA Institute)

- A disciplined rebalancing process removes emotional decision-making from the equation

Life Stage and Goal Alignment

As investors move from wealth accumulation to preservation, the portfolio must evolve alongside them. A 60/40 equity-debt mix appropriate for a 38-year-old entrepreneur with strong business cash flows may be far too aggressive for the same individual at 58, approaching a business exit.

This transition is particularly consequential for UHNIs and family office clients, where the stakes — across multiple entities, geographies, and generations — are considerably higher.

At every major life transition, both steps are required: updating the target allocation to reflect the new stage, and rebalancing the portfolio to match it. Neither step alone is sufficient.

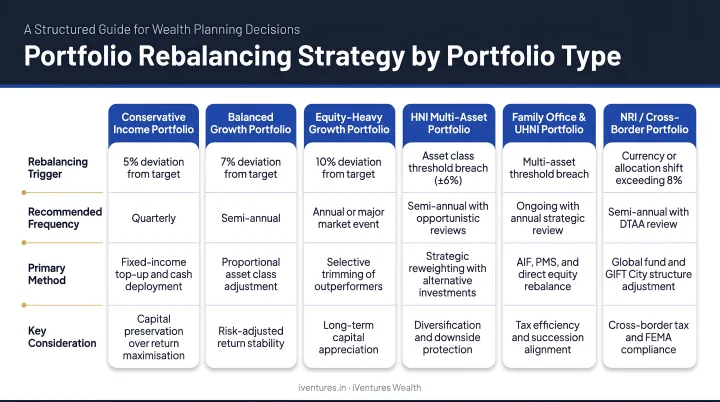

Portfolio Rebalancing Strategies Explained

No single strategy is universally superior. The right approach depends on an investor's risk tolerance, portfolio size, how actively they can monitor allocations, and their tax situation. Five main strategies are used in practice, ranging from simple calendar rules to dynamic insurance frameworks.

Calendar Rebalancing

The investor reviews and restores target allocations on a fixed schedule — monthly, quarterly, semi-annually, or annually.

Vanguard's research found annual rebalancing optimal among calendar-based methods for a 60/40 portfolio, outperforming:

- Monthly rebalancing by 21–28 basis points after costs

- Quarterly rebalancing by 10–16 basis points

More frequent rebalancing incurs higher transaction costs and more taxable events, without proportionate improvement in risk alignment.

Trade-off: Simple and low-cost, but may miss meaningful drift that occurs between review dates during sharp, fast-moving market moves.

Threshold (Corridor) Rebalancing

Instead of a fixed calendar, rebalancing is triggered only when an asset class drifts beyond a preset tolerance band from its target.

A commonly cited framework is the 5/25 rule, widely attributed to practitioner Larry Swedroe: rebalance when an asset class drifts by more than 5 percentage points in absolute terms, or 25% in relative terms from its target weight — whichever threshold is reached first.

In practice: a 10% bond allocation would trigger rebalancing if it falls below 7.5% (a 25% relative deviation), rather than waiting for a full 5-point absolute drift.

Vanguard's modelling found a 3% threshold optimal for a 60/40 portfolio when tracking error must stay within tight bounds. Broader investor guidance from Vanguard cites 5% or 10% bands as practical options depending on portfolio complexity and cost sensitivity.

Trade-off: More responsive to actual market conditions, but requires continuous monitoring to catch threshold breaches.

Constant Mix Strategy

A fixed target weight is maintained for each asset class within defined corridors. As asset prices move, the strategy automatically forces selling of overweighted assets and buying of underweighted ones.

This creates a disciplined buy-low/sell-high cycle that is systematic rather than discretionary.

Best suited for: Oscillating or mean-reverting markets, where the systematic buy-low/sell-high cycle adds clear value. In strongly trending markets — where a single asset class continues rising — the strategy may underperform, since it trims the rising asset before the trend fully plays out.

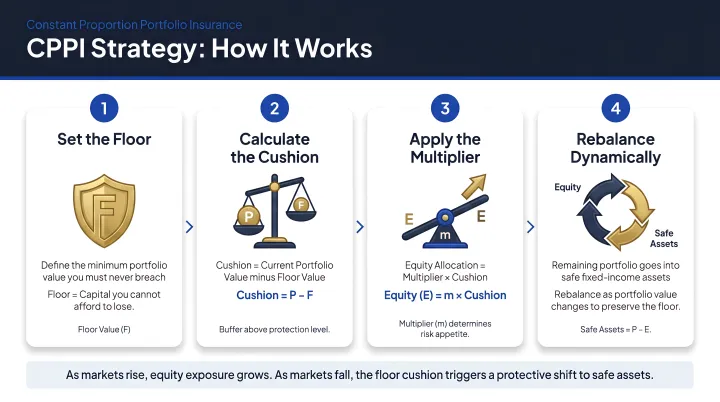

CPPI (Constant Proportion Portfolio Insurance)

CPPI is a dynamic strategy designed for investors who need downside protection but still want to participate in market upside.

The mechanics:

- Define a floor — the minimum portfolio value the investor cannot afford to lose

- Calculate the cushion = Current Portfolio Value − Floor

- Apply a multiplier to the cushion to determine equity exposure: Equity Investment = Multiplier × Cushion

- As the portfolio grows, equity exposure rises. As it falls toward the floor, equity exposure is reduced toward safer assets.

This structure suits investors with a non-negotiable capital floor — someone who cannot absorb losses beyond a defined threshold but still wants equity participation on the upside.

Who this suits:

- Investors approaching retirement who need capital preservation alongside growth participation

- Clients with a defined minimum corpus requirement — education funding for children, for example

For pre-retirement clients, iVentures Wealth applies a bucket-based approach along similar lines: de-risking into a balanced and debt mix during the five years before retirement to protect against sequence-of-returns risk.

Cash Flow Rebalancing

Instead of selling overweight assets, new contributions — SIPs, lump-sum investments — are directed toward underweight asset classes, and withdrawals are taken from overweight ones.

Key advantage: Avoids triggering capital gains tax events and minimises transaction costs. For investors with regular SIP contributions, this can be an effective ongoing correction mechanism.

Limitation: Cash flow rebalancing may be insufficient to correct large allocation drifts during periods of significant market volatility. It works best for investors with meaningful, regular contributions — not for portfolios in the distribution phase where contributions have stopped.

iVentures Wealth applies a version of this approach through what it describes as a "rule-based surplus deployment structure" — systematically directing business cash flows and investment contributions toward underallocated segments rather than triggering unnecessary rebalancing transactions.

When Should You Rebalance Your Portfolio?

Establishing the Baseline

Annual rebalancing is a well-supported starting point for most investors. Vanguard's research shows rebalancing more frequently than annually rarely improves outcomes but consistently increases costs and tax friction.

However, annual rebalancing is a floor, not a ceiling. Portfolio complexity, life stage, and market conditions all influence appropriate frequency.

Calendar vs. Threshold Triggers

| Portfolio Type | Recommended Approach |

|---|---|

| Smaller, simpler portfolios (equity + debt) | Fixed annual calendar review |

| Larger, multi-asset portfolios (equity, debt, gold, REITs, international, AIFs) | Threshold-based triggers with annual baseline |

| Investors with regular SIP contributions | Cash flow rebalancing as ongoing correction |

| Pre-retirement or distribution phase | Semi-annual or quarterly monitoring |

A hybrid approach works best: review annually, but also act when drift exceeds a defined threshold. This balances discipline with responsiveness. iVentures Wealth uses exactly this structure — quarterly scheduled reviews with continuous real-time monitoring running between them.

Life Stage Timing

- Early accumulation phase: Less frequent rebalancing is reasonable; smaller portfolios and regular contributions can naturally correct modest drift

- Mid-career wealth building: Semi-annual or quarterly reviews become appropriate as portfolio values grow and the cost of misalignment increases

- Pre-retirement and distribution phase: More frequent monitoring protects against sequence-of-returns risk — the specific danger that poor early-retirement returns permanently impair the corpus

Market Event Triggers and Behavioural Discipline

Major corrections or extended bull runs warrant an unscheduled check against thresholds. They should not trigger an abandonment of the rebalancing plan.

Market volatility is a prompt to check whether drift thresholds have been breached — not a reason to sell equities out of fear or chase them out of greed. Investors who hold that line through volatile periods consistently retain more wealth over time.

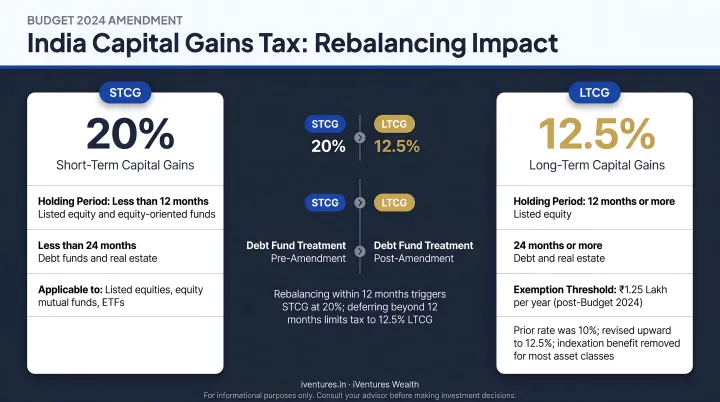

Tax Timing in India

India's capital gains tax framework makes timing rebalancing decisions around holding periods genuinely significant:

- Equity mutual funds and listed stocks held ≤ 12 months: STCG at 20% under Section 111A (effective 23 July 2024)

- Equity mutual funds and listed stocks held > 12 months: LTCG at 12.5% on gains above ₹1.25 lakh under Section 112A

- Debt mutual funds acquired on or after 1 April 2023: Gains are deemed short-term capital gains under Section 50AA — indexation benefit not available

The practical implication: timing equity rebalancing sales after the 12-month mark reduces the tax rate from 20% to 12.5%. For a UHNI with a ₹10 crore equity portfolio requiring 15% rebalancing, that difference is material.

Tax-aware rebalancing is a standard component of iVentures Wealth's advisory process, with rebalancing recommendations explicitly considering LTCG/STCG windows, tax-loss harvesting opportunities, and holding period optimisation.

Key Factors That Shape Your Rebalancing Decision

Risk tolerance and target allocation integrity Any rebalancing plan must be anchored to a documented target allocation that genuinely reflects the investor's risk capacity — not just their stated risk appetite. If goals or life circumstances have changed, the target allocation should be updated before rebalancing begins. Restoring an outdated allocation is not discipline; it's misalignment dressed up as process.

Transaction costs and tax efficiency Over-frequent rebalancing in taxable accounts erodes returns through:

- Securities Transaction Tax (STT): 0.1% on listed equity delivery sales; 0.001% on equity mutual fund redemptions

- Brokerage and statutory charges

- Capital gains tax (STCG at 20% or LTCG at 12.5%)

Practical ways to reduce friction: direct new SIP contributions toward underweight assets, harvest tax losses when available, and time discretionary sales after the 12-month LTCG threshold.

Portfolio complexity and the case for professional guidance A straightforward equity-debt portfolio can be managed with a calendar rule and basic monitoring. A multi-asset portfolio spanning domestic equities, international funds, debt, gold, REITs, AIFs, and private credit demands a more structured approach — one that accounts for illiquidity in alternatives, cross-border tax implications for NRI clients, and coordinated rebalancing across entities in a family office structure.

For UHNIs and family offices managing such portfolios, working with a SEBI-registered, fee-only investment adviser like iVentures Wealth means rebalancing decisions are driven entirely by fiduciary goals and tax efficiency, with no product distribution incentives in the picture.

Common Rebalancing Mistakes to Avoid

Over-trading in response to minor fluctuations triggers avoidable STCG taxes and brokerage costs. Adjust only when a defined threshold is breached or a scheduled review interval is due — not on impulse.

Letting fear or greed drive allocation changes is the opposite of disciplined rebalancing. Selling during a correction or piling into equities at a market peak both undermine the strategy. A rules-based framework — not market sentiment — should determine every move.

Rebalancing to an outdated target creates a false sense of discipline. If the investor has retired, sold a business, or had a major income shift, the target itself needs updating first. Life events should trigger an allocation review, not just a weights check.

A skilled advisory relationship helps catch all three — particularly the emotional drift that's easiest to miss in real time.

Frequently Asked Questions

What is the best rebalancing strategy?

There is no universally best strategy. The right fit depends on portfolio complexity, monitoring capacity, and sensitivity to tax and transaction costs:

- Calendar rebalancing — straightforward, suits most individual investors

- Threshold-based rebalancing — more responsive, better suited to larger portfolios

- Hybrid approach — combines both; most commonly recommended by advisors

What is the 5/25 rule for rebalancing?

The 5/25 rule, widely attributed to practitioner Larry Swedroe, triggers rebalancing when an asset class drifts by more than 5 percentage points in absolute terms or 25% in relative terms from its target — whichever threshold is reached first. This prevents over-trading while still catching meaningful drift before it significantly alters the portfolio's risk profile.

What are the 4 types of portfolio management strategies?

Perold and Sharpe's foundational framework identifies four strategies, each responding differently to trending versus volatile markets:

- Buy and hold — no rebalancing; linear payoff

- Constant mix — fixed weights maintained; benefits from reversals

- CPPI — floor-based insurance; convex payoff profile

- OBPI — option replication; similar convex profile to CPPI

What is the 15×15×15 rule?

The 15×15×15 rule is a SIP wealth accumulation heuristic: investing ₹15,000 per month for 15 years at an assumed 15% annualised return may generate approximately ₹1 crore. It illustrates equity compounding over time but is not a rebalancing rule. Maintaining a disciplined equity allocation through regular rebalancing supports the consistency required to realise such outcomes.

How often should you rebalance your portfolio?

Most advisors recommend reviewing and potentially rebalancing at least annually. Investors with larger or more complex portfolios benefit from quarterly reviews or threshold-based triggers. Investors with regular SIP contributions can use cash flow rebalancing to make smaller, more frequent corrections with minimal tax impact.

Does portfolio rebalancing trigger capital gains tax in India?

Yes. Selling overweight assets during rebalancing triggers capital gains tax — STCG at 20% if held 12 months or less, LTCG at 12.5% on gains above ₹1.25 lakh if held longer. Debt mutual funds acquired after 1 April 2023 are taxed as short-term gains regardless of holding period. Cash flow rebalancing, timing sales after the 12-month threshold, and tax-loss harvesting can substantially reduce this liability.