What makes this particularly complex for NRIs is that India taxes capital gains on Indian assets regardless of where you live. Whether you're selling a flat in Gurugram, redeeming mutual fund units, or transferring unlisted shares, the Income Tax Act applies. This guide covers current rates by asset class, TDS obligations, available exemptions, and DTAA benefits for FY 2025-26.

Key Takeaways

- NRIs pay capital gains tax in India on profits from Indian assets—property, listed shares, mutual funds, and unlisted securities

- STCG on listed equity is now 20%; LTCG is 12.5% above ₹1.25 lakh (no indexation)

- Finance Act 2024 removed indexation for most assets; any grandfathering option for property acquired before July 23, 2024 applies to resident individuals only, not NRIs

- Sections 54, 54EC, and 54F offer legal routes to reduce LTCG liability on property

- TDS is deducted before payment reaches the NRI—excess TDS can be reclaimed by filing ITR-2

Who Is an NRI for Capital Gains Tax in India?

Residential status under Section 6 of the Income Tax Act determines your tax liability—not where your passport is from.

You are classified as a non-resident if you were present in India for fewer than 182 days in the financial year. A secondary test also applies: 60 days in the current year plus 365 days across the preceding four years. Indian citizens leaving for employment abroad — or serving as crew on an Indian ship — are exempt from this secondary test and need only meet the 182-day threshold.

Tax scope for NRIs:

- NRIs are taxed in India only on India-sourced income—not global income

- Capital gains from any capital asset situated in India are deemed to accrue in India under Section 9(1)(i) of the Income Tax Act

- This covers property, listed and unlisted shares, mutual funds, and other Indian capital assets

OCIs and PIOs are subject to the same rules. Section 115C of the Income Tax Act defines a "non-resident Indian" as a citizen of India — or a person of Indian origin — who does not currently reside in India. For capital gains purposes, this means OCI and PIO cardholders with Indian assets are taxed identically to NRI citizens.

Capital Gains Tax Rates for NRIs on Different Asset Types in 2026

The rates below reflect Finance Act 2024 revisions, applicable to all transfers on or after July 23, 2024, and in force for the full FY 2025-26.

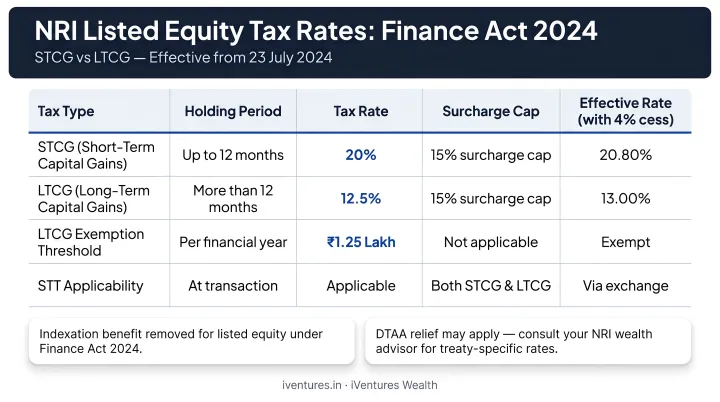

Listed Equity Shares and Equity-Oriented Mutual Funds

| Holding Period | Classification | Tax Rate |

|---|---|---|

| Up to 12 months | Short-Term Capital Gain (STCG) | 20% under Section 111A |

| More than 12 months | Long-Term Capital Gain (LTCG) | 12.5% under Section 112A on gains above ₹1.25 lakh |

Key points for NRIs on equity gains:

- No indexation benefit applies to either STCG or LTCG

- STCG rate was revised upward from 15% to 20% effective July 23, 2024

- The ₹1.25 lakh annual exemption applies only to LTCG on equity; gains below this threshold are not taxed

- Surcharge under Sections 111A and 112A is capped at 15%, plus 4% Health and Education Cess on income tax and surcharge combined

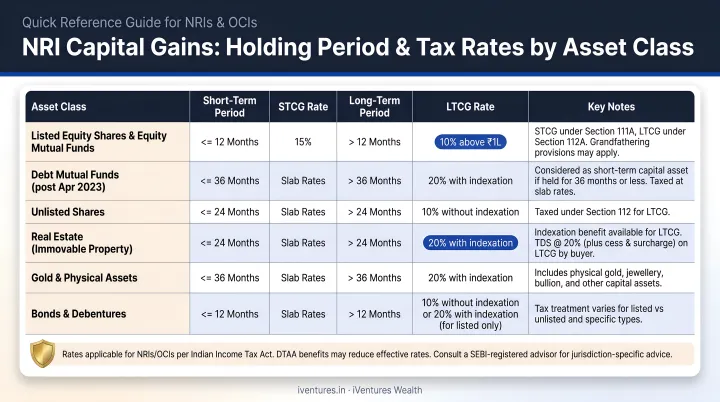

Real Estate and Property

- LTCG (held more than 24 months): 12.5% without indexation

- STCG (held 24 months or less): Applicable income tax slab rates

An important clarification from the Income Tax Department's official capital gains page: the option to compare 12.5% without indexation versus 20% with indexation for property acquired before July 23, 2024, is available only to resident individuals and HUFs—not NRIs. NRIs have no access to this transitional rate-comparison option, regardless of when the property was acquired.

Debt Mutual Funds

Under Section 50AA, debt-oriented mutual funds with less than 35% equity allocation are treated differently from other asset classes:

- Funds acquired on or after April 1, 2023, are taxed as short-term gains regardless of holding period

- Tax applies at applicable income tax slab rates — no flat rate applies

- No LTCG treatment and no indexation benefit available for NRIs in FY 2025-26

Unlisted Shares

- STCG (held under 24 months): Slab rates

- LTCG (held 24 months or more): 12.5% without indexation

Holding Period Rules: Quick Reference

| Asset Class | LTCG Threshold | STCG Rate | LTCG Rate |

|---|---|---|---|

| Listed equity shares | 12 months | 20% | 12.5% (above ₹1.25 lakh) |

| Equity-oriented mutual funds | 12 months | 20% | 12.5% (above ₹1.25 lakh) |

| Immovable property | 24 months | Slab rates | 12.5% (no indexation) |

| Unlisted shares | 24 months | Slab rates | 12.5% (no indexation) |

| Debt mutual funds | N/A (Section 50AA) | Slab rates | Not applicable |

The holding period is counted from the date of purchase to the date of transfer. Include both dates when calculating whether you cross the LTCG threshold — even a single day short of the required period keeps the gain taxed at the higher STCG rate.

Section 48 — Foreign Currency Computation for NRIs: When an NRI sells shares or debentures of an Indian company that were originally purchased in foreign currency, Section 48's first proviso applies a special calculation method. The acquisition cost, transfer expenses, and sale proceeds are each converted to the original foreign currency, the gain is computed in that currency, and the result is then reconverted to Indian rupees.

This provision applies only to shares and debentures of Indian companies — it does not extend to property, debt funds, or other Indian asset classes.

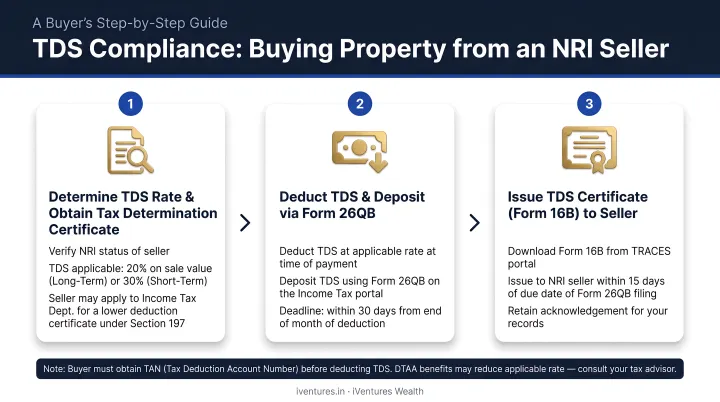

TDS on Capital Gains: What NRIs and Buyers Must Know

TDS for NRI sellers operates under Section 195, not Section 194-IA. The ₹50 lakh threshold that applies when a resident buys from another resident does not apply when the seller is an NRI. The buyer must deduct TDS from the first rupee.

Current TDS Rates for NRI Asset Sales

| Asset Type | TDS Rate |

|---|---|

| Listed equity STCG | 20% |

| Listed equity LTCG | 12.5% |

| Property LTCG (held over 24 months) | 12.5% |

| Property STCG (held under 24 months) | Up to 30% (slab rates) |

Buyer Obligations on Property Purchase from NRI

When buying property from an NRI, the buyer must:

- Deduct TDS at the applicable rate before making payment

- Deposit the deducted amount with the government using Form 27Q

- Issue a TDS certificate to the NRI seller

Failure to comply makes the buyer liable for the unpaid TDS, plus interest and penalties. A frequent error: buyers file Form 26QB (the form for resident-to-resident transactions) instead of Form 27Q, which triggers a separate compliance violation and does not discharge the buyer's liability.

Lower TDS and Refunds

If TDS looks set to exceed the actual tax liability, NRIs have two routes available — before or after the deduction.

Before deduction: Apply to the Income Tax Department under Section 197 using Form 13 for a lower or nil TDS certificate. Once approved, the buyer deducts at the reduced certified rate instead of the standard rate.

After deduction: If excess TDS has already been withheld, NRIs can recover it by filing an income tax return in India. Key points:

- File ITR-2 (covers salary, property income, and capital gains)

- ITR-1 and ITR-4 are not valid options for NRIs with capital gains

- The refund is processed after the return is assessed

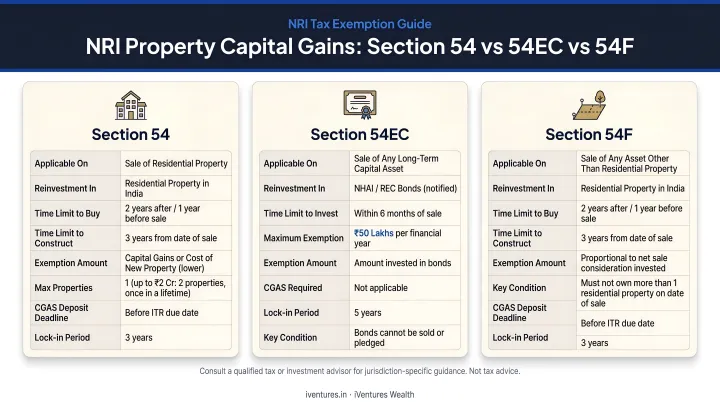

Exemptions That Can Reduce NRI Capital Gains Tax on Property

NRIs cannot avoid capital gains tax entirely, but three statutory provisions significantly reduce liability on property sales.

Section 54 – Reinvestment in Residential Property

Available when an NRI sells a long-term residential house property in India:

- Reinvest the LTCG into a new residential property in India within 2 years of sale (or construct within 3 years)

- The new property must not be sold within 3 years

- One-time option to purchase two houses if LTCG does not exceed ₹2 crore

Section 54F – LTCG on Other Long-Term Assets

Available when selling any long-term capital asset other than a residential house—such as listed shares, commercial property, or gold:

- Invest the net sale proceeds (not just the gains) into a residential house in India

- Exemption applies proportionately to the amount invested

- Condition: must not own more than one residential house (other than the new purchase) at the time of transfer

Section 54EC – Investment in Specified Bonds

One clarification worth noting: Section 54EC applies specifically to LTCG from the transfer of land or building or both—not every long-term capital asset.

- Invest LTCG proceeds in specified government-backed bonds (NHAI, REC, PFC, IRFC) within 6 months of the sale

- Maximum investment: ₹50 lakh per financial year

- Lock-in period: 5 years (selling before 5 years reverses the exemption)

- Current interest rate on these bonds: approximately 5.25% per annum

NRIs planning to use 54EC bonds should factor in the 5-year lock-in and lower yield when evaluating this route against reinvestment options under Section 54 or 54F.

Capital Gains Account Scheme (CGAS)

If reinvestment cannot be completed before the ITR filing deadline (July 31, 2026 for FY 2025-26), deposit the unutilized gain in a Capital Gains Account with a designated bank before that date. The funds remain exempt as long as they are deployed within the statutory reinvestment window. NRIs use an NRO Capital Gains Account for this purpose.

DTAA Benefits, Advance Tax, and Compliance for NRIs

Double Taxation Avoidance Agreements

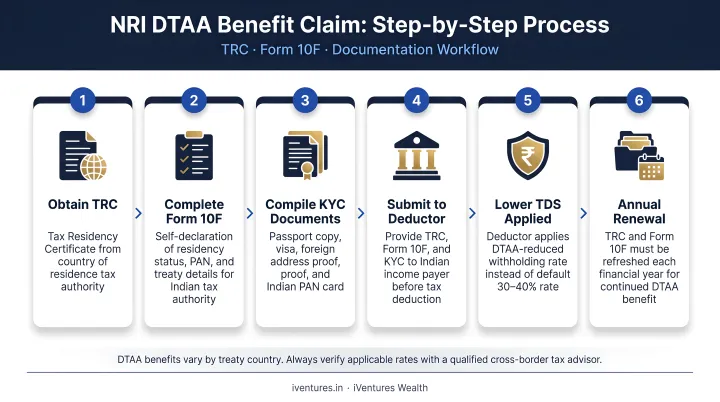

India has DTAAs with numerous countries—US, UK, UAE, Canada, Singapore, Australia, and many others. These treaties prevent the same income from being taxed twice. Under DTAA, NRIs typically either:

- Claim an exemption in one country, or

- Claim a foreign tax credit in their country of residence for taxes already paid in India

To claim DTAA benefits, the NRI must submit:

- A Tax Residency Certificate (TRC) from their country of residence

- Form 10F as prescribed under Section 90

One caution: DTAA provisions vary significantly by country and asset type. The India-UAE treaty, for instance, has a specific Article 13 on capital gains—its terms cannot be assumed to apply under the India-US or India-UK treaty. Check the CBDT DTAA utility for country-specific treaty text before claiming benefits.

DTAA does not eliminate Indian tax on capital gains. It reduces the effective combined burden across jurisdictions.

Advance Tax and ITR Filing

- NRIs must pay advance tax if estimated Indian tax liability exceeds ₹10,000 in the financial year (Section 208)

- Failure to pay triggers interest under Section 234B (non-payment) and Section 234C (installment deferment)

- ITR filing deadline for FY 2025-26 (AY 2026-27): July 31, 2026 (unless extended by CBDT)

NRIs must file an ITR in India if:

- Gross Indian income exceeds the basic exemption limit (₹2.5 lakh under old regime; ₹4 lakh under the new regime for FY 2025-26)

- They want to claim a refund on excess TDS

- They want to carry forward capital losses (requires filing by the due date, even if income is below the exemption limit)

For NRIs managing assets across multiple countries—particularly US, UK, or UAE residents with Indian property and equity portfolios—the intersection of TRC documentation, DTAA claims, FATCA/CRS reporting, and Indian compliance demands careful coordination across jurisdictions.

iVentures Wealth (SEBI RIA: INA000019026) advises NRI/OCI clients on DTAA structuring, TDS planning, and capital gains optimization as part of its cross-border wealth mandates. The firm works with clients holding ₹5 crore or more in investable assets.

Frequently Asked Questions

Do NRIs need to pay capital gains tax in India?

Yes. NRIs are taxed on capital gains from the sale of any asset situated in India—including property, listed shares, mutual funds, and unlisted securities—regardless of where they reside. This is governed by the Income Tax Act under Section 9(1)(i), which deems such gains to arise in India.

How is capital gains tax calculated for an NRI?

Capital gains equal the sale price minus the cost of acquisition (and improvement costs, where applicable). The gain is classified as short-term or long-term based on the holding period, then taxed at the applicable rate—for example, 20% STCG or 12.5% LTCG for listed equity—plus a 4% Health and Education Cess on top of income tax and surcharge.

How can NRIs reduce capital gains tax on property?

NRIs can reduce LTCG liability by reinvesting under Section 54 (another residential property), Section 54EC (specified bonds up to ₹50 lakh within 6 months), or Section 54F (net proceeds into a residential house). These exemptions must be planned before or shortly after the sale—they cannot be applied retroactively.

What TDS rate applies when an NRI sells property in India?

The buyer deducts TDS at 12.5% on LTCG (property held over 24 months) and up to 30% on STCG (held under 24 months). The NRI can apply to the Income Tax Department for a lower TDS certificate via Form 13 under Section 197 if actual liability is lower than the standard rate.

Can NRIs claim indexation benefits on capital gains in 2026?

Following Finance Act 2024, indexation benefits have been removed for most assets. The grandfathering option (20% with indexation vs. 12.5% without) for property acquired before July 23, 2024, applies only to resident individuals and HUFs—not NRIs. Consult a qualified tax adviser to confirm your position based on purchase date.

What is DTAA and how does it help NRIs?

A DTAA is a bilateral treaty between India and an NRI's country of residence that prevents the same income from being taxed twice. NRIs can claim a tax credit or exemption abroad for taxes paid in India by submitting a Tax Residency Certificate and Form 10F. Treaty terms vary by country and asset type.