₹5 crore is a serious number. But whether it funds a comfortable 30-year retirement or runs dry in 15 depends on where you live, how you spend, when you retire, and critically, how the corpus is invested and drawn down. This article examines each of those variables with actual numbers, not reassuring generalisations.

Key Takeaways

- ₹5 crore at a 4% withdrawal rate generates approximately ₹1.6–1.7 lakh per month — workable for moderate spenders, tight for affluent ones

- India-specific research puts the safer withdrawal rate at 2.6–3%, not 4%, given higher inflation and return volatility

- Healthcare inflation is the single biggest long-term threat to a fixed corpus

- Real return (nominal return minus inflation) is what determines whether your corpus lasts — not headline yield

- Structuring how you draw down matters as much as the corpus size itself

What Determines Whether ₹5 Crore Is "Enough" for Retirement in India?

₹5 crore is a starting point, not a finish line. How far it takes you depends on a set of personal and economic variables that play out very differently for each retiree.

Lifestyle and Monthly Expenditure

Three common spending profiles for Indian retirees:

| Profile | Monthly Spend | Pressure on ₹5 Crore |

|---|---|---|

| Modest | ₹75K–₹1 lakh | Highly manageable |

| Comfortable | ₹1.5–₹2.5 lakh | Works, requires discipline |

| Affluent | ₹3–₹5 lakh | Strained without growth investing |

Location changes everything. According to Economic Times data, a family in Delhi spends roughly ₹1.2 lakh per month versus ₹77,000 in Jaipur. Mercer's 2024 Cost of Living rankings confirm Mumbai is India's most expensive city, with New Delhi seeing a 13% rise in average rental costs between 2023 and 2024. For a retiree drawing on a fixed corpus, a 13% jump in housing costs alone can shave years off how long that corpus lasts.

Retirement Age and Longevity

The retirement timeline reshapes the entire calculation:

- Retire at 55 → corpus must last ~30 years

- Retire at 60 → corpus must last ~25 years

- Retire at 65 → corpus must last ~20 years

SEBI's own investor reference material uses a planning life expectancy of 83 years as a baseline, implying a 23-year post-retirement horizon from age 60. Given rising life expectancy in India, planning for at least 25–30 post-retirement years is prudent — especially for those in good health at retirement.

Dependents, Liabilities, and Legacy Goals

Longevity alone doesn't tell the full story. Many HNIs retire carrying obligations that extend well beyond their own lifestyle — a spouse's needs, children's higher education or wedding costs, ageing parents requiring care, or a clear desire to leave an inheritance.

Each of these adds real pressure to the corpus. A ₹5 crore figure that appears sufficient for two people's living expenses can look very different when it must also fund a child's education abroad or a meaningful bequest.

The Real Math: How Long Will ₹5 Crore Actually Last?

The most important concept in retirement planning isn't the nominal return on your portfolio. It's the real return — what remains after inflation.

If your portfolio earns 10% annually but inflation runs at 6%, your real return is roughly 4%. That 4% is what must fund your withdrawals and preserve your corpus. The Nifty 50 Total Return Index has delivered 12.74% annualised from 1995 to 2026 — but with annualised volatility of 21.13%. Average returns are not guaranteed returns.

The 4% Withdrawal Rule and What It Means for ₹5 Crore

The 4% rule — popularised by William Bengen's 1994 research — states that withdrawing 4% of your corpus annually, adjusted for inflation, is sustainable over 25–30 years. Applied to ₹5 crore:

- Annual withdrawal: ₹20 lakh

- Monthly income: ~₹1.67 lakh (approximately ₹1.6 lakh pre-tax)

This works — but only if the corpus remains invested in growth-oriented assets. Parking ₹5 crore entirely in fixed deposits defeats the purpose.

Indian retirees face a stricter constraint. Ravi Saraogi's 2022 SSRN paper computed the safe withdrawal rate for India specifically, arriving at 3% for the average investor and as low as 2.6% for conservative investors — materially lower than the US-derived 4% figure, due to India's higher inflation environment and return volatility.

At 3%, ₹5 crore supports ₹15 lakh per year, or ₹1.25 lakh per month. At 2.6%, that drops to roughly ₹1.08 lakh per month. For many metro-based retirees with comfortable lifestyles, these are constrained numbers.

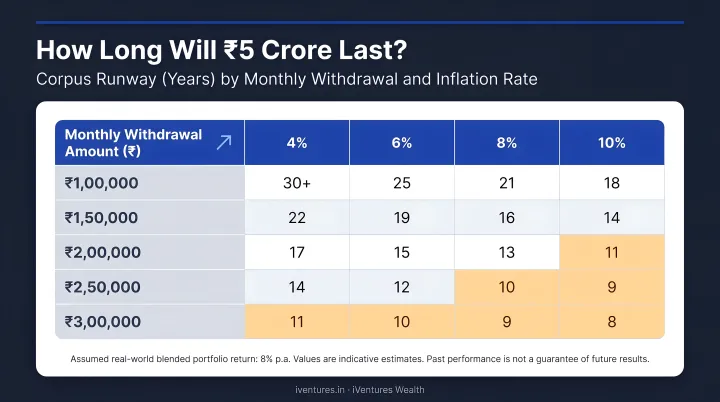

How Spending Level Changes the Corpus Runway

The table below illustrates how monthly withdrawal amounts affect corpus longevity at different inflation assumptions (assumes a balanced portfolio generating ~9–10% nominal returns):

| Monthly Withdrawal | Inflation Assumption | Approximate Corpus Runway |

|-------------------|---------------------|--------------------------|

| ₹1 lakh | 6% | 35+ years |

| ₹1.5 lakh | 6% | 25–28 years |

| ₹2 lakh | 6% | 18–22 years |

| ₹3 lakh | 6% | 12–15 years |

| ₹1.5 lakh | 8% | 18–20 years |

Indicative projections only. Actual outcomes depend on portfolio construction, sequence of returns, and actual inflation experienced.

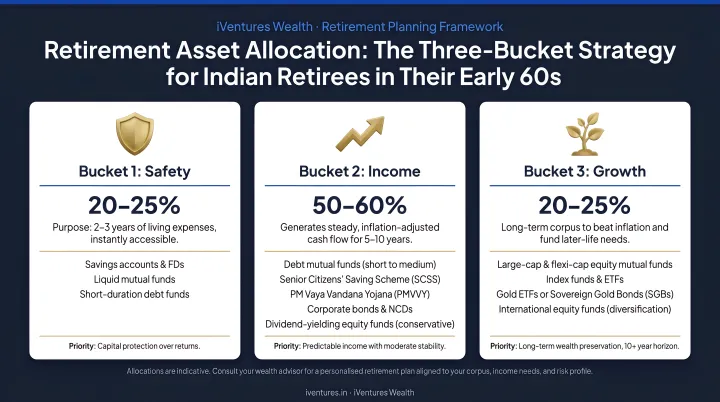

The Bucket Strategy: A Smarter Way to Draw Down

Rather than drawing from a single pool, the three-bucket approach significantly extends how long ₹5 crore lasts:

- Short-term bucket (1–3 years of expenses): Liquid funds, overnight funds, short-duration debt — preserved from market volatility

- Medium-term bucket (3–10 year horizon): Balanced advantage funds, high-quality bonds, corporate debt — moderate growth with stability

- Long-term bucket (10+ years): Equity mutual funds, PMS, select AIFs — growth assets that beat inflation over time

This structure addresses sequence of returns risk by ensuring near-term income is never dependent on equity market performance. iVentures Wealth applies this framework for HNI retirement clients — with a safety bucket holding 5–7 years of expenses in high-quality fixed income, a stability bucket covering the 8–15 year horizon, and a growth bucket in select equity and AIF strategies designed to compound over time.

The Hidden Risks That Can Quietly Erode a ₹5 Crore Corpus

Most retirement calculations focus on average returns and average inflation. The risks that actually derail retirements are structural and slow-moving — they don't show up on a spreadsheet until it's too late.

Four of these risks deserve close attention:

Healthcare Inflation

General CPI inflation was 2.82% year-on-year in May 2025 according to MOSPI — near multi-year lows. But health inflation ran at 4.34% in the same period and has historically trended higher than headline CPI. As retirees age, healthcare becomes an increasing share of total spending, not a stable line item.

National Health Accounts 2021-22 data shows household out-of-pocket health expenditure represents 39.4% of Total Health Expenditure in India — households still fund a large share of medical costs directly. For a retiree without adequate health insurance coverage, a single major illness can consume ₹20–50 lakh. Two or three such events over a 25-year retirement can seriously impair the corpus.

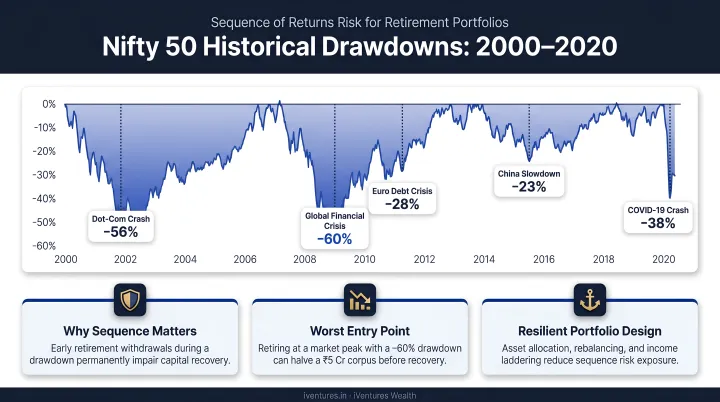

Sequence of Returns Risk

Market returns don't arrive as a smooth average. The Nifty 50 TRI has seen severe drawdowns at regular intervals:

- 51% during the dot-com crash (2000–2002)

- 59% during the 2008 global financial crisis

- 37% during the March 2020 COVID crash

If your portfolio suffers a sharp loss in years 1–3 of retirement — precisely when you're making early withdrawals — the damage is permanent. Later recoveries cannot undo it because the withdrawn capital never participated in the rebound.

This is why structured liquidity planning matters most in the first few years of retirement. Quarterly portfolio reviews and a clear withdrawal sequence can prevent forced selling at the worst possible time — when markets are down and the corpus is most vulnerable.

Longevity Risk and Lifestyle Creep

Two underappreciated risks:

- Outliving the corpus — retiring healthy at 55 with a 30-year runway demands genuine financial discipline, not just optimistic projections

- Lifestyle creep — early retirement, when energy and health allow travel, dining out, and new experiences, tends to cost more than planned. Spending in years 1–5 often runs 20–30% above what retirees budgeted

Tax Drag on Withdrawals

Poorly planned withdrawals create unnecessary tax leakage:

- Equity mutual fund LTCG: Gains above ₹1.25 lakh taxed at 12.5% (for transfers on or after 23 July 2024) under Section 112A

- Fixed deposit interest: Taxed at slab rates, though senior citizens can claim a ₹50,000 deduction under Section 80TTB

- NPS: 60% lump sum at age 60 is tax-exempt under Section 10(12A); annuity income is taxable

Drawing from instruments in the wrong order — for example, exhausting tax-efficient equity funds first while leaving taxable FD interest untouched — can reduce effective corpus value significantly over 20+ years.

How to Invest ₹5 Crore Post-Retirement to Make It Last

The investment strategy in retirement must shift from accumulation to preservation-with-growth. The goal isn't maximum returns — it's sustained, inflation-beating income that the corpus can generate for 25–30 years without running dry.

Asset Allocation for Retirees

A retiree in their early 60s needs equity in their portfolio. Not because equity is comfortable, but because fixed income alone cannot beat a 6–7% inflation rate over two decades. SEBI's own reference material for retired investors suggests 30% equities, 60% bonds, and 10% cash for someone five years from retirement — and researchers at Actuaries India recommend 40–50% equity allocation specifically for Indian retirement withdrawal portfolios to balance return needs against volatility.

A workable framework for a retiree in their early 60s:

- Equities (40–45%): Large-cap index funds, balanced advantage funds, select PMS strategies

- Debt and fixed income (40–45%): Short-to-medium duration debt funds, high-quality bonds, senior citizen FDs (current rates: up to 7.30% at SBI, up to 7.10% at ICICI)

- Liquid/cash buffer (10–15%): Overnight and liquid funds for immediate needs

This allocation should be reviewed and gradually de-risked as age increases — moving from 40% equity at 62 toward 25–30% equity by 75.

For HNIs managing ₹5 crore or more, a SEBI-registered investment adviser like iVentures Wealth can build a customised retirement portfolio spanning equity, debt, bonds, REITs, and private credit AIFs. The portfolio is structured around the three-bucket framework and reviewed quarterly to reflect both market conditions and life changes.

Tax-Efficient Withdrawal Planning

How you draw down your corpus matters as much as how it's invested. Strategic withdrawal sequencing can extend how long your ₹5 crore lasts:

- Draw from liquid bucket first for near-term expenses

- Use SWPs from equity funds rather than dividend options — LTCG treatment is more efficient than dividend taxation at slab rates

- Claim Section 80TTB deduction on senior citizen FD interest (up to ₹50,000)

- Plan NPS drawdown carefully — the 60% tax-exempt lump sum should align with broader tax planning for that year

- Harvest LTCG up to ₹1.25 lakh annually tax-free to systematically rebalance without tax cost

When ₹5 Crore May Not Be Enough — And What to Do About It

₹5 crore falls short in specific scenarios:

- Retiring before 55 with 30+ years ahead and India's conservative SWR of 2.6–3%

- Sustaining an affluent metro lifestyle of ₹3–4 lakh per month with international travel

- Significant healthcare needs or a family history requiring expensive long-term care

- Supporting dependents — children, ageing parents, or a spouse with different longevity

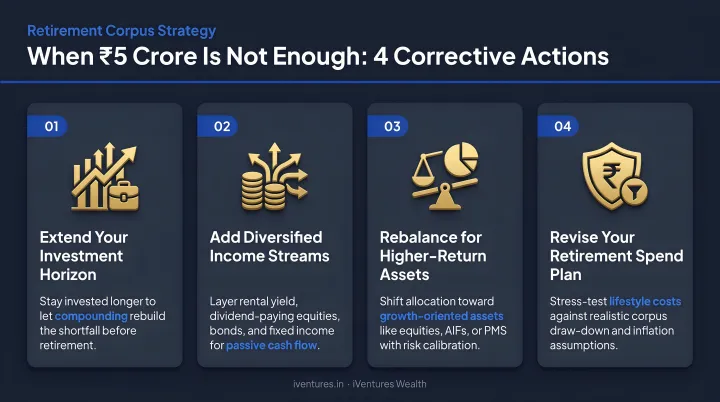

If you're in one of these categories, the corrective actions are concrete:

- Delay retirement by 2–3 years — a corpus growing at 10–12% annually can add ₹1–1.5 crore, meaningfully extending your runway without changing your lifestyle

- Supplement with part-time income in early retirement years, reducing corpus drawdown pressure when sequence risk is highest

- Increase the corpus target — ₹7–8 crore provides meaningfully more runway for higher-spending retirees

- Reduce discretionary spending selectively rather than across the board

If you're unsure whether your number holds up, that's the signal to move beyond rules of thumb. A formal retirement readiness assessment — stress-testing your corpus across inflation scenarios, withdrawal rates, and healthcare projections — gives you a defensible answer rather than a comfortable assumption. For most affluent investors, that assessment is the most valuable financial exercise they'll undertake.

Frequently Asked Questions

Is ₹5 crore corpus enough to retire in India?

For moderate spenders in Tier 2 cities or those with low fixed costs, ₹5 crore is generally sufficient. For metro-based retirees with higher lifestyle costs or early retirement timelines, it may fall short without careful investment planning and spending discipline.

How much interest will I get for ₹5 crore?

In a senior citizen fixed deposit at current rates (up to 7.10–7.30% annually), ₹5 crore generates roughly ₹35–36 lakh per year before tax. A growth-oriented portfolio can generate more, though returns vary. FD interest taxed at slab rates is rarely optimal as a standalone retirement income strategy.

How long will ₹5 crore last after retirement?

With a 4–5% annual withdrawal rate and a growth-oriented portfolio, ₹5 crore can last 25–35 years. The bucket strategy can extend this further. Monthly spending relative to the corpus is the single most important variable.

What monthly income can ₹5 crore generate in retirement?

At a 4% withdrawal rate, ₹5 crore generates approximately ₹1.6–1.7 lakh per month pre-tax. A more conservative 3% rate — closer to ₹1.25 lakh per month — tends to be more sustainable over a 30-year retirement in the Indian context.

Should I retire early if I have ₹5 crore?

Early retirement with ₹5 crore is possible, but it extends your drawdown horizon by a decade or more, amplifying both longevity and sequence-of-returns risk. It requires disciplined spending, a higher equity allocation, and a stress-tested withdrawal strategy before you exit employment.