Introduction

India's retirement landscape has shifted dramatically. Life expectancy is rising, only about 11% of employed workers have access to formal social security, and inflation continues eroding purchasing power. For affluent Indians — founders, CXOs, UHNIs — retirement is a decades-long financial challenge with no government safety net to fall back on.

Most people spend months choosing which funds to invest in. Far fewer give serious thought to who should guide that decision. That's a mistake.

The advisor you choose determines not just your returns, but how long your corpus lasts, how tax-efficiently you draw it down, and whether your estate reaches the right people without dispute. Getting that choice wrong is one of the few retirement mistakes you can't recover from.

Key Takeaways

- Only SEBI-registered Investment Advisers (RIAs) are legally required to act as fiduciaries in India

- Commission-based distributors earn from product sales — their incentives don't always align with yours

- Retirement planning requires decumulation expertise, not just wealth accumulation skills

- Fee differences of even 1% annually can cost ₹40–50 lakh on a ₹5 crore corpus over 20 years

- The right advisor adjusts your plan as markets, tax laws, and life change — not just at onboarding

What Is a Retirement Financial Advisor?

A retirement financial advisor helps individuals build and sustain financial security after they stop working. The scope goes well beyond picking mutual funds — it covers income generation, tax-efficient withdrawals, capital preservation, and estate planning, with one clear goal: ensuring your assets outlast you.

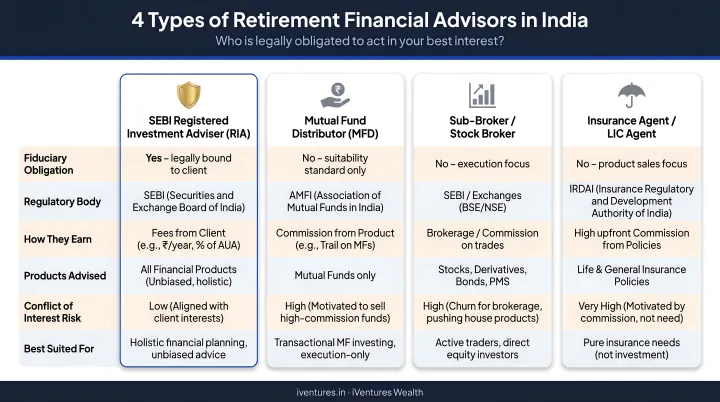

In India, this advisory landscape is fragmented. You'll encounter:

- SEBI-registered Investment Advisers (RIAs) — licensed fiduciaries who charge clients directly

- AMFI-registered mutual fund distributors — earn commissions from fund houses when they sell products

- Bank relationship managers — typically distribute in-house or partner products

- Insurance agents — focused on insurance-linked products, often with retirement framing

The distinction isn't just technical. It directly shapes the quality and objectivity of advice you receive.

Types of Retirement Advisors in India

| Advisor Type | How They're Paid | Fiduciary Obligation? |

|---|---|---|

| SEBI RIA (fee-only) | Directly by client | Yes — legally required |

| Mutual fund distributor | Commission from AMC | No |

| Bank RM | Salary + product targets | No |

| Insurance agent | Commission on premiums | No |

When choosing someone to manage a retirement corpus that may need to last 25–30 years, that fiduciary column matters enormously. That fiduciary standing also determines the breadth of services you can expect.

What Services Should You Expect?

A qualified retirement advisor provides far more than an investment portfolio. Core services include:

- Retirement corpus calculation aligned with your lifestyle, health, and longevity assumptions

- Portfolio design across equity, debt, fixed income, and alternative assets

- SWP (Systematic Withdrawal Plan) structuring for tax-efficient regular income

- NPS and EPF withdrawal optimization under current PFRDA rules

- Tax planning on retirement income under Indian tax law

- Estate and succession planning, including wills and trust structures

- Insurance adequacy review to protect against longevity and healthcare risks

For UHNIs, founders, and business owners, this integration is critical. A retirement plan that doesn't account for estate structure, concentrated equity holdings, or business exit liquidity is incomplete — regardless of how well the portfolio itself is constructed.

Key Factors When Choosing a Retirement Financial Advisor

With over 1,044 registered investment advisers currently listed on SEBI's directory, choosing the right one requires evaluating verifiable criteria — not just brand recognition or a personal referral.

SEBI Registration and Regulatory Standing

SEBI RIA registration is non-negotiable. Under the SEBI Investment Advisers Regulations, 2013, only registered investment advisers are legally required to act in a fiduciary capacity — disclosing conflicts of interest, conducting risk profiling, and ensuring all advice is suitable to the client's profile.

How to verify: Check the SEBI Investment Adviser directory by name or registration number. You can confirm registration validity, contact details, and registration period. Do this before any other evaluation — it's your first filter.

SEBI also prohibits individual RIAs from simultaneously providing distribution services, ensuring the same advisor can't recommend a fund and earn trail income from it.

Fiduciary Commitment vs. Commission-Based Advice

This is the most consequential distinction in Indian financial advisory. Here's what it means in practice:

- A commission-based distributor earns revenue each time they sell a product. Their income depends on which products you buy — not how well those products serve your retirement goals.

- A fee-only RIA earns nothing from product manufacturers. Their only income is your advisory fee, which means their recommendations are structurally unbiased.

For retirement planning, mis-selling risk is real and well-documented. ULIPs, for example, are frequently positioned to appear similar to mutual funds despite lock-ins and higher costs that can permanently impair a retirement corpus. SEBI now uses AI to detect mis-selling in the mutual fund industry — a signal of how widespread the problem is.

The financial cost of conflicted advice is quantifiable. A U.S. Council of Economic Advisers study estimated that commission-driven investment advice reduces retirement saver returns by approximately 1 percentage point per year. Over 30 years, that compounds into a 12% reduction in total savings. The mechanism operates identically in India, even if the scale hasn't been officially measured.

Credentials and Retirement-Specific Expertise

For retirement planning clients in India, the benchmark credential combination is:

- SEBI RIA registration — confirms fiduciary obligation and regulatory standing

- CFA charterholder — signals deep expertise in portfolio construction, asset allocation, and investment analysis (over 2,400 CFA Society India members nationally)

- CFP certification — indicates comprehensive financial planning capability, including retirement income strategies (3,215 CFP professionals in India as of 2025)

These credentials confirm a defined competence threshold — but they don't substitute for demonstrated experience. Ask the advisor directly: how many clients have you managed through retirement transitions? Can you walk me through a retirement drawdown strategy you've built for someone in a similar situation?

Advisors who have worked extensively with UHNIs, founders, or NRI clients bring familiarity with the most complex retirement structures. That depth of experience matters as much as any single credential.

Retirement-Specific Knowledge: Decumulation vs. Accumulation

Retirement planning is a distinct discipline from general wealth management. The skills required to grow a corpus are not the same as those required to sustain it.

A retirement specialist must understand:

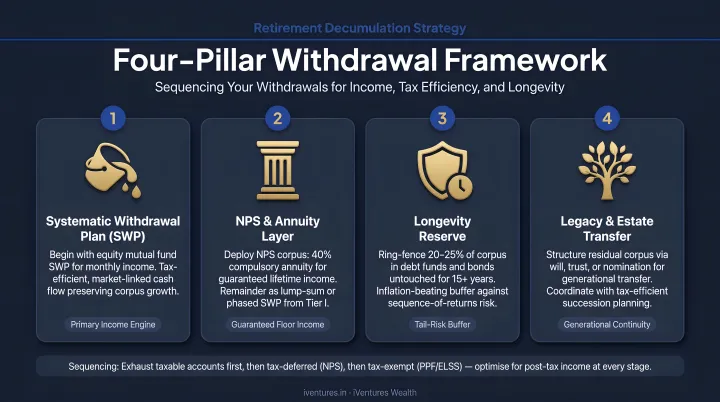

- Withdrawal sequencing — which assets to draw from first (NPS, EPF, mutual funds, fixed income) and in what order to minimise tax

- SWP mechanics — structuring systematic withdrawals so that only gains are taxed, not principal; equity fund LTCG is taxed at 12.5% on gains above ₹1.25 lakh after the relevant holding period

- NPS exit rules — as updated in December 2025, non-government-sector subscribers can take up to 80% as lump sum (60% tax-exempt under Section 10(12A)) and must use at least 20% for annuity purchase

- Longevity risk — planning for a 25–30-year retirement horizon, not just a 10-year accumulation window

Advisors without this specialisation typically default to growth-oriented strategies well into the retirement phase — a mismatch that erodes capital precisely when clients can least afford the risk.

Fee Structure and Total Cost Transparency

SEBI caps advisory fees at 2.5% of AUA per annum or a fixed fee of up to ₹1.51 lakh per annum per family. In practice, market rates for advisors serving wealthier clients typically fall between ₹25,000 and ₹1.5 lakh for fixed-fee models.

Fee differences that appear small compound significantly over time. Consider a ₹5 crore retirement corpus over 20 years:

| Annual Advisory Fee | Corpus After 20 Years | Fee Drag |

|---|---|---|

| 0.5% | ~₹4.52 Cr | ~₹0.48 Cr |

| 1.0% | ~₹4.09 Cr | ~₹0.91 Cr |

| 1.5% | ~₹3.70 Cr | ~₹1.30 Cr |

(Calculated on fee drag only, excluding investment returns and taxes)

The difference between a 0.5% and 1.5% fee structure is approximately ₹82 lakh over 20 years on a ₹5 crore corpus — before accounting for investment returns.

Any reputable advisor should disclose all fees — advisory charges, fund expense ratios, and any transaction costs — upfront and in writing before you commit.

Personalization, Communication, and Long-Term Partnership

Retirement planning is not a one-time deliverable. Markets shift, tax laws change, health circumstances evolve. A retirement plan built at 55 should look materially different by 65 and again by 75.

Ask prospective advisors:

- How often do you conduct formal portfolio reviews?

- What is your process when a client faces a major life event — a business sale, a health crisis, a family transition?

- How do you communicate during market downturns?

- Who manages my relationship if you're unavailable?

That last question is often overlooked. A team-based advisory model with documented succession protocols is far preferable to a single-advisor dependency — particularly for clients whose retirement horizon spans decades.

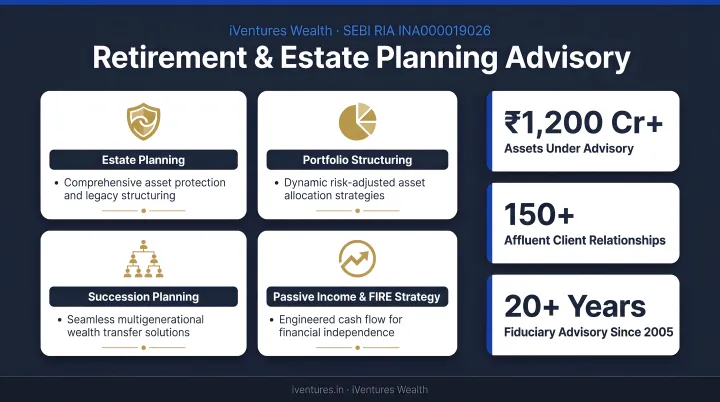

How iVentures Wealth Can Help

iVentures Wealth (SEBI RIA No. INA000019026) is a fee-only investment advisory firm that has been serving affluent families since 2005, with SEBI registration formalised in 2010. The firm manages ₹1,146+ Cr across 150+ client relationships, serving UHNIs, family offices, CXOs, founders, and NRI/OCI clients with complex, multi-generational financial structures.

The firm's retirement advisory goes beyond portfolio management:

- SWP structuring with tax optimisation built in — withdrawal frameworks designed to generate regular income while preserving capital

- Estate and succession planning — wills, private trust establishment, and wealth transfer structures prepared with senior legal counsel

- Cross-border retirement planning for NRIs/OCIs — DTAA structuring, GIFT City vehicles, and USD-denominated passive income strategies

- FIRE/early retirement planning — FIRE-number computation, glide-path planning for the 5 years pre-retirement, and de-accumulation strategy post-retirement

- Bucket strategy design — documented in a ₹100+ Cr case study where a founder's exit liquidity was structured into safety, stability, and growth buckets with a family trust framework

These services are backed by Krishna Makhariya, CFA charterholder and Head of Research, who leads investment strategy and portfolio construction. The Wealth Monitor App provides real-time consolidated portfolio visibility across mutual funds, equities, bonds, FDs, PMS, and AIFs — tracked through a single dashboard.

As a SEBI-registered RIA, iVentures is structurally prohibited from earning commissions, trail income, or placement fees from any product manufacturer. Fees are disclosed upfront, in writing, before any investment is made.

Conclusion

Choosing a retirement financial advisor is one of the most consequential financial decisions you'll make — a relationship that shapes two to three decades of your financial life. The right advisor is defined by regulatory standing, fee structure integrity, and genuine retirement specialisation — not the breadth of products they can sell you.

Before committing, run through this checklist:

- Confirm SEBI registration and RIA status

- Verify fiduciary obligation in writing

- Evaluate credentials and retirement-specific experience

- Understand the full fee structure and what's included

A well-chosen advisor will review and recalibrate your strategy as your health, family, markets, and tax laws evolve. That ongoing relationship — grounded in trust, transparency, and technical depth — determines whether your retirement corpus holds through every phase of life ahead.

Frequently Asked Questions

Can a financial advisor help with retirement planning?

Yes. A qualified SEBI-registered RIA can support every stage of retirement planning — from corpus building and asset allocation to post-retirement income structuring, tax optimisation, and estate planning. Choose an advisor with retirement-specific expertise, not just general investment management capability.

What is the difference between a financial advisor and a retirement planner?

A financial advisor provides broad guidance across investments, insurance, and tax. A retirement planner specialises in building and sustaining post-retirement income — including decumulation strategy, withdrawal sequencing, and longevity risk management. The strongest advisors integrate both capabilities within one engagement.

What credentials should I look for in a retirement financial advisor in India?

SEBI RIA registration is the foundational credential — it legally mandates fiduciary duty. A CFA charterholder designation indicates deep investment expertise, while CFP certification reflects comprehensive financial planning knowledge. Prioritise advisors who combine SEBI RIA registration with one or both of these designations.

What is a fiduciary financial advisor and why does it matter for retirement?

A fiduciary is legally obligated to act in the client's best interest at all times. For retirement planning, this means recommending only what serves your goals — not what earns the advisor the highest commission. In India, only SEBI-registered investment advisers carry this legal obligation.

How much does a retirement financial advisor charge in India?

SEBI caps advisory fees at 2.5% of AUA per annum or ₹1.51 lakh per annum per family. Market rates typically range from ₹25,000 to ₹1.5 lakh for fixed-fee models. Fee-only RIA structures align better with client interests — in commission-based models, product revenue can skew recommendations.

When should I start working with a retirement financial advisor?

Ideally, 10–15 years before your target retirement date — this allows sufficient time for corpus building, strategy refinement, and tax-efficient structuring. Advisors also deliver strong value for clients already in retirement, through withdrawal optimisation, tax management, and capital protection.