Introduction

Most senior executives reach the top of their careers with significant compensation — but a surprisingly fragmented financial picture. The salary is high, the bonuses are variable, ESOPs are vesting in batches, and deferred compensation is sitting in accounts that haven't been reviewed in years. Yet few executives have a coherent plan that ties all of it together.

Getting this wrong at the executive level carries real costs:

- Paying lakhs in avoidable tax on ESOP exercises

- Holding concentrated employer equity that erodes during a bad quarter

- Discovering that corporate health insurance lapses the day you leave your job

Executive financial planning in India carries complexity that most earners never face. SEBI's Prohibition of Insider Trading (PIT) Regulations restrict when you can sell company shares. ESOP perquisite taxation can create a tax bill before you've sold a single share. And at ₹2-3 crore annual income, standard Section 80C instruments barely register.

A structured strategy addresses all of this — integrating tax planning, equity management, and compensation timing into a single, coherent plan.

Key Takeaways

- Executive financial planning requires managing compensation complexity, equity concentration, and tax efficiency simultaneously — not sequentially.

- ESOPs trigger perquisite tax at exercise and capital gains tax at sale — both must be planned proactively, not managed after the fact.

- Employer NPS contributions under Section 80CCD(2) offer deductions beyond the standard ₹1.5 lakh cap — one of the most underused tools for CXOs.

- Legacy and estate planning should start in your 40s — when equity wealth compounds fastest — not as a pre-retirement afterthought.

Why Executive Financial Planning Requires a Different Approach

Standard financial planning templates assume stable, predictable income and a portfolio spread across mutual funds and fixed deposits. Neither assumption holds for most senior executives.

Three structural differences set executive wealth apart:

- Most of an executive's net worth is tied to a single employer through ESOPs, RSUs, and deferred bonuses — creating concentration risk that a diversified mutual fund investor never faces.

- Compensation varies substantially year to year. A ₹5 crore bonus year followed by a transition year changes every planning assumption from tax optimization to liquidity management.

- Regulatory constraints mean you cannot sell company shares on demand — SEBI PIT rules can restrict trading for over 200 days in a single year.

That 200-day figure adds up fast: trading windows close from quarter-end until 48 hours after results are declared, and listed companies have up to 45 days post-quarter (60 days for annual results) to publish financials.

The practical implication: liquidity and diversification cannot be assumed. They must be engineered within compliance windows, in advance.

Deloitte's 2024 Executive Performance and Rewards Survey reported average CEO compensation in India at ₹13.8 crore — up 40% from pre-COVID levels. At that scale, every unplanned tax event or unstructured equity holding represents a material wealth erosion, not a rounding error.

Structuring Your Total Compensation: Making Every Rupee Work Harder

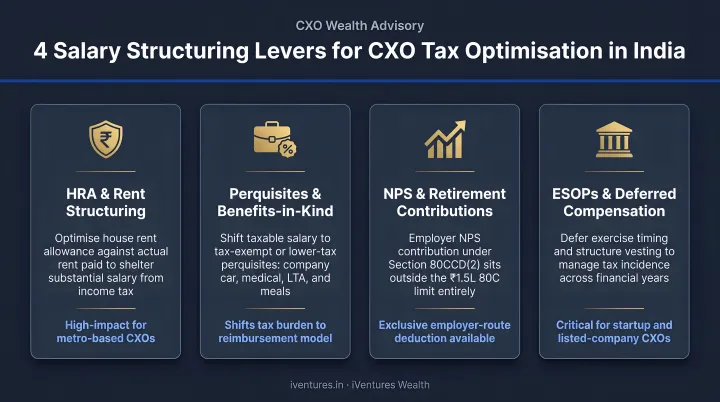

Salary and Benefits Structuring

For executives, the salary structure itself is a first-order tax planning decision. Many CXOs receive a flat CTC without reviewing whether its components are optimised — and leave significant post-tax income on the table.

Key levers worth reviewing every performance cycle:

- HRA: Exempt up to the least of actual HRA, rent paid minus 10% of salary, or 50% of salary in Delhi/Mumbai/Kolkata/Chennai (40% elsewhere) — useful under the old tax regime.

- LTA: Covers actual travel fare for up to two journeys in a four-year block; domestic travel only under Section 10(5).

- NPS employer contribution: This is the single most valuable structuring tool for CXOs. Under Section 80CCD(2), employer contributions to NPS are deductible over and above the ₹1.5 lakh Section 80C cap. Private-sector employees get a deduction of up to 10% of salary under the old regime; 14% under the new regime. This is separate from the employee's own NPS contribution and does not reduce take-home pay — it reduces CTC tax cost.

- NPS employee contribution: An additional ₹50,000 deduction under Section 80CCD(1B) is available, but only under the old tax regime. The new regime under Section 115BAC does not permit this deduction.

Deferred Compensation and Bonus Structuring

Fixed pay structuring covers only half the picture. Variable pay adds its own layer of complexity — and its own opportunities.

When a large bonus is expected in a year when other income is already high, deferring it to the following financial year can reduce the marginal tax burden meaningfully. This single decision, timed correctly, can save lakhs for a CXO in the 30% bracket.

Voluntary Provident Fund (VPF) is worth examining alongside bonus planning:

- You can contribute above the statutory 12% EPF rate into VPF — it qualifies under Section 80C within the ₹1.5 lakh limit

- For executives in the 30% bracket, it offers a tax-efficient, sovereign-backed fixed-income allocation

- Rule 9D caveat: Interest on employee PF contributions exceeding ₹2.5 lakh per year (₹5 lakh where no employer contribution exists) is taxable — so size VPF contributions carefully

Review your compensation structure at every appraisal cycle. Shifts in income level, tax regime choice, or employer financial health can all change which tools deliver the most value.

Managing ESOPs, Stock Options, and Concentrated Equity Risks

Understanding How ESOPs Are Taxed in India

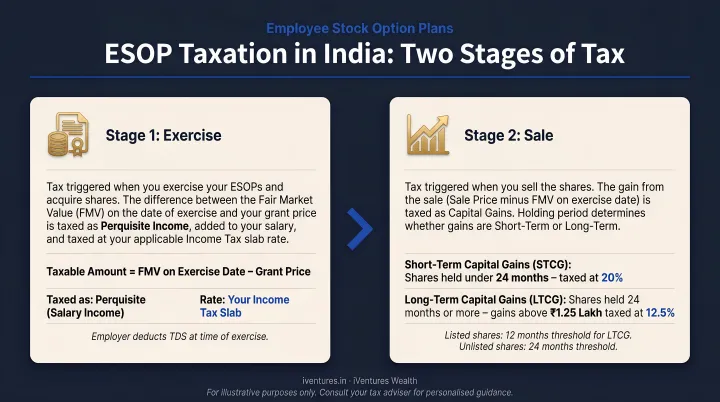

ESOP taxation in India occurs in two distinct stages, and failing to plan for both is one of the most expensive mistakes executives make.

Stage 1: At exercise — The difference between the Fair Market Value (FMV) on the exercise date and your exercise price is treated as a salary perquisite, taxed at your applicable slab rate in that financial year. This tax applies regardless of whether you've sold a single share.

Stage 2: At sale — When you sell, capital gains are computed on the difference between the sale price and the FMV used at exercise. For listed shares:

- STCG (held under 12 months): Taxed at 20% under Section 111A (for transfers on or after July 23, 2024)

- LTCG (held over 12 months): Taxed at 12.5% under Section 112A above the annual ₹1.25 lakh exemption

The timing of exercise therefore has direct tax consequences. Exercising in a financial year when other income is lower — during a sabbatical, a role transition, or early in the year before a large bonus lands — can reduce the perquisite tax meaningfully. Running the numbers before vesting, not after, is what separates a tax-efficient outcome from an avoidable liability.

Managing SEBI Insider Trading Compliance

Listed-company executives operate under SEBI PIT Regulations (last amended December 2024), which impose three practical constraints on equity sales:

- Trading windows: Closed when designated persons may possess Unpublished Price Sensitive Information (UPSI), including around financial results.

- Pre-clearance: Company codes set thresholds for trades requiring advance compliance approval.

- Blackout periods: Effectively remove daily market access for extended stretches each year.

Regulation 5 of the SEBI PIT Regulations permits structured trading plans — pre-determined plans set up during open windows that execute automatically, reducing both compliance risk and emotional decision-making around equity sales. This is broadly analogous to a 10b5-1 plan in the US context. Executives should discuss this option with their company's compliance officer and a financial adviser familiar with Indian PIT conditions.

Diversifying Away From Concentration

Once a structured sell-down plan is in place, the next question is where the proceeds go. Reinvesting into a diversified portfolio rather than holding cash or buying more equity exposure is the discipline that converts liquidity events into long-term wealth.

At the ₹10 crore+ asset level, PMS (Portfolio Management Services, minimum ₹50 lakh) and AIFs (Alternative Investment Funds) offer professional management across asset classes — equities, private credit, infrastructure, and alternatives — that standard mutual funds don't reach.

iVentures Wealth works specifically with CXO clients on ESOP sell-down frameworks and post-vesting diversification, operating as a fee-only SEBI-registered RIA without earning commissions on recommended products. When comparing PMS managers or AIF categories, commission-driven recommendations can distort the analysis — a conflict that doesn't exist in a fee-only structure.

Tax-Smart Retirement and Savings Strategies for High Earners

Maximising Tax-Advantaged Instruments

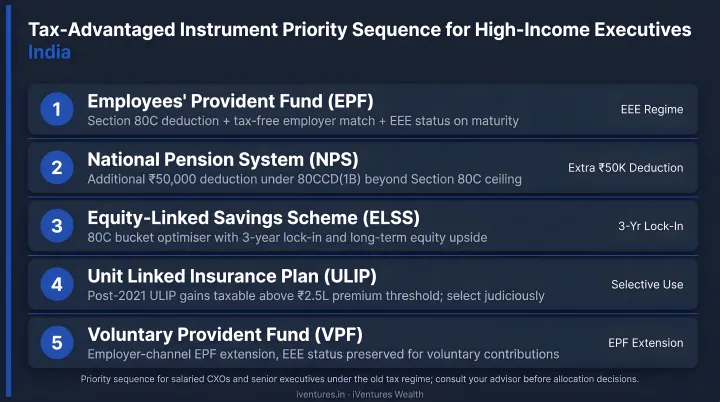

For executives already in the 30% bracket, the tax-saving instrument stack should be deployed in a specific sequence:

| Priority | Instrument | Regime | Limit |

|---|---|---|---|

| 1 | EPF + VPF (own contribution) | Old | ₹1.5 lakh under 80C |

| 2 | Employee NPS under 80CCD(1B) | Old only | Additional ₹50,000 |

| 3 | Employer NPS under 80CCD(2) | Both | 10% salary (old) / 14% salary (new) |

| 4 | ELSS within remaining 80C headroom | Old | Within ₹1.5 lakh total |

| 5 | PPF | Old | ₹1.5 lakh per year, EEE status |

PPF remains relevant despite the cap. At 7.1% per annum compounded yearly with sovereign backing and full EEE (exempt-exempt-exempt) tax treatment, it provides a guaranteed debt allocation within the retirement corpus that carries no credit risk.

Retirement Corpus Planning and Distribution

A practical starting framework: target a corpus of 25x your expected annual post-retirement expenses, adjusted for inflation and lifestyle expectations. For an executive targeting ₹20 lakh per year in today's money, the required corpus at retirement is approximately ₹5 crore — before accounting for inflation over the accumulation period.

At NPS exit, two rules govern how you access your money:

- 60% lump sum: Withdrawable tax-free under Section 10(12A)

- 40% annuity: Mandatory purchase; annuity income is taxable at your slab rate when received

Planning which assets to draw down first — and in what sequence — directly shapes the overall tax burden in retirement years.

Because the annuity component locks in taxable income, executives with a substantial mutual fund corpus often use Systematic Withdrawal Plans (SWPs) as a parallel income source. With SWPs, only the capital gains portion of each withdrawal is taxable — not the full amount — making them meaningfully more tax-efficient than FD interest or other instruments taxed at slab rates.

Going Beyond Standard Instruments

Once the standard stack is exhausted, executives have four additional avenues:

- Direct equity with tax-loss harvesting: Realising losses to offset capital gains systematically

- Debt mutual funds: Post-Finance Act 2023 (Section 50AA), units acquired from April 1, 2023 onwards are taxed at slab rates regardless of holding period — factor this into yield calculations

- REITs and InvITs: SEBI data shows 4 REITs and 24 InvITs in the Indian market as of March 2024, offering yield-generating diversification with regular distributions

- International diversification via LRS: Up to USD 250,000 per financial year under RBI's Liberalised Remittance Scheme; Budget 2025 raised the TCS threshold from ₹7 lakh to ₹10 lakh for most LRS purposes

Wealth Protection, Legacy Planning, and Estate Structuring

The Three Insurance Gaps Most Executives Have

Corporate group policies create a false sense of security. At job change or retirement, they lapse — often at exactly the point when personal financial obligations are highest.

Three coverage areas executives should address independently of employer policies, through a dedicated insurance advisor:

- Group life cover typically provides ₹1-2 crore — far short of the ₹30-40 crore a ₹2 crore earner actually needs for meaningful family protection.

- Individual health floater policies ensure continuity of coverage that doesn't disappear when employment ends.

- Personal accident and disability cover protects against loss of earning capacity — particularly relevant for executives whose income depends entirely on their ability to work.

Estate Structuring Essentials

Insurance adequacy is only one piece. For executives who've spent years accumulating wealth, the larger risk is often the absence of a structured estate plan.

Kotak Private's Top of the Pyramid Report 2024, which surveyed 150 Ultra-HNIs across 12 cities, found that 30% had not yet thought about succession planning — despite two in three calling it critical.

The four foundational tools in India:

- Registered Will: Without one, assets distribute per applicable succession laws — which may not reflect your intent. This is the non-negotiable starting point.

- Nomination updates: Nominations across demat accounts, mutual funds, and bank accounts simplify transmission — but don't override succession law or determine ownership. A Will remains essential alongside them.

- HUF (Hindu Undivided Family): Useful for income splitting on genuine family assets. One hard boundary: HUF structures cannot be used to divert executive salary income.

- Private trusts (Indian Trusts Act, 1882): Relevant for executives with significant accumulated assets or dependants needing structured, long-term financial support. Revocable and irrevocable structures serve different purposes — the right choice depends on your control, tax, and succession objectives.

iVentures Wealth's legacy planning practice addresses multi-generational wealth transfer for CXOs and UHNIs — from Will drafting coordinated with senior legal counsel to private trust establishment with documented governance rules.

Estate documents need revisiting every 2-3 years. Key triggers that make an older structure inadequate:

- ESOP vesting or liquidity events

- Property acquisitions or disposals

- Marriage, divorce, or new dependants

- Changes in tax law or succession regulations

Frequently Asked Questions

What is the 50/30/20 rule in finance?

The 50/30/20 rule allocates 50% of after-tax income to needs, 30% to wants, and 20% to savings — a reasonable starting point for general budgeting. Corporate executives with complex compensation structures typically need a customised approach: higher savings rates, tax-efficient salary structuring, and multi-instrument planning that the rule doesn't account for.

What are the steps of financial planning for corporate executives?

The key steps are: (1) assess total compensation and net worth including ESOPs and deferred pay, (2) optimise salary structure for tax efficiency, (3) plan ESOP exercise timing and manage equity concentration risk, (4) maximise tax-advantaged retirement savings in the correct sequence, (5) build a diversified portfolio beyond employer equity, and (6) establish wealth protection through insurance and estate structures.

How are ESOPs taxed in India for corporate executives?

ESOP taxation happens at two stages. At exercise, the difference between FMV and the exercise price is taxed as a salary perquisite at your applicable slab rate. At sale, the gain from FMV to sale price is taxed as capital gains — STCG at 20% for listed shares held under 12 months, or LTCG at 12.5% above ₹1.25 lakh for shares held over 12 months.

What tax-saving options are available beyond Section 80C for high-income executives?

Key options include employer NPS contributions under Section 80CCD(2), deductible beyond the ₹1.5 lakh cap (10% of salary under the old regime, 14% under the new), and health insurance premiums under Section 80D. PMS and AIFs add investment-level diversification through strategies unavailable via standard mutual funds.

How much should a corporate executive ideally save for retirement?

A common benchmark is 20-30% of gross income, but at executive income levels the corpus should be modelled individually. The 25x annual expenses rule is a useful starting point; retirement age, healthcare costs, and longevity all shift the final number enough to make a personalised projection far more reliable.

When should corporate executives start legacy and estate planning?

Mid-career — typically between 35 and 45 years — is the right window to start. ESOP vesting events, property acquisitions, marriage, and children all create new estate planning triggers that accumulate quickly. Waiting until pre-retirement often means missed structuring opportunities and compressed timelines for setting up trusts or updating nominations correctly.