Introduction

Most investors put genuine effort into selecting their initial investments — researching funds, evaluating asset classes, and setting a target allocation. Then they move on. Months pass. Markets move. And the portfolio quietly drifts away from the original plan while the investor assumes everything is still on track.

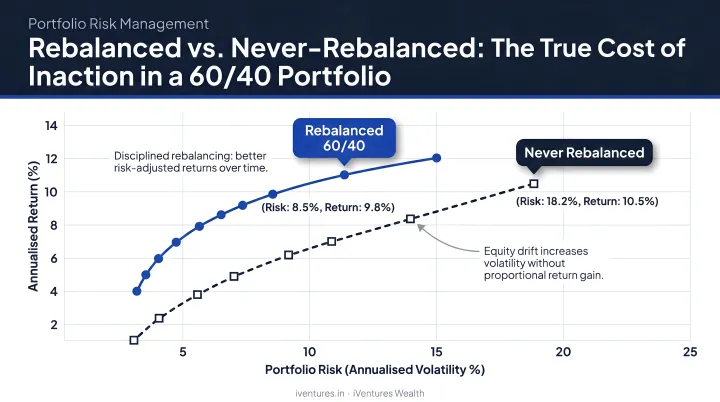

This is one of the most common and costly oversights in wealth management. Vanguard's analysis of a 60/40 stock-bond portfolio from 1926 to 2009 found that a never-rebalanced portfolio drifted to an average equity allocation of 84.1% — reaching as high as 99% at its peak — against an original target of 60%.

Portfolio rebalancing is what prevents this drift. It realigns your holdings with your intended asset allocation, controlling risk and keeping your portfolio consistent with your financial goals.

This article covers:

- What rebalancing actually means and how it works

- Why it matters across different life stages

- How portfolio drift develops in practice

- The main rebalancing strategies available

- Tax implications Indian investors need to account for

Key Takeaways

- Rebalancing controls risk — not returns. It prevents your portfolio from becoming far riskier than you intended.

- Portfolio drift happens automatically as different assets grow at different rates. You don't have to make a single bad decision for it to occur.

- Annual rebalancing is the standard starting point; complex portfolios benefit from pairing calendar reviews with drift thresholds.

- Every rebalancing decision in India carries potential capital gains tax implications — plan around them, not after them.

- Fresh inflows and dividends can often rebalance a portfolio without triggering taxable events.

What Is Portfolio Rebalancing?

The CFA Institute defines rebalancing as "the discipline of adjusting portfolio weights to more closely align with the strategic asset allocation." In practical terms, it means periodically reviewing what your portfolio actually holds and making buy or sell decisions to restore the original intended mix.

It's Personal, Not Formulaic

A common misconception is that rebalancing means moving to a 50/50 split. It doesn't. Your target allocation is specific to you — it might be 70% equity and 30% debt, or 60% equity with allocations across debt, alternatives, and global funds. What matters is that the actual allocation stays close to your target, not anyone else's.

The target is set based on your financial goals, investment horizon, income needs, and risk tolerance. That mix looks different for everyone:

- A CXO approaching retirement may favour a conservative tilt toward fixed income

- An entrepreneur in their 30s with a 20-year horizon may carry higher equity exposure

- An NRI with global diversification needs may hold cross-border allocations alongside domestic assets

The discipline is simply keeping the portfolio aligned with whichever allocation was chosen — not someone else's benchmark.

Rebalancing Is Not Market Timing

This distinction matters. Rebalancing is a rules-based discipline triggered by allocation drift, not by a view on where markets are headed. When you rebalance, you're not predicting that equities will fall or that bonds will outperform. You're simply restoring proportions. Vanguard puts it plainly: the primary goal of rebalancing is to minimise risk relative to your target allocation, not to maximise returns.

Why Rebalancing Is Essential to Long-Term Wealth Management

The Risk Problem Nobody Notices

Asset classes that outperform naturally grow to dominate your portfolio. Equities tend to outperform debt over long periods — which is exactly why an unmanaged portfolio becomes progressively more equity-heavy, and therefore more volatile, without the investor making a single active decision.

Vanguard's research on rebalancing puts this in concrete terms: a never-rebalanced 60/40 portfolio generated a 9.1% annualised return with 14.4% standard deviation, while an annually rebalanced version produced 8.6% return with just 11.9% standard deviation. The unrebalanced portfolio returned slightly more — but only by accepting substantially more risk. For most investors, that tradeoff was never part of the original plan.

The Behavioural Dimension

Markets create emotional pressure in both directions. During a bull run, investors feel confident and reluctant to sell rising assets. During a correction, fear makes buying more of anything feel counterintuitive. Both reactions work against good portfolio management.

Rebalancing inverts this pattern deliberately. By selling what has grown beyond its target weight and buying what has fallen below it, the process mechanically enforces a "sell high, buy low" discipline. As Investor.gov notes, this approach helps investors avoid the opposite — buying at peaks and selling in panic. At iVentures Wealth, continuous portfolio monitoring is part of the advisory process precisely for this reason — catching drift into return-chasing behaviour before it compounds into a structural problem.

Critical Life Stages

Rebalancing becomes especially consequential at major transitions, where an inappropriate allocation can cause lasting damage:

- Approaching retirement: a portfolio that's drifted too equity-heavy has limited time to recover from a sharp drawdown

- After a business exit: sudden liquidity events require rapid reallocation away from concentrated positions

- Receiving an inheritance: new assets may significantly shift the overall allocation and risk profile

- Major goal changes: a shift in time horizon or income needs often warrants a new target allocation, followed by rebalancing toward it

Without rebalancing, diversification breaks down silently. A well-diversified portfolio at inception can drift into heavy concentration in a single asset class or sector — not through any decision, but through inaction. That concentration is precisely the risk that rebalancing is designed to prevent.

How Portfolio Drift Occurs: A Practical Example

Portfolio drift doesn't require any mistakes. It happens automatically whenever different asset classes post different returns.

A Simple Illustration

Suppose an investor starts with 65% equity funds and 35% debt funds. After a sustained equity rally, stocks appreciate significantly while the debt portion grows more slowly. Without any action, the ratio shifts to 78% equity and 22% debt.

The investor is now running a materially different portfolio from the one they originally agreed to — heavier in equities, more exposed to volatility — without having made a single active decision.

The shift in portfolio weights depends on how all assets move simultaneously, not just one. A 20% decline in one asset class may shift proportions less than a 10% gain in another, depending on their starting weights. Monitoring drift means looking at the portfolio as a whole, not asset by asset.

The Rebalancing Threshold

Not every deviation warrants action. Small, short-term fluctuations — a 1-2 percentage point drift — may not justify the costs of rebalancing. But when drift becomes significant, inaction carries its own risk.

Two widely referenced benchmarks offer practical guidance:

- Vanguard recommends annual or semi-annual monitoring with a 5% threshold as a reasonable balance between risk control and cost minimisation.

- Morningstar suggests rebalancing when allocation variance from target reaches 5 or 10 percentage points.

Both frameworks share the same logic: set a clear trigger in advance, so rebalancing becomes a process rather than a reactive scramble.

Portfolio Rebalancing Strategies: Finding the Right Approach

There are three main strategies. The right choice depends on portfolio complexity, monitoring capacity, and cost sensitivity.

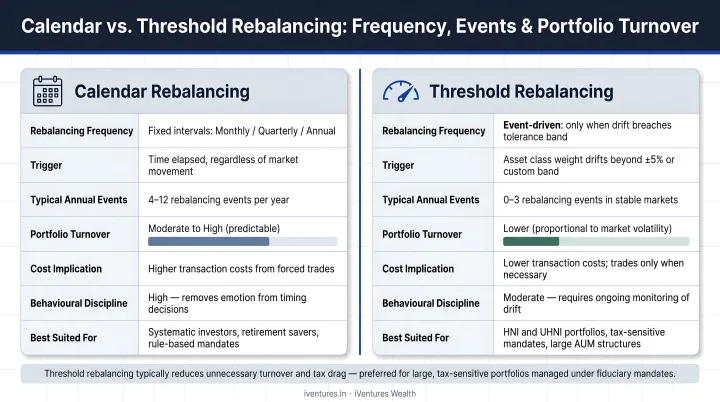

Calendar-Based Rebalancing

The investor reviews and rebalances on a fixed schedule — quarterly, semi-annually, or annually — regardless of how much the portfolio has drifted. Annual rebalancing is widely considered the most practical option for most long-term investors. It limits unnecessary transaction costs while still catching meaningful drift before it compounds.

The limitation: this approach may miss significant drift that occurs between review dates, particularly in volatile markets.

Threshold-Based (Constant-Mix) Rebalancing

Rebalancing is triggered only when an asset class drifts beyond a defined tolerance band — for example, if equity allocation moves more than 5 percentage points above or below target.

This approach responds to actual market movement rather than arbitrary dates, which makes it more precise. The tradeoff is that it requires more frequent monitoring. Vanguard's data shows monthly threshold-based rebalancing required 1,008 rebalancing events and 2.7% annual portfolio turnover — versus just 15 events and 1.4% turnover for annual monitoring with a 10% threshold. More frequent intervention doesn't always translate to better risk-adjusted results.

Combined Calendar and Threshold Rebalancing

This hybrid approach — reviewing on a set schedule but only rebalancing if drift has exceeded a defined threshold — avoids unnecessary trading while ensuring meaningful deviations are addressed.

For investors managing complex, multi-asset portfolios — UHNIs, family offices, or those with cross-border holdings — this structure offers the best balance of discipline and responsiveness. iVentures Wealth's advisory process follows this model: continuous monitoring, at least quarterly formal reviews, and rebalancing triggered by both scheduled reviews and market-driven drift.

That said, not every investor needs active oversight. Target-date or lifecycle funds automate rebalancing entirely — a workable option for simpler portfolios. The tradeoff is reduced flexibility: an active advisory relationship accounts for drift, tax impact, and individual circumstances that automated funds simply cannot replicate.

When and How Often Should You Rebalance?

There's no universal rule, but research points in a clear direction. Rebalancing too frequently — monthly, or on a pure calendar basis with no threshold — generates unnecessary transaction costs without meaningful risk benefit. Rebalancing too infrequently, say every two years or more, allows the kind of drift that can fundamentally alter your portfolio's risk profile.

Annual reviews are the widely recommended baseline for most long-term investors. Those with larger or more complex portfolios typically benefit from pairing the annual review with threshold-based monitoring.

Event-Driven Triggers

Beyond the calendar, several life events warrant an immediate review:

- A significant market correction or sustained rally

- Retirement, business exit, or other major liquidity events

- Receipt of new assets — inheritance, ESOP payout, property sale proceeds

- A change in financial goals, risk appetite, or time horizon

- Major family changes — marriage, children entering education, health events

For investors managing multi-asset portfolios across equity, debt, real estate, and alternatives — including PMS, AIFs, and bonds — maintaining visibility across all holdings simultaneously is the core challenge. iVentures Wealth's Wealth Monitor App, launched in 2020, addresses this directly by giving clients a consolidated view of their asset allocation in real time, so drift is caught early rather than corrected late.

Tax and Cost Considerations When Rebalancing

Every rebalancing transaction has potential costs, and in India, the most significant is typically capital gains tax.

The Indian Tax Framework

For direct equity and equity-oriented mutual funds, the holding period determines whether gains are classified as short-term or long-term. Per the Income Tax Department's framework, assets held for 12 months or less are short-term; those held for more than 12 months are long-term. Both LTCG and STCG carry tax implications that should be factored into any rebalancing decision — though readers should consult a qualified tax adviser for current applicable rates, as these can change with each Budget.

For debt mutual funds acquired on or after 1 April 2023, Section 50AA deems gains as short-term regardless of the holding period — a significant change from the earlier tax treatment that investors must account for when planning rebalancing in the debt portion of their portfolio.

Securities Transaction Tax (STT) applies to exchange-executed transactions and adds to the cost of frequent trading.

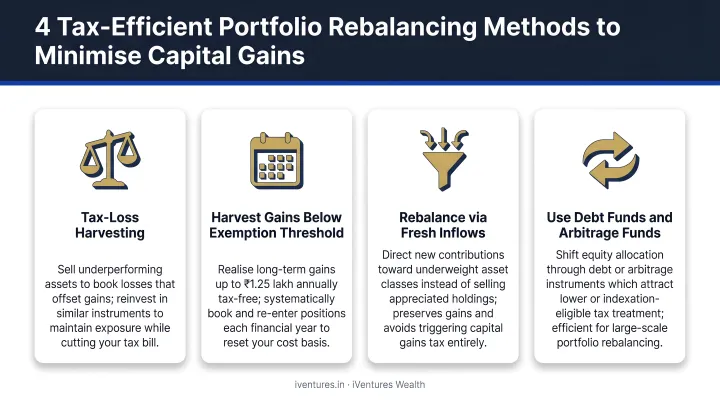

Tax-Efficient Rebalancing Methods

Selling appreciated assets to rebalance isn't the only approach — and often isn't the most efficient one:

- Redirect fresh contributions to underweight asset classes rather than selling overweight positions

- Use dividends and interest receipts to top up lagging allocations without triggering sales

- Time withdrawals strategically — when you need to take money out, take it from overweight asset classes, serving a dual purpose

- Use Systematic Withdrawal Plans (SWPs) from mutual funds structured around tax-efficient lots, particularly for equity-oriented funds held beyond 12 months

Applying these methods requires judgment, not just rules. iVentures Wealth builds tax-aware structuring into portfolio decisions as standard practice — covering LTCG/STCG timing, DTAA considerations for NRI clients, and coordination with clients' chartered accountants.

The core principle: excessive or undisciplined rebalancing can erode net returns through transaction costs and tax leakage. But the cost of unchecked drift — holding a portfolio far riskier than intended — is equally real. The decision always involves weighing both sides.

Frequently Asked Questions

What is the 5/25 rule for portfolio rebalancing?

The 5/25 rule, attributed to financial planner Larry Swedroe, says to rebalance when an asset class drifts more than 5 percentage points from its target allocation, or more than 25% of its original weight — whichever threshold is smaller. Vanguard and Morningstar use simpler variants, flagging drift of 5 to 10 percentage points as a rebalancing trigger.

Is portfolio rebalancing a good idea?

For most long-term investors, yes. Rebalancing controls risk, maintains alignment with financial goals, and instils investment discipline. The key is avoiding over-rebalancing, which generates unnecessary costs without proportionate benefit. Annual reviews with a defined threshold work well for most investors.

What are the 7 steps of the portfolio process?

The CFA Institute defines seven steps: setting objectives, assessing constraints, creating an investment policy statement, establishing target allocation, constructing the portfolio, monitoring and rebalancing, and measuring performance. Rebalancing is step six — the ongoing maintenance that preserves the integrity of every decision made before it.

How often should I rebalance my investment portfolio?

Annual rebalancing is a sensible starting point for most investors. Those managing larger or more complex portfolios across multiple asset classes, global funds, or illiquid alternatives typically benefit from pairing annual reviews with threshold-based triggers to catch meaningful drift between scheduled dates.

How does rebalancing affect taxes in India?

Selling assets to rebalance can trigger STCG or LTCG depending on the holding period. For equity and equity-oriented funds, the 12-month holding period determines the classification. Debt funds acquired on or after 1 April 2023 are treated as short-term regardless of how long they've been held. Consulting a tax adviser before executing rebalancing transactions is advisable, as tax rates and rules can change.

What is the difference between calendar and threshold rebalancing?

Calendar rebalancing occurs on a fixed schedule regardless of how much the portfolio has drifted. Threshold rebalancing is triggered only when an asset's allocation moves beyond a defined band. A combined approach reviews on a schedule but only rebalances if meaningful drift has actually occurred — minimising unnecessary trading while keeping risk in check.