Introduction

Picture this: you're sitting across from a wealth advisor for the first time. They speak confidently about market cycles, asset allocation, and long-term returns. You nod. The brochure looks professional. The office is impressive. But when you leave, you realise you never asked anything that mattered.

For founders, CXOs, and HNI families, this is more common than it should be. The cost isn't just a bad meeting : it's misaligned portfolios, hidden commissions eroding returns, and wealth transfer plans that exist on a napkin rather than a legal document.

India's wealth management industry is projected to grow from US$1.1 trillion in FY24 to US$2.3 trillion by FY29, according to Deloitte India. As more advisors enter this space, the gap between a true fiduciary and a commission-earning distributor has never been wider — and the consequences of choosing wrong have never been higher.

The 10 questions below are grouped into five themes: fiduciary standing, compensation structure, investment approach, planning depth, and communication. Together, they give you a clear framework to evaluate any advisor — whether you're walking in for the first time or stress-testing a relationship you've had for years.

Key Takeaways

- SEBI registration matters — not all advisors in India are legally bound to act in your interest

- Fee structure shapes advice quality; know whether your advisor earns commissions on what they recommend

- Investment philosophy should be research-driven and stress-tested, not reactive to market noise

- Advisory scope should extend to tax planning, estate structuring, and generational wealth transfer — not just investments

- Communication cadence and transparent reporting are non-negotiable in a long-term advisory relationship

Questions 1–3: Credentials, SEBI Registration & Fiduciary Duty

Why These Questions Come First

In India, the term "financial advisor" covers a wide spectrum — mutual fund distributors, insurance agents, stock brokers, and SEBI-registered investment advisers (RIAs) all use the title. Each operates under a different regulatory framework with different obligations to you as a client. Start here before anything else.

Question 1: "Are you a SEBI-registered investment adviser?"

SEBI RIA registration is not just a credential — it's a legal obligation. Under SEBI's Investment Advisers Regulations 2013, a registered investment adviser must act in a fiduciary capacity, disclose all conflicts of interest, and is prohibited from earning commissions on products they recommend.

Mutual fund distributors, by contrast, earn trail commissions from AMCs. They are not fiduciaries. The difference matters every time a product is recommended.

How to verify: Search the SEBI Investment Adviser database using the advisor's name or registration number. The list is live and current — do not rely on what the advisor tells you verbally.

iVentures Wealth is registered as SEBI RIA (INA000019026). The firm does not earn commissions on recommended products — compensation comes directly from clients through transparent advisory fees, with no product-shelf restrictions or conflicts of interest.

Question 2: "What are your qualifications and certifications?"

Credentials signal how your advisor was trained — and what they were trained for. Look for these specifically:

- CFA (Chartered Financial Analyst): Rigorous training in portfolio construction, asset valuation, and macro analysis — not product sales

- CFP (Certified Financial Planner): Covers financial planning across goals, tax, estate, and retirement in a structured framework

- SEBI RIA registration: Requires passing a competency assessment — not just a sales licence

Experience matters as much as the letters after a name. Institutional investing, family office advisory, and macro research are what separate a qualified advisor from a credentialed salesperson. Krishna Makhariya, Head of Research at iVentures Wealth, holds the CFA charter and applies it directly to portfolio construction and investment strategy for HNI and UHNI clients.

Question 3: "Will you have a fiduciary duty to me?"

A fiduciary must legally prioritise your financial interest above their own or their firm's. Ask for this in writing.

The contrast is real: a fiduciary adviser discloses all conflicts proactively, whereas a non-fiduciary only needs to avoid "unsuitable" recommendations — a weaker standard that still allows product incentives to shape advice.

Red flag: If an advisor deflects this question, gives a vague answer, or references "best interest" guidelines without SEBI RIA registration, treat it as a warning sign. The right answer is short, direct, and comes with documentation — not a verbal reassurance.

Questions 4–5: Fees, Compensation & Conflicts of Interest

Question 4: "How are you paid, and what are my all-in costs?"

Fee structure is one of the most consequential and most misunderstood parts of wealth advisory in India. Many investors assume advisory is free, when the advisor is actually earning trail commissions from AMCs or insurance companies on every product placed.

The three primary models:

| Model | How the Advisor Is Paid | Conflict Level |

|---|---|---|

| Fee-only | Client pays directly (AUM %, flat fee, or retainer) | Lowest |

| Commission-based | Earns from product manufacturers | Highest |

| Fee-based | Combination of client fees + some commissions | Medium |

Fee-only advisors have the fewest conflicts. Ask for a written fee disclosure before engagement — not after.

That written disclosure matters more than most investors realise. SEBI's 2020 amendment to the Investment Advisers Regulations created stricter segregation between advisory and distribution activity — SEBI-registered RIAs cannot earn commissions while simultaneously charging advisory fees. If your advisor operates under both modes, ask exactly how those activities are separated.

iVentures Wealth operates on a fee-only model. Fee structures vary by client segment (AUM-based, fixed retainer, or mandate-based) and the full schedule is disclosed in writing before any investment is executed.

Question 5: "Do others stand to gain from the financial advice you give me?"

An advisor affiliated with an AMC, insurance company, or brokerage may have incentives to recommend specific products — even if those products are not optimal for your situation.

A clean, trustworthy answer looks like this:

- The advisor proactively shares their complete fee schedule

- Confirms they earn no commissions on recommended products

- Provides a written engagement letter before the relationship begins

- Uses direct plans for mutual fund recommendations (zero trail commission to advisor)

If those boxes aren't checked, treat the gaps as signals. Watch for:

- Vague verbal commitments instead of written disclosures

- References to "platform fees" without clear dollar amounts

- "We only charge when you make money" framing — performance fees are not the same as conflict-free advice

None of these are substitutes for fiduciary transparency.

Questions 6–7: Investment Philosophy & Risk Strategy

Question 6: "What is your investment philosophy, and how does it change when markets decline?"

Two advisors can both hold SEBI registration and clean fee structures — and still have completely different approaches when markets turn volatile. Philosophical alignment determines whether you get a call during a correction or silence until the next quarterly review.

A credible advisor should articulate:

- A consistent, research-driven framework — not a strategy that shifts with market sentiment

- Specific tactics for downturns: rebalancing, tax-loss harvesting, maintaining asset allocation

- A concrete example of what they did during a real volatility event

iVentures Wealth's philosophy is anchored in disciplined allocation and long-term compounding — not market timing. During the 2020 COVID crash, the Nifty 50 fell approximately 40% before recovering to new highs within four months. Panic-driven exits during that window locked in permanent losses; disciplined investors who held or added captured the full recovery.

The cost of poor timing compounds quietly. iVentures' internal data indicates the behaviour gap cost Indian investors an estimated 5.3% annually from 2003 to 2022 — the difference between what a fund returned and what the average investor actually earned.

Vague answers like "we invest for the long term" are insufficient. The same standard applies to risk profiling — which is where Question 7 comes in.

Question 7: "How do you personalise portfolios for my specific goals and risk profile?"

Standard risk questionnaires — conservative, moderate, aggressive — are not risk profiling. For HNIs and UHNIs, meaningful profiling should account for:

- Liquidity needs and investment horizon

- Income sources (salary, business dividends, rental income)

- Family obligations and dependent structures

- Psychological risk tolerance vs. financial capacity for loss

- Illiquid asset exposure: business holdings, real estate, ESOPs, private equity

For family office mandates, the investable portfolio strategy should be built with full awareness of what sits outside it. A founder with ₹80 Cr concentrated in their own company's stock is not starting from a neutral position — and their advisor should treat that concentration risk as the first problem to address.

Ask also how the advisor benchmarks performance — which index, over what rolling period, and how they communicate when the portfolio trails that benchmark. A research-led advisor answers this without hesitation. One focused primarily on product distribution typically cannot.

Questions 8–9: Tax Optimisation, Estate Planning & Wealth Scope

Question 8: "How will you help me optimise my tax liability?"

Tax planning is not a year-end add-on. For HNIs and UHNIs, LTCG, STCG, dividend taxation, and surcharge implications on high incomes all directly affect net returns. For NRI clients, TDS and DTAA provisions add additional complexity that requires proactive structuring, not reactive filing.

Ask whether the advisor:

- Integrates tax planning into portfolio construction (not just tracks it after the fact)

- Identifies tax-harvesting opportunities proactively

- Coordinates with a CA or tax professional — or simply refers you elsewhere and moves on

- Structures withdrawal sequencing to minimise tax drag across financial years

iVentures Wealth incorporates tax optimisation across portfolio strategy — including capital gains computation, DTAA structuring for NRI clients, and coordination with chartered accountants for ITR filing. For passive income strategies, the firm calibrates SWP withdrawal lots to LTCG-efficient thresholds. The result: clients avoid tax drag that typically erodes 1–2% of net returns annually through uncoordinated planning.

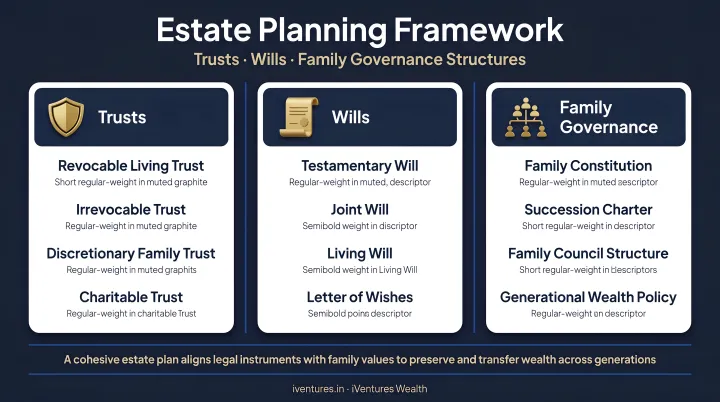

Question 9: "Do your services extend to estate and legacy planning?"

According to EY India, only 59% of surveyed Indian families have wills or family agreements in place. 11% have only verbal succession arrangements, and 11% have not discussed succession at all — despite an estimated US$1.5 trillion intergenerational wealth transfer expected over the next decade.

For HNIs and family offices, wealth transfer planning is a governance issue, requiring the same rigour applied to portfolio construction. Probe specifically whether they can:

- Help structure private family trusts, discretionary or revocable

- Draft or coordinate wills with experienced estate planning attorneys

- Set up family constitutions and governance frameworks for business-owning families

- Work across multiple entities — individuals, HUFs, trusts, NRI accounts, LLPs

iVentures Wealth provides full-scope estate planning coordination — from trust structuring to succession governance, working alongside legal experts including senior counsel experienced in trusts, cross-border inheritance structures, and succession planning. Within family office mandates, this is a structured deliverable with defined milestones — not an ad hoc referral made when a client raises the question.

Question 10: Communication, Reporting & Long-Term Partnership

Question 10: "How often will we meet, and how will you communicate my portfolio's progress?"

For busy founders, CXOs, and UHNI families, communication frequency is only part of the answer. What matters more is whether your advisor reaches out proactively when market conditions shift — not just at the next scheduled review.

What good reporting looks like:

- Consolidated views across all accounts, entities, and asset classes in one place

- Monthly statements and quarterly performance reports with XIRR, absolute returns, and benchmark comparison

- Proactive outreach during significant market events or regulatory changes — not just in the next scheduled review

- A digital platform that gives real-time visibility between formal meetings

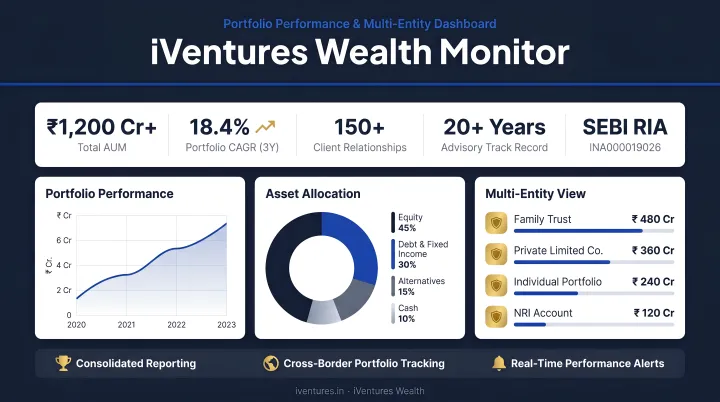

iVentures Wealth conducts portfolio reviews at least quarterly, with continuous real-time monitoring via the Wealth Monitor App. Clients can toggle between individual, family, and HUF portfolios, view performance attribution by fund and category, and access reports — all secured with bank-grade encryption.

For UHNI families, role-based dashboard access means trustees, next-generation members, and advisors each see only what is relevant to their role.

All investment decisions are communicated in advance via email, app notification, or recorded call — with written confirmation or digital acceptance before execution. For clients managing complex, multi-entity wealth, this paper trail is not a formality — it is accountability built into every transaction.

How to Prepare Before Your First Advisor Meeting

You do not need to arrive with tax returns, exact account balances, or a detailed financial audit. What matters is clarity of intent.

Before the meeting, prepare:

- A high-level picture of your investable portfolio, existing insurance policies, business interests, and real estate holdings

- Outstanding liabilities — loans, guarantees, contingent obligations

- Your most pressing financial goals: liquidity in three years, retirement at 55, business exit planning, NRI cross-border tax exposure

Once you have your preparation in order, think carefully about how you use the meeting itself:

- Select 3–4 priority questions from the 10 above and send them in advance — this forces the advisor to prepare substantive answers rather than generic responses

- Evaluate the advisor on two dimensions: technical competence (credentials, fee structure, investment philosophy) and interpersonal trust (do they listen, ask questions about your life, and speak without jargon?)

A relationship designed to last decades needs both. An advisor who is technically sharp but impossible to communicate with will produce strategies you never fully understand — and therefore never fully commit to. The meeting itself is the first test of that balance.

Frequently Asked Questions

What are the best questions to ask a financial advisor?

The five most important questions cover fiduciary status, fee structure, credentials, investment philosophy, and the scope of planning services. Priority shifts with context — a new advisor evaluation calls for more scrutiny on registration and compensation, while reviewing an existing relationship warrants sharper questions about performance attribution and planning breadth.

How do I prepare for a conversation with a financial advisor?

Get a rough picture of your financial situation — investable assets, liabilities, income sources — and clarify your top two or three goals before the meeting. Prepare 3–4 specific questions in advance so the conversation has direction rather than defaulting to a generic pitch.

What does it mean for a financial advisor to be SEBI registered?

SEBI RIA registration legally obliges the advisor to act as a fiduciary — placing your interest above their own — and prohibits them from earning commissions on products recommended while charging advisory fees. This is a different standard entirely from mutual fund distributors or insurance agents, who earn from product sales.

What is the difference between a fee-only and a commission-based financial advisor?

Fee-only advisors are compensated solely through client fees — an AUM percentage, flat fee, or retainer — with no product commissions. Commission-based advisors earn from the products they place, which creates an inherent conflict of interest. Fee-only is the cleaner model; get the compensation structure confirmed in writing before engaging.

How often should I meet with my financial advisor?

Quarterly reviews are the baseline for HNIs and UHNIs. More frequent check-ins make sense during significant market events, tax planning season, or major life changes — a business exit, inheritance, or shift in residency status are common triggers.

What documents should I bring to my first meeting with a financial advisor?

A high-level summary of current assets, liabilities, and income sources is sufficient for a first meeting. Skip the paperwork deep-dive — focus instead on two or three specific concerns you want resolved so the conversation is productive from the start.