Introduction

There's a financial paradox at the heart of many dental careers in India. Dentists earn well — often ₹20–40 lakh annually once established — yet arrive at retirement with no structured pension, no employer-funded safety net, and a savings window that is typically 8–10 years shorter than their salaried peers.

A BDS degree takes 4 academic years plus a compulsory one-year internship. An MDS adds another 3 years on top. By the time many dentists establish independent practice, their peers in salaried careers have already been contributing to EPF for nearly a decade.

Unlike those salaried professionals, dentists have no employer-provided provident fund, no defined benefit pension, and no TDS deducted at source. The entire retirement corpus must be built deliberately, from scratch, using personal discipline and the right instruments.

This article covers the core pillars of retirement planning for dentists in India — the unique financial challenges, the instruments that matter most, tax-saving strategies, and the insurance gaps that can derail even the best-laid plans.

Key Takeaways

- Dentists typically begin earning independently in their early 30s — every year of delay in starting SIPs compounds the cost significantly

- Without EPF, retirement is entirely self-funded — PPF, NPS, ELSS, and diversified equity are not optional, they're the plan

- Most dentists leave part of their ₹2 lakh annual tax deduction unclaimed — Sections 80C and 80CCD(1B) together cover the full amount

- A dental practice is a retirement asset, but only if valuation and succession planning begin years before exit

- Disability insurance covering the inability to practise dentistry specifically is the most underused protection in the profession

Why Dentists in India Need a Specialised Retirement Plan

The Income Structure Creates a False Sense of Security

A dentist earning ₹30 lakh a year and a salaried professional at the same income level are in fundamentally different financial positions. The salaried employee has EPF contributions flowing in automatically, group health cover, and TDS managing their tax liability throughout the year. The dentist has none of these.

Self-employed dentists must manage:

- No automatic EPF contributions from an employer

- No group health or disability cover

- Irregular income tied to clinic footfall and patient volume

- Overhead that consumes a substantial share of gross receipts — equipment costs, rent, lab fees, staff salaries, and consumables

This overhead burden makes it easy to indefinitely defer retirement savings. There is always a reason to reinvest in the clinic rather than in a PPF or mutual fund account.

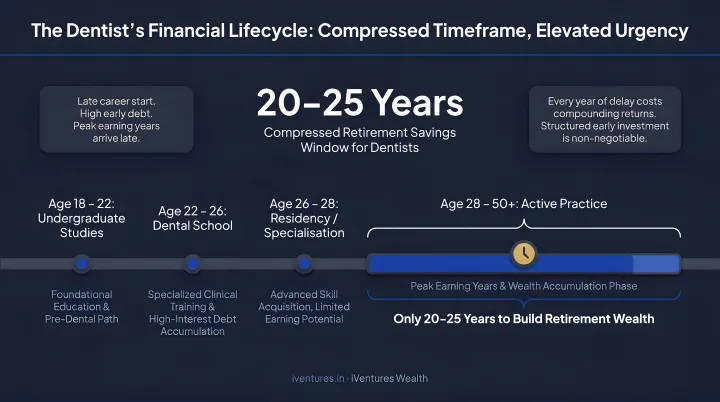

The Compressed Savings Window

Per DCI regulations, a BDS programme comprises 4 academic years plus a 1-year compulsory rotating internship. An MDS adds a further 3 years. A dentist who completes both degrees and then spends time building a practice often does not begin saving meaningfully until their early 30s — several years behind peers in other professions who started earning in their mid-20s.

Compounding rewards time more than it rewards amounts. Starting at 28 versus 38 can produce a materially different corpus by age 60, even with identical monthly contributions. Those lost years are unrecoverable — which is why the savings strategy must account for this compressed window from the outset.

The Physical Constraint on the Career Horizon

Research published in PMC found that musculoskeletal disorders affected 78.6% of dentists in the studied setting. A UK study on dental practitioners found that those who retired due to ill-health did so at a mean age of just 51.5 years — well short of any planned retirement date.

Carpal tunnel syndrome, chronic back problems, and eye fatigue are occupational realities for dentists. The physical demands of precision clinical work mean many dentists cannot, or choose not to, practise past 55–60. This shrinks the accumulation phase to as little as 20–25 years — making early, consistent investing the single most important variable in building a retirement corpus that actually lasts.

Building Your Retirement Corpus: Investment Instruments Every Dentist Should Know

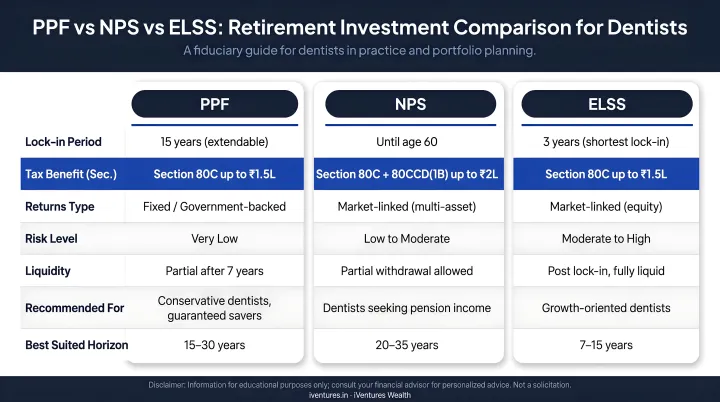

Public Provident Fund (PPF)

PPF is the foundation of any self-employed professional's retirement portfolio. It offers a triple tax exemption — contributions qualify under Section 80C, returns are tax-free, and the maturity amount is entirely exempt.

Key facts per the National Savings Institute:

- Minimum deposit: ₹500 per year; maximum: ₹1.5 lakh per financial year

- Current interest rate: 7.1% per annum (Apr–Jun 2026 quarter)

- Lock-in: matures after 15 complete financial years from account opening

- Partial withdrawals permitted from the 7th financial year

The 15-year lock-in enforces savings discipline and maximises compounding over time. A dentist who opens a PPF account at 30 and contributes the maximum every year will see that corpus compound at a tax-free rate through their most productive working decades.

National Pension System (NPS)

NPS is particularly valuable for self-employed dentists because it opens an additional tax deduction that salaried employees don't access as easily. Per the NPS Trust, self-employed subscribers can claim:

- Section 80CCD(1): up to 20% of gross income, subject to the overall ₹1.5 lakh Section 80C limit

- Section 80CCD(1B): an additional ₹50,000 deduction over and above the 80C limit

At retirement (age 60), NPS requires a minimum of 40% of accumulated wealth to be converted into an annuity; up to 60% can be taken as a lump sum. The equity exposure within NPS Tier I can generate meaningful long-term growth across a 20–30 year career horizon.

ELSS Mutual Funds

SEBI classifies ELSS funds as schemes that invest at least 80% in equity and equity-related instruments, offering Section 80C deductions up to ₹1.5 lakh per financial year. The lock-in is just 3 years — the shortest of any tax-saving instrument.

For dentists, systematic SIPs into ELSS over a 20–25 year career can build significant corpus while generating annual tax deductions. The equity orientation also means ELSS historically delivers returns that outpace inflation — critical for a corpus that must sustain 20–30 years of post-retirement life.

Diversified Equity Mutual Funds Beyond the 80C Limit

Once the 80C limit is exhausted, the next priority is building wealth through diversified equity — large-cap, flexi-cap, and index funds via ongoing SIPs. This is where portfolio construction matters most and where a research-driven approach to fund selection pays dividends over a long horizon.

Selecting the wrong funds, holding too many overlapping schemes, or staying overweight in one sector can steadily erode returns over a 20-year period. iVentures Wealth, a SEBI-registered investment adviser with a CFA-led research team, works with professionals to build customised mutual fund portfolios — screening for consistent compounders, eliminating high-cost underperformers, and aligning the portfolio to specific retirement timelines.

Fixed Deposits and Debt Instruments

As dentists approach retirement, capital preservation takes priority over growth. FDs, RBI Floating Rate Bonds, and debt mutual funds provide stability, predictable income, and low correlation to equity market swings. These instruments are less exciting in the accumulation phase but become critical in the 5–10 years before and after retirement.

In the five years before retirement, shifting a portion of equity gains into these instruments locks in wealth already built — protecting it from a poorly timed market downturn just before you need it most.

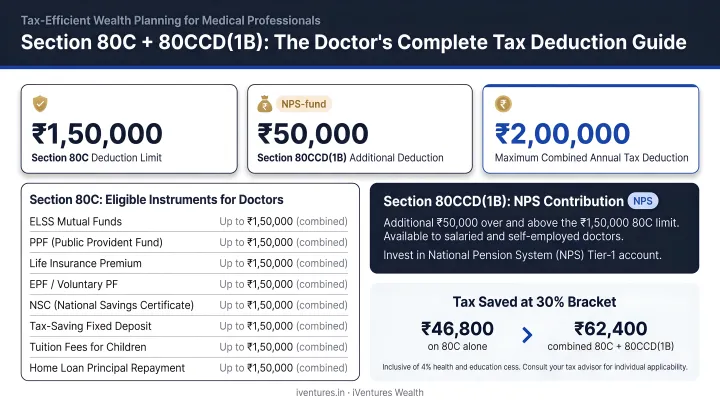

Tax-Efficient Strategies to Maximise Retirement Savings

Maxing Out Section 80C

The Section 80C deduction allows up to ₹1.5 lakh per financial year. Many dentists fill this inconsistently or sub-optimally — using it partially for life insurance premiums while leaving capacity unused.

The most tax-efficient instruments to fill the 80C bucket:

- PPF contributions

- ELSS mutual fund SIPs

- Life insurance premiums

- Principal repayment on home loans

Prioritise PPF and ELSS over insurance-linked investment products (ULIPs), which are less efficient on both return and cost.

Section 80CCD(1B): The Underused ₹50,000 Deduction

This is the most underutilised tax break available to self-employed professionals in India. Contributing to NPS Tier I unlocks an additional ₹50,000 deduction over and above the ₹1.5 lakh Section 80C limit.

A dentist who maxes both simultaneously reduces taxable income by ₹2 lakh annually — at a 30% tax bracket, that's ₹60,000 in tax saved each year, which is itself an investable amount.

Structuring the Practice as an LLP or Private Limited Company

Dentists operating as sole proprietors bear the full personal tax burden on practice income. Operating under a registered LLP or private limited company structure changes this materially.

Under Section 37(1) of the Income Tax Act, non-capital business expenditure laid out wholly and exclusively for the profession is deductible when computing profits. This includes:

- Equipment depreciation

- Clinic rent

- Staff salaries

- Consumables and lab fees

Deploying surplus funds from within a private limited company structure — rather than drawing them as personal income — allows wealth to accumulate at the corporate tax rate and defers personal taxation over multiple years. iVentures Wealth has worked with business owners to structure exactly this kind of approach, building investment strategies around company capital rather than post-tax personal income.

LTCG Tax Planning on Equity Investments

The Budget 2024 (PIB/CBDT notification) raised the LTCG exemption on financial assets from ₹1 lakh to ₹1.25 lakh per year, with gains beyond that threshold taxed at 12.5%. For listed equities, the long-term holding period remains 12 months.

A dentist with an equity portfolio that has grown significantly over a 15–20 year career should plan annual gain-booking to stay within the ₹1.25 lakh exemption each year, rather than allowing unrealised gains to accumulate and triggering a large LTCG liability in a single year.

Retirement Planning by Career Stage: A Roadmap for Dentists

Early Career (Ages 25–35): The Foundation Phase

The priority here isn't maximising investment amounts — it's building habits and systems that compound over time.

- Open PPF and NPS Tier I accounts immediately

- Start SIPs even at ₹5,000–₹10,000/month into ELSS and a diversified equity fund

- Clear high-interest education debt aggressively before scaling investments

- Build an emergency fund covering 6 months of expenses before committing heavily to long-term instruments

- Start now, not later. The compounding gap between starting at 28 versus 38 is permanent and irreversible

Mid-Career (Ages 35–48): The Acceleration Phase

By this stage, practice income is stable enough to shift from cautious to deliberate. Scale up with intent:

- Increase SIP amounts in line with income growth — target directing 20–30% of take-home toward retirement instruments

- Diversify into direct equity and real estate beyond the standard tax-saving instruments

- Max out NPS contributions annually to capture the full 80CCD(1B) deduction

- Review term insurance and critical illness cover — this is the phase where income is highest and dependants' reliance is greatest

- Start planning practice succession 10–15 years out: a well-structured exit takes time to execute

Pre-Retirement (Ages 48–58): The Consolidation Phase

The focus moves from building the corpus to protecting it. Priorities shift accordingly:

- Gradually reduce equity allocation; increase exposure to debt instruments, bonds, and liquid funds

- Stress-test the corpus against estimated post-retirement expenses, adjusted for inflation

- Firm up the practice exit strategy — whether outright sale, partnership buyout, or gradual handover to an associate

- Work with a wealth adviser to build a post-retirement income plan from the corpus, accounting for healthcare costs, lifestyle expenses, and legacy goals

Your Practice as a Retirement Asset: Valuation and Succession Planning

For many Indian dentists, the clinic itself — its patient base, goodwill, location, and equipment — is among their most significant financial assets. Yet it often goes unexamined as part of retirement planning until it's too late to maximise its value.

How Dental Practice Valuation Works

Practice valuation typically considers a combination of:

- Revenue and profitability (EBITDA as a baseline)

- Patient base size, loyalty, and recurring appointment frequency

- Location quality and lease terms

- Equipment condition and remaining useful life

- Reputation and referral network

India's dental services market was valued at $3 billion, with organised chains accounting for less than 10% of practices — meaning most clinics remain independently owned. This creates both an opportunity (dental chains are actively acquiring) and a risk (without preparation, an independent practice can be significantly undervalued at sale).

Succession Options

Dentists have several exit routes:

- Outright sale to a younger dentist or a dental chain

- Partnership with buyout provision — bringing in a junior partner over 3–5 years with a pre-agreed buyout formula

- Gradual wind-down — transitioning clinical work to an associate while remaining in a consulting or supervisory role

Poorly planned exits consistently result in undervalued sales. A practice that took 25 years to build should not be sold in 6 months under time pressure. Starting the succession conversation at 45–48 rather than 57 makes a material difference to the exit value.

Tax Implications of Selling a Practice

The exit structure also determines your tax liability — so succession planning and tax planning need to happen together.

The tax treatment depends on what is being sold:

- Tangible assets (equipment, furniture) — governed by Section 50 of the Income Tax Act as capital gains on depreciable assets

- Goodwill/intangibles — governed by Section 55; self-generated goodwill may be treated as having a nil cost of acquisition, which has significant tax implications

Advance tax planning with a qualified adviser before the sale can reduce the liability on exit proceeds substantially. iVentures Wealth works with business owners navigating significant liquidity events, structuring post-exit portfolios across asset classes to ensure proceeds are deployed efficiently rather than sitting idle in deposits.

Disability Insurance: The Missing Piece in Dentist Retirement Planning

A dentist's income is entirely dependent on their physical ability to perform precision clinical work. This is not a generic professional risk — it is specific to the demands of dentistry: fine motor control, sustained posture, visual concentration, and repetitive hand movements over 6–8 hours a day.

Research published in PMC found musculoskeletal disorders in 78.6% of dentists in the studied population. A UK ill-health retirement study found dental practitioners who retired due to ill health did so at a mean age of 51.5 years. For Indian dentists, the risk is compounded by high patient loads and limited ergonomic infrastructure in most private practice settings.

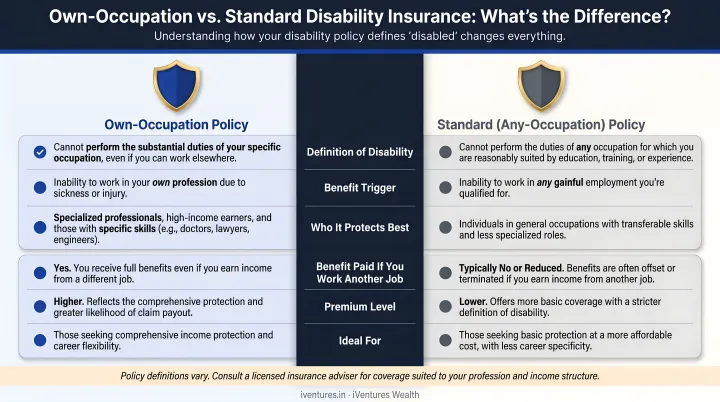

Own-Occupation vs. Standard Disability Policies

Standard personal accident and disability policies in India typically define total disablement as the inability to engage in any occupation — meaning a dentist who can no longer practise dentistry but can theoretically do desk work may not be eligible for a claim.

Own-occupation disability insurance, by contrast, pays benefits if the insured cannot perform the duties of their specific occupation — dentistry — regardless of whether they could work in another field. For a profession where the ability to hold a handpiece is the income, this distinction matters more than it does in almost any other field.

While iVentures Wealth does not sell insurance products directly, any comprehensive financial plan for a dentist should map insurance gaps across:

- Disability income protection (preferably own-occupation or equivalent)

- Critical illness insurance covering major conditions that could interrupt practice

- Term life insurance sized to replace income and protect corpus-building if the dentist dies prematurely

Without this coverage, a single health event can undo years of disciplined saving — and leave a dentist financially exposed at precisely the moment they are least able to recover.

Frequently Asked Questions

At what age do most dentists retire in India?

There is no mandated retirement age for dentists in private practice in India. Most independent practitioners retire between 55–65, with physical stamina and financial readiness being the primary drivers. Planning earlier gives dentists the option to retire on their own terms rather than the profession's.

What do dentists do when they retire?

Post-retirement options include a full exit or a phased wind-down through consulting, mentoring, dental education, or academic roles. Each path requires a different corpus size — a dentist earning consulting income needs less capital buffer than one with no practice-related income.

How much retirement corpus does a dentist need in India?

A standard starting benchmark is the 25x rule: accumulate 25 times your expected annual expenses. iVentures Wealth refines this further based on healthcare costs, lifestyle expectations, inflation, and practice exit proceeds. A personalised calculation with a SEBI-registered adviser gives you an accurate target.

When should a dentist start retirement planning in India?

The moment they begin earning, even as an associate. Starting SIPs and opening PPF/NPS accounts early matters more than the initial amount. Starting at 28 versus 38 creates a compounding gap that larger contributions later simply cannot close.

What tax-saving instruments are most effective for dentists?

PPF, ELSS, and NPS form the most impactful combination. Together, Section 80C (up to ₹1.5 lakh) and Section 80CCD(1B) (additional ₹50,000) allow dentists to reduce taxable income by up to ₹2 lakh annually — benefits that compound over a 25-year career.

Should a dentist invest in expanding the clinic or in financial assets for retirement?

Both serve different purposes and should be treated as complementary. Practice investment builds the business asset and its eventual sale value. Financial assets provide a retirement corpus independent of practice performance. Neglecting either creates a vulnerable plan — the goal is a balanced allocation between the two.