Introduction

Most Indian HNI and UHNI investors still hold their fixed income portfolios almost entirely in domestic instruments — G-Secs, corporate bonds, debt funds. That worked when the rupee held steady and domestic yields were competitive. Neither condition holds today. The rupee has depreciated over 37% against the dollar in the last decade (from ₹61.03 in 2014 to ₹83.67 in 2024, per World Bank data), domestic rate cycles have grown more volatile, and global credit markets now offer yield environments that don't exist within Indian borders.

Three specific gaps make that domestic concentration a structural liability: correlation risk, yield limitations, and single-currency exposure. This article explains what global bonds are, what measurable portfolio advantages they provide, and how to size them correctly within a broader fixed income strategy.

Key Takeaways

- Global bonds are debt instruments issued across multiple international markets, offering access to differentiated yield curves and credit spreads.

- They reduce correlation to domestic Indian assets — providing a buffer when RBI rate cycles or credit events hit domestic portfolios.

- The INR has lost over 37% of its value against the USD in the past decade, making foreign currency exposure a concrete portfolio consideration.

- Hedged global bonds historically showed a -13.6% maximum drawdown vs. -24.2% for unhedged versions over 10 years (BNY, 2025).

- Indian investors can access global bonds via LRS, international fund-of-funds, or global ETFs, each carrying distinct tax and compliance considerations.

What Are Global Bonds?

A global bond is a debt instrument issued simultaneously across multiple international markets — typically denominated in major currencies like USD, EUR, or JPY — allowing issuers to raise capital globally and investors to participate in international fixed income markets.

They are issued by three main types of entities:

- Sovereign governments — national governments raising debt in foreign markets

- Multinational corporations — large companies accessing cheaper or broader capital pools

- Supranational bodies — institutions like the World Bank, which issued a USD 6 billion 7-year global bond in January 2025 with an order book exceeding USD 12.6 billion, drawing investors from EMEA, the Americas, and Asia

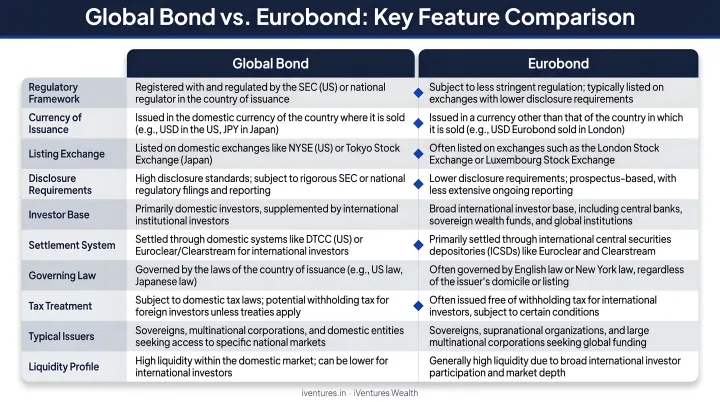

How Global Bonds Differ from Eurobonds

The distinction matters for Indian investors evaluating what they're actually buying:

| Feature | Global Bond | Eurobond |

|---|---|---|

| Where traded | Home country + international markets | Outside the issuer's home currency country |

| Currency | Often in issuer's home currency or major foreign currency | Typically foreign to the issuer |

| Market access | Broadest — listed across multiple exchanges | International, but not in the home market |

A real-world Indian example: Reliance Industries priced a USD 4 billion multi-tranche offering in January 2022 — including 10-year, 30-year, and 40-year tranches — distributed across US and international markets simultaneously under Rule 144A/Regulation S. This is what global bond issuance looks like at scale.

Global bonds are not an exotic asset class. For Indian investors, they are a practical tool for accessing yield environments, credit markets, and currencies that the domestic bond market cannot replicate.

Key Benefits of Global Bonds

The three advantages below focus on portfolio-level outcomes — how global bonds measurably improve risk-adjusted returns, open yield opportunities, and manage macro risk. Each maps to metrics that serious fixed income investors track.

Portfolio Diversification and Reduced Correlation

When Indian equity or bond markets face stress — a sharp RBI tightening cycle, a domestic credit event, sovereign risk concerns — globally diversified fixed income allocations can cushion drawdowns. The core reason: foreign rate cycles and credit conditions operate on entirely different timelines than India's.

This isn't theoretical. The stock-bond correlation itself is regime-dependent, as the BIS noted — it turned positive in mid-2021 during inflation-driven volatility, meaning domestic bonds stopped offsetting equity risk precisely when investors needed that buffer most. Global bond markets, running on different inflation and rate cycles, can provide what domestic bonds no longer offer during those periods.

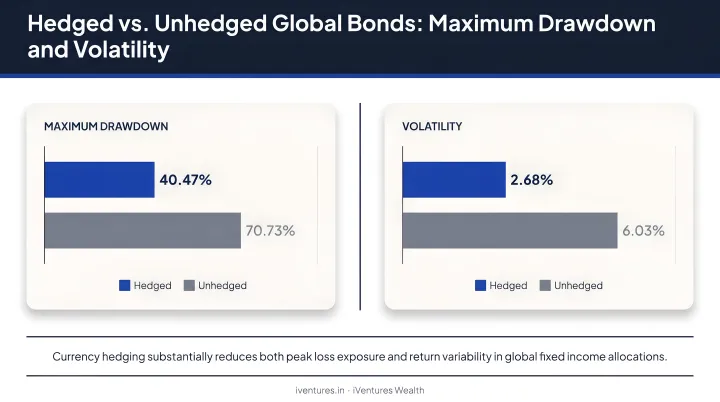

The hedging dimension amplifies this. According to BNY Investments research, over the 10 years ending September 30, 2025:

- Hedged Bloomberg Global Aggregate: Maximum drawdown of -13.6%

- Unhedged Bloomberg Global Aggregate: Maximum drawdown of -24.2%

Hedged versions also showed nearly half the volatility of unhedged positions. Vanguard's global fixed income research adds that hedged global bonds delivered risk-adjusted returns approximately 2.9 times greater than unhedged versions on average.

KPIs this improves: Portfolio volatility (standard deviation), maximum drawdown, Sharpe ratio, correlation coefficient to domestic equity index.

When it matters most: RBI tightening cycles, domestic credit stress, rupee depreciation spikes, Indian sovereign risk events — the moments when a purely domestic portfolio has no offsetting position.

Access to Differentiated Yield Opportunities

Different economies sit at different points in their rate cycles at any given time. Global bonds let investors capture yield from markets that are out of sync with India — sometimes offering better risk-adjusted returns even when India's absolute yields appear competitive.

Verified yield comparison (end-2024):

| Market | Instrument | Yield (Dec 31, 2024) |

|---|---|---|

| India | 10-year G-Sec | 6.76% |

| United States | 10-year Treasury | 4.48% |

At face value, India appears to offer higher yields. But risk-adjusted yield — accounting for currency risk, credit risk, and portfolio diversification benefit — shifts the comparison materially once hedging costs and diversification benefit are factored in.

The BNY illustration using Japanese government bonds shows how this works in practice: an unhedged JGB yield of 3.18% transformed into an approximate USD-hedged yield of 6.68–6.70% after accounting for the differential between US and Japanese policy rates. The underlying principle — that rate differentials between two markets can substantially enhance effective yield through currency hedging — applies to any investor navigating cross-border fixed income, including from an INR base.

For UHNIs and family offices managing large fixed income allocations, even a 50–75 basis point improvement in risk-adjusted yield across a significant corpus has material compounding value over a 5–10 year horizon.

KPIs this improves: Portfolio yield-to-maturity, income generated, total return over 3–5 year periods, risk-adjusted return versus benchmark.

When it matters most: When Indian domestic bond markets are in a low-spread phase, or when rate hike cycles have compressed bond prices — global diversification allows investors to seek better value without abandoning fixed income entirely.

Currency Diversification and Macro Risk Management

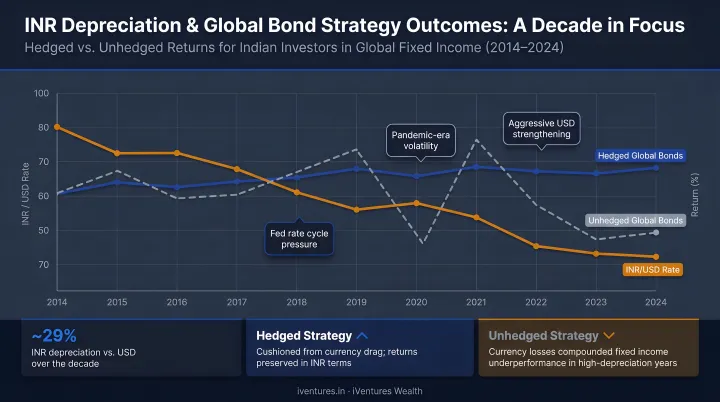

The INR's long-run trajectory against the dollar is one of the clearest arguments for foreign currency exposure in any Indian investor's portfolio. World Bank official exchange rate data shows the INR moved from 61.03 per USD in 2014 to 83.67 in 2024 — a 37.10% increase in rupees required to buy one dollar over that period.

A 37% depreciation over a single decade is a baseline planning assumption, not an outlier scenario.

The hedged vs. unhedged decision works as follows:

- Unhedged global bonds gain in INR terms when the rupee weakens — providing a natural cushion during periods of currency stress. Reuters confirmed the INR fell 10.14% in 2022, its worst annual decline since 2013.

- Hedged global bonds eliminate currency volatility but still deliver the interest rate and credit diversification benefit — typically lower volatility, as the drawdown data above confirms.

Neither approach is universally superior. The right choice depends on the investor's INR outlook, foreign currency liabilities, and risk tolerance.

For Indian HNIs or NRIs with USD-denominated goals — international education, overseas property, foreign travel — global bonds provide a natural match for those future outflows. For purely domestic investors, the currency layer adds diversification that Indian bonds structurally cannot provide.

KPIs this improves: Currency-adjusted total return, portfolio drawdown during INR depreciation events, real return, portfolio concentration in INR-denominated assets.

When it matters most: Global risk-off sentiment triggering capital outflows from India, current account deficit widening, aggressive Fed rate hike cycles — each a scenario where unhedged rupee exposure compounds portfolio stress.

What Happens When Global Bonds Are Left Out of the Portfolio

Portfolios concentrated entirely in domestic fixed income carry a specific set of compounding vulnerabilities that are easy to underestimate in benign periods:

- A domestic rate hike cycle simultaneously depresses bond prices and compresses future yields — with no offsetting position providing relief elsewhere in the portfolio.

- Full INR exposure leaves the portfolio vulnerable to any rupee depreciation event — a direct threat for investors with foreign-currency-denominated goals.

- When India's credit or rate environment isn't attractively priced on a risk-adjusted basis, a domestically concentrated investor has no alternative within fixed income to draw on.

- Without diversification, investors tend to compensate by holding larger cash or short-duration positions as a defensive buffer — accumulating a return drag instead of managing risk through portfolio construction.

The cumulative cost is a fixed income allocation that performs well only when domestic conditions align — and struggles precisely when diversification would matter most.

How to Get the Most Value from Global Bonds

Global bonds deliver meaningful outcomes when approached with discipline. Three conditions determine whether the allocation actually works:

Strategic Allocation, Not Tactical Trading

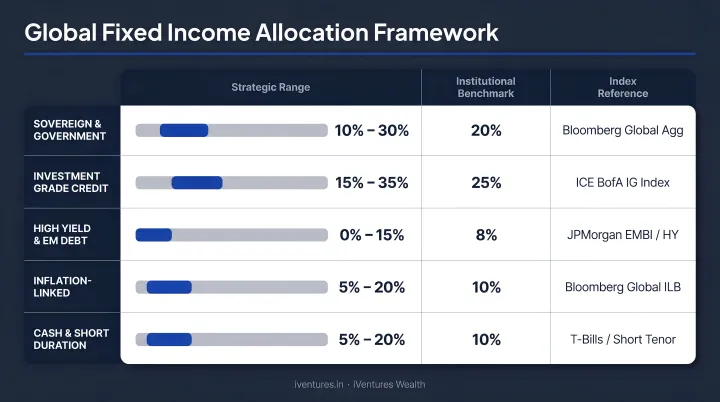

A consistent global bond allocation delivers more reliable outcomes than opportunistic position-taking. For reference, Japan's GPIF targets 25% foreign bonds (±6% deviation) in its policy portfolio, while Norway's Government Pension Fund Global allocates 30% to fixed income with a 70/30 government-corporate split within that sleeve.

These are institutional benchmarks, not prescriptions for individual investors — but they confirm that meaningful foreign fixed income allocations are standard practice at the highest levels of portfolio management.

Commonly cited ranges for a global fixed income allocation within an HNI/UHNI fixed income sleeve run from 15% to 30%, depending on risk profile, foreign liability exposure, and currency outlook.

Deliberate Hedging Decisions

Once the allocation size is set, the hedged vs. unhedged decision deserves equal attention — it should never be a default. Base it on:

- The investor's foreign currency liabilities and goals

- INR outlook and macro environment

- Risk tolerance and time horizon

- Cost of hedging relative to the yield differential

iVentures Wealth assesses each client's risk appetite and recommends unhedged, partially hedged, or fully hedged strategies based on portfolio size and outlook. For clients with USD-denominated goals, unhedged positions often provide a natural match; for investors seeking lower volatility within fixed income, hedged allocations are typically more appropriate.

Regular Review and Rebalancing

Global bond positions should be reviewed at least quarterly — rate cycles, credit spreads, and currency conditions shift, and rebalancing is warranted when macro drivers or target allocations move materially. iVentures Wealth provides ongoing global market monitoring and disciplined rebalancing for clients holding international fixed income positions.

Frequently Asked Questions

What is a global bond?

A global bond is a debt instrument issued simultaneously across multiple international markets — typically by large corporations, sovereign governments, or supranational bodies like the World Bank — and denominated in major currencies such as USD or EUR. Unlike domestic bonds, they carry regulatory and settlement frameworks designed for cross-border trading from the outset.

What is an example of a global bond?

The World Bank regularly issues global bonds across international markets. In January 2025, it issued a USD 6 billion 7-year bond with investors spanning EMEA, the Americas, and Asia. On the corporate side, Reliance Industries issued USD 4 billion in USD-denominated bonds across US and European markets in January 2022 — India's largest foreign-currency bond deal at the time.

Are global bonds a good investment?

They can add value for investors seeking to reduce correlation to domestic markets, access international yield opportunities, or hedge against INR depreciation. Suitability depends on the investor's risk profile, time horizon, foreign currency exposure, and whether a hedged or unhedged approach is appropriate.

How do global bonds differ from domestic bonds?

Domestic bonds are issued and traded within a single country in its local currency. Global bonds are issued simultaneously across multiple international markets — potentially in different currencies — giving investors access to different yield curves, credit environments, and currency dynamics that don't exist in their home market.

What are the key risks of investing in global bonds?

The primary risks are currency risk (for unhedged positions, exchange rate movements can reduce INR returns), interest rate risk in foreign markets, credit risk (particularly for emerging market bonds), and geopolitical risk. Most of these can be managed through diversification, appropriate hedging, and credit-quality screening.

Can Indian investors invest in global bonds?

Yes. Indian residents can access global bonds through the RBI's Liberalised Remittance Scheme (LRS), which permits remittances of up to USD 250,000 per person per financial year for overseas investments. Additional access routes include international mutual funds, fund-of-funds structures, and global ETFs. iVentures Wealth guides clients through the full process — LRS structuring, broker setup, tax compliance, and portfolio integration — as a SEBI-registered investment adviser (INA000019026).