The rules aren't straightforward either. Finance Act 2025 restructured the new tax regime slabs for AY 2026-27, Budget 2024 changed capital gains rates, and a provision introduced back in 2020 means some UAE-based NRIs may not be as "non-resident" as they assume. Non-compliance carries interest under Sections 234B and 234C, plus potential penalties.

This guide covers everything NRIs need to know: how residency status is determined under the Income Tax Act, which income types trigger Indian tax, the updated slab rates for FY 2025-26, deductions available (and which ones are blocked), and the key filing steps.

Key Takeaways

- NRIs are taxed only on income earned or received in India, not on global income

- Residency under the Income Tax Act (not FEMA) must be re-evaluated every financial year

- The new tax regime is the default for FY 2025-26 — switching to the old regime requires an active choice at filing

- NRIs are not eligible for the Section 87A rebate under either regime

- NRE and FCNR interest is tax-free; NRO interest is fully taxable with TDS at 30%

How NRI Residency Status Is Determined for Tax Purposes

The Income Tax Act vs. FEMA — Two Different Tests

Residency for tax purposes is governed by the Income Tax Act, 1961 — not FEMA. A person can be an NRI under FEMA (for banking and remittance purposes) but qualify as a tax resident under the IT Act. That distinction changes their entire tax exposure. Re-evaluate this status every April; a longer-than-planned India visit can shift the result.

Section 6 of the Income Tax Act defines the rules:

Standard Resident Tests:

- Present in India for 182 or more days in the financial year, OR

- Present for 60+ days in the current year and 365+ days in the preceding 4 years

For Indian citizens leaving India for employment (or ship crew members), the 60-day threshold is replaced by 182 days — a carve-out that protects genuine emigrants.

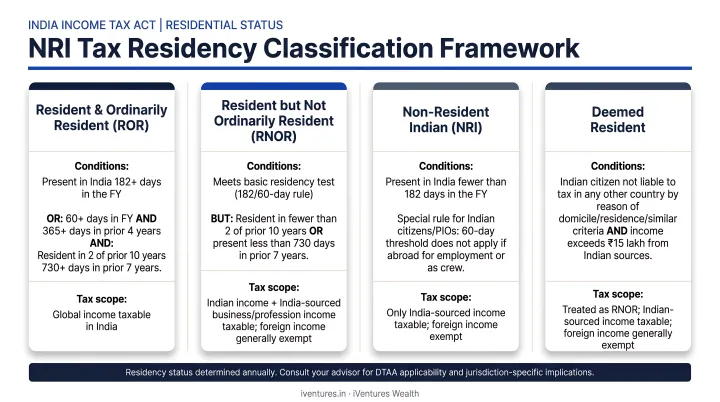

The 120-Day Rule and RNOR Status

Finance Act 2020 added a sharper rule for high-income visitors. An Indian citizen or PIO whose Indian-sourced income exceeds ₹15 lakh and who stays between 120 and 182 days is classified as Resident but Not Ordinarily Resident (RNOR).

RNOR status is a middle ground, not full resident taxation. The tax scope is more limited than a standard resident:

- Taxable: Indian income, plus foreign income from a business controlled or profession set up in India

- Not taxable: Foreign salary earned from a foreign employer — this stays outside India's tax net

The "Deemed Resident" Trap for UAE-Based NRIs

RNOR is not the only residency risk for frequent visitors. Section 6(1A) targets a different group entirely: an Indian citizen whose Indian income exceeds ₹15 lakh and who is not liable to tax in any other country is deemed a resident, even without setting foot in India.

This provision is routinely missed by NRIs in zero-tax jurisdictions like the UAE. Being based in Dubai does not automatically create tax liability there. If you pay no tax in your country of residence and your Indian income crosses ₹15 lakh, India can treat you as a deemed resident. A formal residency analysis — not a country-label assumption — is the only way to confirm your position.

The Decision Framework:

| Classification | Condition | Tax Scope |

|---|---|---|

| Resident & Ordinarily Resident | Meets basic resident tests + long-stay history | Global income |

| RNOR | 120–182 days + ₹15L+ Indian income, or non-resident in 9 of last 10 years | Indian income + India-connected foreign income |

| Deemed Resident | ₹15L+ Indian income + no tax liability abroad | Indian income only |

| NRI | None of the above | Indian income only |

What Income Is Taxable for NRIs in India?

The anchor provision is Section 5(2): India taxes non-residents on income received or deemed received in India, and income accruing, arising, or deemed to accrue/arise in India.

| Taxable in India | Not Taxable in India |

|---|---|

| Rental income from Indian property | Salary for services rendered entirely abroad |

| NRO account interest | NRE / FCNR account interest |

| Dividends from Indian companies | Income earned and received outside India |

| Capital gains on Indian assets | Foreign business income (no India connection) |

| Salary for services rendered in India | Overseas rental income |

Salary and Business Income

Salary is taxable in India when services are rendered here — regardless of where payment lands. An NRI working remotely for an Indian company with salary deposited into an NRO account pays Indian tax at applicable slab rates.

Business profits are taxable when the enterprise meets either of these conditions:

- Set up in India (registered or incorporated here)

- Controlled or managed from India (key decisions made by Indian-based principals)

Rental Income and TDS by Tenants

Rental income from Indian property is taxed at slab rates. For computing the taxable amount, 30% of the annual value is allowed as a standard deduction under Section 24(a), and municipal taxes paid reduce the annual value first.

One obligation that surprises many tenants: when paying rent to an NRI landlord, tenants must deduct TDS at 30% plus applicable surcharge and 4% cess under Section 195 before remitting payment. For income below the surcharge threshold, the effective rate works out to 31.2%.

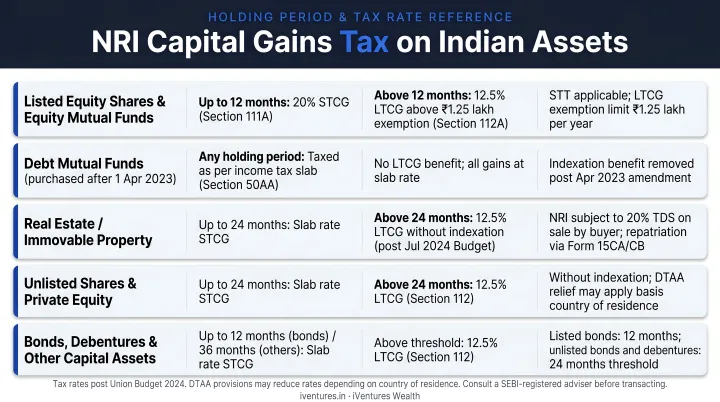

Capital Gains on Indian Assets

Rates changed with Budget 2024. Current rules for AY 2026-27:

| Asset Type | Holding Period | Tax Rate |

|---|---|---|

| Listed equity / equity funds (STT-paid) — STCG | Under 12 months | 20% (Section 111A) |

| Listed equity / equity funds — LTCG | 12+ months | 12.5% above ₹1.25 lakh (Section 112A) |

| Immovable property — LTCG | 24+ months | 12.5% (Section 112) |

Property buyers purchasing from an NRI must deduct TDS at the applicable capital gains rate under Section 195. When the actual gain is lower than the gross sale price implies, NRIs can apply for a lower-deduction certificate to avoid excess withholding.

NRO, NRE, and FCNR Account Taxation

- NRO accounts: Interest is fully taxable; TDS applies at 30% plus surcharge and cess

- NRE accounts: Interest is exempt under Section 10(4)(ii)

- FCNR deposits: Interest is exempt, subject to the deposit satisfying statutory conditions

Account type directly determines your tax exposure on interest income. NRIs cannot maintain regular resident savings accounts. Existing savings accounts must be converted to NRO accounts, and that conversion has immediate tax consequences: NRO interest becomes fully taxable from the date of conversion.

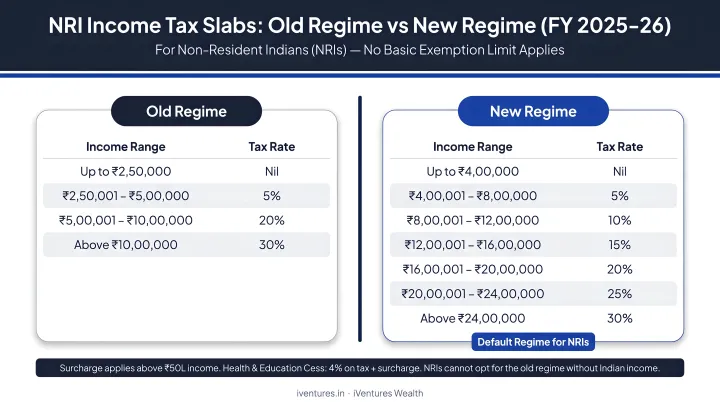

NRI Income Tax Slabs & Rates for FY 2025-26 (AY 2026-27)

Both regimes are open to NRIs. The new regime under Section 115BAC is the default; opting for the old regime requires an explicit election in the ITR. Unlike residents, NRIs receive no age-based concessions — a 70-year-old NRI and a 30-year-old NRI face identical slabs.

Slab Comparison: Old vs. New Regime

| Income Range | Old Regime | New Regime (115BAC) |

|---|---|---|

| Up to ₹2.5 lakh | Nil | — |

| Up to ₹4 lakh | — | Nil |

| ₹2.5L – ₹5L | 5% | — |

| ₹4L – ₹8L | — | 5% |

| ₹5L – ₹10L | 20% | — |

| ₹8L – ₹12L | — | 10% |

| ₹10L+ | 30% | — |

| ₹12L – ₹16L | — | 15% |

| ₹16L – ₹20L | — | 20% |

| ₹20L – ₹24L | — | 25% |

| Above ₹24L | — | 30% |

These new regime slabs reflect the Finance Bill 2025 as passed for AY 2026-27.

Surcharge, Cess, and the 87A Gap

Three components stack on top of your base tax liability:

- Surcharge: 10% (₹50L–₹1Cr), 15% (₹1Cr–₹2Cr), 25% (₹2Cr–₹5Cr), 37% above ₹5Cr under the old regime. The new regime caps surcharge at 25%. Surcharge on Section 111A and 112A capital gains is capped at 15% under both regimes.

- Health & Education Cess: 4% on (income tax + surcharge) under both regimes.

- Section 87A rebate: NRIs are not eligible. The rebate — up to ₹12,500 under the old regime or ₹60,000 under the new regime — applies only to resident individuals, as confirmed by the Income Tax Department. This is one of the most commonly misapplied provisions in NRI tax calculations.

Special Flat Rates for Specific NRI Income

| Income Type | Applicable Rate |

|---|---|

| Dividends from Indian companies | 20% |

| Royalties / Fees for Technical Services | 20% |

| STCG on listed equity (Section 111A) | 20% |

| LTCG on foreign exchange assets (Section 115E) | 12.5% |

| Investment income under Chapter XII-A | 20% |

These rates apply before surcharge and cess and do not follow the standard slab structure. Where a DTAA applies, treaty rates may override these defaults — making the applicable rate dependent on the NRI's country of residence and the specific income category.

Deductions Available to NRIs (And What's Off the Table)

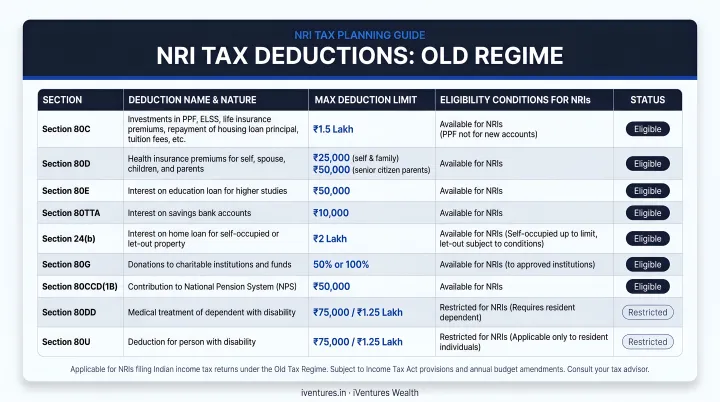

What NRIs Can Claim Under the Old Regime

| Section | Deduction | Limit |

|---|---|---|

| 80C | Life insurance premiums, ELSS, ULIP, home loan principal, tuition fees | ₹1.5 lakh |

| 80D | Health insurance — self/spouse/children | ₹25,000 (₹50,000 if senior citizen) |

| 80E | Education loan interest | Unlimited, up to 8 years |

| 80G | Eligible donations | Varies |

| 80TTA | NRO savings account interest | ₹10,000 |

| Section 24(b) | Interest on home loan (let-out property) | Actual interest paid |

None of these apply under the new tax regime, except Section 24(b) for let-out property interest.

What NRIs Cannot Claim

Several deductions are either scheme-ineligible or restricted to resident individuals:

- PPF contributions — NRIs cannot open new PPF accounts; existing accounts can continue but no fresh 80C claim on new contributions

- NSC, SCSS, Post Office 5-year deposits — not available to NRIs under scheme rules

- Sections 80DD, 80DDB, 80U — disability and specified disease deductions are resident-linked

Filing errors on these specific items are common. Getting them wrong doesn't just cost tax — it can trigger scrutiny on the entire return.

Choosing Between Regimes

NRIs with substantial 80C and 80D deductions may find the old regime more efficient. Those without significant deductions typically benefit from the new regime's broader slab structure and lower rates at middle-income levels. The optimal answer depends on the specific income mix.

For NRIs and OCIs with investable assets of ₹5 Crores or more, iVentures Wealth's NRI/OCI Wealth Management service covers exactly this — regime modeling alongside investment structuring, so the chosen regime and the portfolio are aligned from the start. The SEBI-registered advisory team (INA000019026) coordinates with tax professionals in the UAE, US, UK, Singapore, Canada, and Australia, ensuring India-side and overseas-side implications are both covered before filing or investing.

DTAA Benefits, TDS Rules, and ITR Filing for NRIs

DTAA: Relief from Double Taxation

India has signed Double Taxation Avoidance Agreements with over 90 countries. When the same income is taxed in both India and the NRI's country of residence, relief is available through two methods:

- Exemption method: Income is taxed in only one country

- Tax credit method: Tax paid in India is credited against foreign tax liability

DTAA benefits are not automatic. To claim them, NRIs must provide a Tax Residency Certificate (TRC) from their country of residence and, where required, submit Form 10F to the deductor.

Treaty provisions vary significantly by country. Under the India-UAE DTAA, gains on immovable property in India are typically taxable where the property is located. Under the India-US DTAA, dividend and interest income may qualify for reduced treaty rates, though only after proper documentation is in place.

ITR Filing: Which Form, When, and Whether at All

NRIs cannot use ITR-1 or ITR-4. The applicable forms are:

- ITR-2: Salary, house property, capital gains, foreign assets

- ITR-3: Business or professional income

Filing is mandatory if gross Indian income exceeds the basic exemption — ₹2.5 lakh under the old regime, ₹4 lakh under the new regime.

Even below these thresholds, filing is advisable to claim TDS refunds — particularly for NRO interest, where 30% is withheld upfront.

Exception under Section 115G: If an NRI's only Indian income consists of investment income or LTCG from specified foreign exchange assets (as defined under Section 115C) and TDS has been fully deducted, filing an ITR is not mandatory.

Due date: 31 July 2026 for FY 2025-26 (AY 2026-27), subject to any CBDT extension.

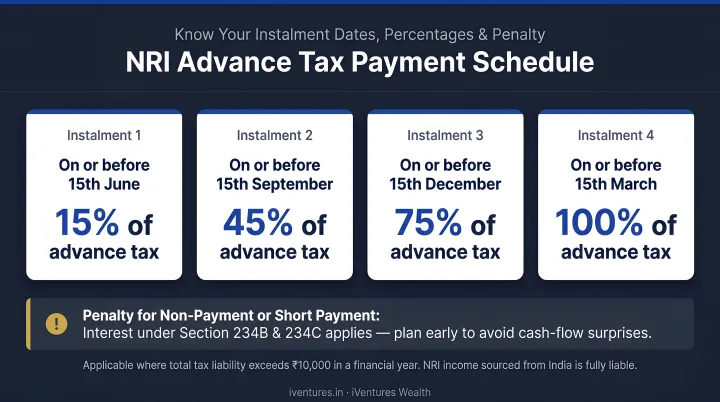

Advance Tax and Documentation

Alongside filing, NRIs must stay current on advance tax. If total tax liability exceeds ₹10,000 after TDS, advance tax is due in four instalments: 15 June (15%), 15 September (45%), 15 December (75%), and 15 March (100%). Shortfalls attract interest at 1% per month under Sections 234B and 234C.

Keep these documents on hand for a clean ITR filing:

Documents to maintain for clean ITR filing:

- Passport with travel dates

- PAN card

- Form 26AS and AIS

- Form 16A from deductors

- NRO/NRE/FCNR account statements

- Capital gains computation records

- TRC and Form 10F (if claiming DTAA benefits)

Frequently Asked Questions

How much tax does an NRI pay in India?

NRIs pay tax only on Indian-source income at slab rates ranging from 0% to 30%, plus applicable surcharge and 4% cess. Under the default new regime for FY 2025-26, income up to ₹4 lakh is exempt and the 30% rate applies above ₹24 lakh. TDS is often deducted upfront, with the ITR reconciling the final liability.

What is the 90% rule for non-residents?

Under Section 115G, if an NRI's only Indian income is "special investment income" from Section 115C assets (interest/dividends from shares, debentures, or government securities acquired in foreign currency) and TDS has already been deducted on it, filing an ITR is not required. The "90% rule" refers to this complete-TDS-coverage condition.

Are NRIs eligible for the Section 87A rebate?

No. The Section 87A rebate — up to ₹12,500 under the old regime or ₹60,000 under the new regime — is available only to resident individuals. NRIs are explicitly excluded under both regimes.

Is interest earned on an NRE account taxable for NRIs?

Interest on NRE and FCNR accounts is completely exempt from Indian income tax under Section 10(4)(ii). However, interest on NRO accounts is fully taxable and subject to TDS at 30% plus applicable surcharge and cess.

Can NRIs claim deductions under Section 80C?

Yes, under the old tax regime, NRIs can claim Section 80C deductions up to ₹1.5 lakh — covering life insurance premiums, ELSS, ULIP, and home loan principal repayment, but not PPF, NSC, SCSS, or post office deposits. No 80C deductions apply under the new regime.

What is the ITR filing deadline for NRIs for FY 2025-26?

The due date is 31 July 2026, subject to extension by the Income Tax Department. NRIs below the basic exemption limit aren't required to file, but filing is advisable to claim TDS refunds on NRO interest, rental income, or capital gains.