Under the Income Tax Act, 1961, rental income from Indian property is always taxable in India, regardless of where you live. Section 5 and Section 9 of the Act make this unambiguous: income arising from property situated in India is Indian-source income, full stop. What many NRIs miss are the deductions, treaty protections, and compliance steps that can substantially reduce—and sometimes recover—that tax.

This guide covers how rental income is calculated and taxed, which deductions NRIs can claim, how TDS compliance works for both landlords and tenants, the deemed rent trap for multiple properties, and how DTAA prevents double taxation.

Key Takeaways

- Rental income from Indian property is taxable in India; tenants must deduct TDS at 31.2% under Section 195 with no minimum rent threshold

- NRIs can reduce taxable income via the 30% standard deduction on NAV, municipal tax deductions, and home loan interest under Section 24(b)

- Owning more than two residential properties triggers the deemed rent rule, meaning vacant third properties are taxed on notional rental income

- India's DTAAs with the USA, UK, Canada, UAE, and Australia allow NRIs to claim foreign tax credits and avoid paying tax on the same income twice

- File your ITR if total Indian income exceeds ₹2.5 lakh (old regime) or ₹4 lakh (new regime) — it's also the only way to claim TDS refunds

How Rental Income Is Taxed for NRIs: The NAV Framework and TDS Basics

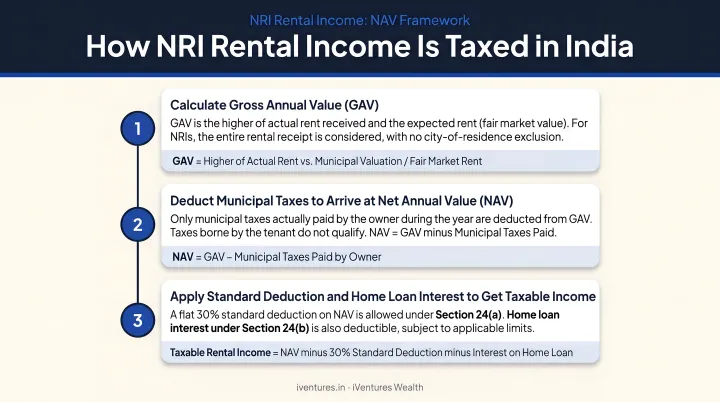

Calculating Taxable Rental Income Using NAV

Taxable rental income for NRIs isn't simply the rent collected. It's calculated through the Net Annual Value (NAV) framework, which works in three steps:

- Start with Gross Annual Rent — the total rent receivable for the year

- Subtract municipal taxes — only taxes actually paid by the owner during the financial year qualify

- Apply a 30% standard deduction on the resulting NAV under Section 24(a)

Example:

| Step | Amount |

|---|---|

| Gross Annual Rent | ₹6,00,000 |

| Less: Municipal taxes paid | ₹30,000 |

| Net Annual Value (NAV) | ₹5,70,000 |

| Less: 30% standard deduction | ₹1,71,000 |

| Taxable House Property Income | ₹3,99,000 |

Note that rental income is taxed on an accrual basis, not receipt. If rent was due in March but paid in April, it's still taxable in the earlier financial year.

This accrual treatment also determines when TDS obligations are triggered — which brings us to what tenants must deduct.

TDS Under Section 195: What Tenants Must Deduct

Section 195 applies to all payments made to non-residents that are chargeable under the Act. For rental income, this means:

- TDS is deducted at 31.2% (30% base rate + 4% health and education cess)

- No minimum threshold—unlike Section 194I for resident landlords, which kicks in only above ₹2.4 lakh annually

- Deduction applies at the time of credit or payment, whichever is earlier

For higher-income NRIs, a surcharge applies on top of the base rate:

| Income Slab | Surcharge | Effective TDS Rate |

|---|---|---|

| Up to ₹50 lakh | Nil | 31.2% |

| ₹50 lakh – ₹1 crore | 10% | 34.32% |

| ₹1 crore – ₹2 crore | 15% | 35.88% |

| ₹2 crore – ₹5 crore | 25% | 39.0% |

| Above ₹5 crore (new regime) | 25% | 39.0% |

| Above ₹5 crore (old regime) | 37% | 42.744% |

Old Regime vs. New Regime: Key Differences

NRIs can choose between two tax regimes, and the decision has real implications for their net rental income:

- Old regime: Allows home loan interest deduction (Section 24b), principal repayment (Section 80C), and other deductions; often better for NRIs with significant loans on let-out properties

- New regime: Lower slab rates, but no deduction for home loan interest on self-occupied properties; the 30% standard deduction on let-out properties remains available under both regimes

Where home loan interest on a let-out property exceeds rental income, the resulting loss can be set off against other income — capped at ₹2 lakh per assessment year — and carried forward for up to 8 years under Section 71B.

Tax Deductions NRIs Can Claim to Reduce Their Rental Income Tax

Standard Deduction (Section 24a)

Every NRI earning rental income gets a flat 30% deduction on the NAV—automatically, regardless of actual repair or maintenance costs. This applies to let-out properties under both the old and new tax regimes. No documentation required.

Municipal Tax Deduction

Municipal/property taxes can be deducted from gross rent, but only if:

- The taxes were actually paid by the NRI during the financial year

- Outstanding dues or arrears don't qualify

- Taxes paid by the tenant on the NRI's behalf don't qualify either

Home Loan Interest Under Section 24(b)

This is one of the most significant deductions available:

- Let-out property (old regime): Full interest on home loan deductible with no upper cap, including 1/5th of pre-construction interest spread over five years

- Self-occupied property (old regime): Capped at ₹2 lakh per year (₹30,000 for repair/renewal loans)

- New regime: No interest deduction for self-occupied properties; let-out property interest remains deductible

Additional Deductions Under the Old Regime Only

- Section 80C: Up to ₹1.5 lakh deduction on home loan principal repayment, subject to the aggregate Section 80C limit

- Section 80EE: Additional ₹50,000 on interest for qualifying first-time homebuyer loans (loan sanctioned between April 1, 2016 and March 31, 2017; loan amount not exceeding ₹35 lakh; property value not exceeding ₹50 lakh)

Neither Section 80C nor Section 80EE deductions are available under the new tax regime.

Lower TDS Certificate Under Section 197

If an NRI's actual tax liability—after applying all deductions—is well below 31.2%, that gap creates a significant cash-flow problem. The TDS is deducted upfront; the refund comes only after filing the ITR.

The solution: apply to the Assessing Officer under Section 197 via Form 13, submitting income projections and supporting documents. If approved, the AO issues a certificate authorising the tenant to deduct TDS at a reduced rate. For NRI landlords managing significant rental portfolios, this is one of the most effective ways to avoid over-deduction and preserve cash flow through the year. iVentures Wealth routinely structures this as part of broader NRI TDS planning, ensuring clients aren't waiting on refunds that could be avoided upfront.

TDS Compliance and ITR Filing: A Step-by-Step Guide for Landlords and Tenants

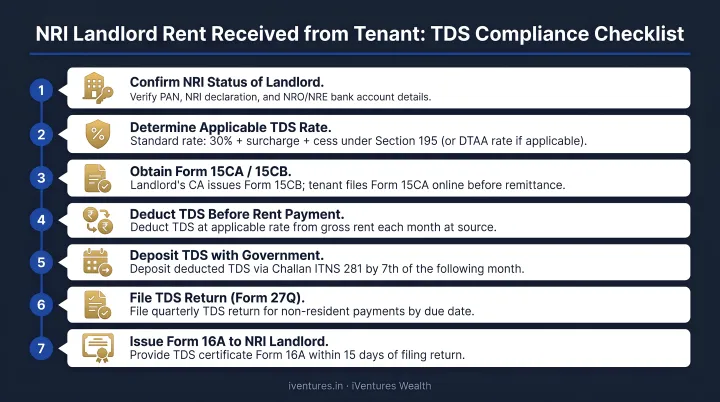

Tenant's TDS Obligations: A Step-by-Step Process

Tenants renting from an NRI landlord carry the full compliance burden. The steps, in order:

- Obtain a TAN (Tax Deduction Account Number) from the NSDL website under Section 203A

- Deduct 31.2% TDS from every rent payment

- Deposit TDS using Challan ITNS 281 by the 7th of the following month

- File Form 15CA online on the income tax portal before each rent remittance

- Obtain Form 15CB from a Chartered Accountant if annual rent exceeds ₹5 lakh—this must be done before submitting Form 15CA

- File quarterly TDS returns using Form 27Q

- Issue Form 16A to the NRI landlord within 15 days of filing the quarterly return

The most common tenant error: failing to identify the landlord as an NRI and not deducting TDS at all. It is the tenant's legal responsibility to verify residential status. A failure to deduct attracts a penalty equal to the full undeducted TDS amount — regardless of whether the tenant knew the landlord's status.

NRI Landlord's Documentation and Monitoring Duties

NRI landlords aren't passive participants in this process. Key obligations include:

- Maintain updated lease agreements that clearly state NRI status

- Collect and retain all Form 16A TDS certificates from tenants

- Ensure rental income is credited to an NRO account (or NRE account only if the tenant is also an NRI paying from an NRE account)

- Regularly check Form 26AS and the Annual Information Statement (AIS) on the income tax portal to confirm TDS has been correctly deposited and reported

ITR Filing Deadlines and Thresholds

NRIs must file an Income Tax Return in India if total Indian income exceeds ₹2.5 lakh (old regime) or ₹4 lakh (new regime). The standard filing deadline is July 31st of the assessment year.

Even below these thresholds, filing is advisable — it's the only way to recover refunds when TDS deducted exceeds actual tax liability.

Penalties for Non-Compliance

Missing any of the obligations above carries real financial and legal consequences:

- Tenant who fails to deduct TDS: Penalty equal to the undeducted TDS amount under Section 271C

- Non-payment of deducted TDS: Rigorous imprisonment from 3 months to 7 years under Section 276B, plus fine

- NRI landlord who fails to report income: Income tax penalties and potential scrutiny in both India and the country of residence

The Deemed Rent Rule: What NRIs with Multiple Properties Must Know

How Deemed Rent Works

When an individual owns more than two residential properties, the third (and any additional) property is treated as "deemed let-out"—even if it sits completely vacant. The estimated market rent it could fetch is added as taxable income.

NRIs can designate any two properties as self-occupied. The strategic move: designate the two with the highest potential rent as self-occupied, minimising the deemed income on which tax is payable.

The Five Property Scenarios

| Scenario | Tax Treatment |

|---|---|

| One property, not rented | Self-occupied, no tax |

| One property, rented out | Rental income taxed normally |

| Two properties, one rented | Tax only on the rented property |

| Two properties, neither rented | One deemed self-occupied, one deemed let-out—notional rent taxed |

| Three or more properties | Only two can be self-occupied; remaining properties attract deemed rent regardless of vacancy |

Many NRIs who have inherited multiple properties in India are caught off-guard by scenarios four and five. The assumption that "if there's no tenant, there's no tax" simply doesn't hold once a third property enters the picture.

This gap can result in unexpected tax liability year after year—making it worth reviewing your property portfolio before the next filing cycle.

If you own more than two Indian properties, consult a tax advisor to determine which properties to designate as self-occupied and review your overall tax exposure. iVentures Wealth's NRI advisory team helps clients map their full real estate footprint, assess deemed rent exposure, and integrate property decisions into a tax-efficient wealth structure—drawing on 20+ years of cross-border advisory experience.

DTAA Benefits and Smart Tax Planning for NRI Landlords

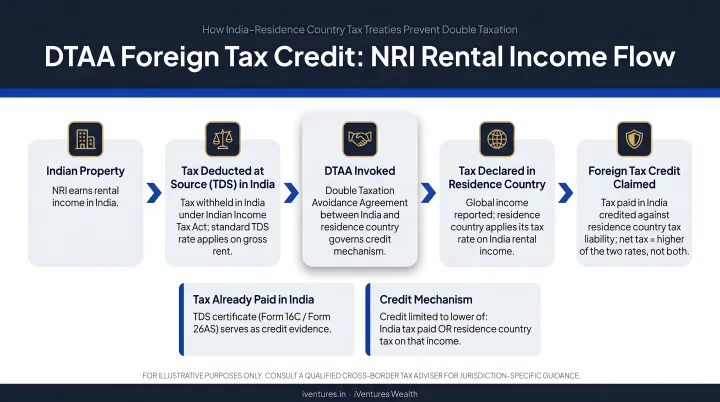

How DTAA Prevents Double Taxation

India maintains Double Taxation Avoidance Agreements with the USA, UK, Canada, UAE, Australia, and many other countries. Under the official DTAA framework, NRIs can typically:

- Claim a tax credit in their country of residence for taxes already paid in India (the credit method—used by the USA, UK, Canada, and Australia)

- Claim an exemption where the treaty specifically provides for it (less common for immovable property income)

The applicable method depends on the specific DTAA between India and the NRI's country of residence. Critically, Indian TDS is not eliminated by a DTAA—Indian tax on Indian-source property income is preserved under virtually every treaty's Article 6 (Immovable Property). The treaty provides relief in the residence country, not India.

A Practical Example: US-Based NRI

A US-based NRI earns ₹6,00,000 in annual rental income from an Indian property. After the 30% standard deduction, taxable income is approximately ₹3,99,000. The tenant deducts 31.2% TDS on the gross rent—₹1,87,200.

On the US tax return, this NRI can claim a Foreign Tax Credit via IRS Form 1116 for the Indian taxes paid, subject to US foreign tax credit rules. The result: the same income is not taxed twice. To invoke DTAA benefits, the NRI must provide a Tax Residency Certificate (TRC) along with Form 10F, filed electronically on the Indian income tax portal. The NRI must still file an ITR in India to remain compliant.

When Expert Guidance Makes the Difference

Navigating DTAA claims, Section 197 applications, tax regime selection, Form 15CA/15CB compliance, and ITR filings across jurisdictions isn't a one-time exercise. It's an ongoing, multi-country obligation that demands coordination between advisors in both countries.

iVentures Wealth coordinates DTAA optimisation, TDS planning, and ITR compliance for NRI clients across the US, UK, UAE, Canada, Singapore, and Australia. With 20+ years of experience and SEBI RIA registration (INA000019026), the firm works alongside tax advisors in both jurisdictions to align India-side compliance with the NRI's home-country filing obligations. For NRI landlords with ₹5 crore or more in investable assets, this cross-border coordination is built into a broader wealth management strategy — not treated as a standalone CA filing task.

Frequently Asked Questions

Do NRIs have to pay tax on rental income in India?

Yes. All rental income from property located in India is taxable in India under the Income Tax Act, 1961, regardless of where the NRI resides. The tenant is legally responsible for deducting TDS at 31.2% at source before making any rent payment.

How much rental income is tax-free for NRIs?

There is no automatic basic exemption limit on rental income. After the 30% standard deduction and other eligible deductions, taxable income is significantly reduced. ITR filing is mandatory only if total Indian income exceeds ₹2.5 lakh (old regime) or ₹4 lakh (new regime), with applicable slab rates determining tax owed beyond those thresholds.

What is the TDS limit for rent paid to an NRI landlord?

There is no minimum threshold. Unlike Section 194I—which applies to resident landlords and has a ₹2.4 lakh annual threshold—Section 195 applies to every rent payment made to an NRI, regardless of amount. TDS at 31.2% must be deducted from the very first payment.

Can NRIs claim deductions on rental income in India?

Yes. NRIs can claim the 30% standard deduction on NAV, deduct municipal taxes paid, and under the old regime, claim home loan interest under Section 24(b) and principal repayment under Section 80C. If actual tax liability is lower than the 31.2% TDS rate, NRIs can apply for a lower TDS certificate under Section 197 via Form 13.

What happens if the tenant doesn't deduct TDS on rent paid to an NRI?

The tenant faces a penalty equal to the undeducted TDS amount under Section 271C, and failure to deposit deducted TDS can result in imprisonment of 3 months to 7 years under Section 276B. The NRI landlord must self-declare the income and pay advance tax directly to remain compliant.

How can NRIs avoid double taxation on Indian rental income?

NRIs in countries with which India has a DTAA can claim either an exemption or a tax credit for taxes paid in India when filing returns in their country of residence. A Tax Residency Certificate (TRC) and Form 10F are required to invoke DTAA benefits. The NRI must still file an ITR in India to remain compliant with Indian tax law.