Introduction

You earn a steady income. Your salary hits your account every month. Yet somehow, by the 25th, you're wondering where it all went.

This isn't unusual. According to the NCFE Financial Literacy and Inclusion Survey, only 27% of Indian adults are financially literate — meaning most people managing money daily have never been taught a structured system for doing so. A 2023 Moneycontrol survey of 1,364 salaried employees found that 57% saved less than 20% of their take-home pay, and 23% had no financial buffer for emergencies.

The problem isn't income. It's the absence of a clear framework.

That framework is what this guide builds. It covers the four pillars of personal finance, two proven budgeting approaches, how to build an emergency fund, and the real difference between saving and investing — grounded in examples that reflect how Indian earners actually manage money.

Key Takeaways

- Personal finance rests on four pillars: earning, budgeting, saving, and investing — each supports the others.

- Use the 50/30/20 or 70/20/10 rule to eliminate guesswork from money allocation.

- Maintain a 3–6 month emergency fund — adequate liquidity is the foundation before any investment commitment.

- Savings preserve liquidity; investments build wealth — you need both.

- When financial complexity grows, a SEBI-registered investment adviser provides structured, conflict-free guidance.

What Personal Finance Really Means

Personal finance is the practice of managing your income, expenses, savings, debt, and investments to achieve specific life goals. It's not a one-time plan you set and forget — it's a dynamic system that evolves as your income, responsibilities, and goals change.

Two common misconceptions hold people back:

- Anyone who wants their money to work harder needs a system — not just those in financial difficulty.

- Higher income without a plan just produces higher expenses. The habits come first; the wealth follows.

Financial literacy is the foundation. You don't need to be an expert, but you need to understand the basics before any wealth-building strategy can stick.

The Four Pillars of Personal Finance

Pillar 1 — Earning

Income is where everything starts — but how much you take home matters more than your gross CTC. After EPF contributions, professional tax, and TDS deductions, your actual net take-home is often 20–30% lower than your CTC headline figure.

Two things worth building here:

- Understand your real take-home pay before you build any budget or savings target

- Reduce single-income risk — a second income stream, freelance work, or skill development that supports career growth provides a buffer that salary alone cannot

Pillar 2 — Budgeting

A budget gives every rupee a job. Without one, even ₹1,50,000 monthly earners find themselves short by month-end — not because they overspend dramatically, but because of dozens of small untracked decisions.

Budgeting reveals leakage. Subscriptions, impulsive online purchases, and eating out quietly drain thousands each month — amounts that only become visible once you start tracking them.

Pillar 3 — Saving

Saving is not "whatever's left over." Intentional saving means transferring a fixed percentage before you pay other expenses — the pay-yourself-first model.

Short-term savings goals: Emergency fund, travel, down payment

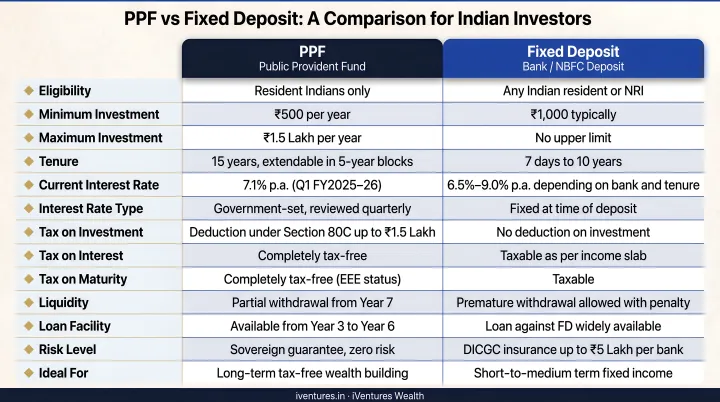

Long-term savings instruments in India:

| Instrument | Rate | Lock-in | Tax Treatment |

|---|---|---|---|

| PPF | 7.1% p.a. | 15 years | EEE (fully exempt) |

| SBI FD (1–2 years) | 6.25% p.a. | Flexible | Taxable interest |

| HDFC FD (18 months–3 years) | 6.45% p.a. | Flexible | Taxable interest |

PPF is particularly useful for long-term, tax-exempt compounding — but its 15-year lock-in makes it unsuitable as an emergency fund.

Pillar 4 — Investing

Investing is how savings grow over time. Compounding returns — earned on both your principal and prior gains — is what turns disciplined saving into meaningful, lasting wealth.

Investing involves risk — that's the trade-off for higher returns. The goal is to match your investment type to your time horizon and risk appetite. A ₹10,000 monthly SIP at 12% annualised returns grows to over ₹1 crore in 20 years — an outcome no savings account can replicate.

Protection — The Cross-Pillar Principle

No financial plan survives a serious health crisis without insurance. A 2021 NITI Aayog report found that at least 30% of India's population — roughly 40 crore people — lacks financial protection for healthcare costs. A 2023 study found that nearly 60% of Indian households had no member covered by health insurance.

Adequate health and term life insurance protects all four pillars simultaneously. One major uninsured medical event can:

- Wipe out years of accumulated savings

- Force premature liquidation of long-term investments

- Derail financial goals that took a decade to build

Budgeting Frameworks That Actually Work

Budgeting rules are heuristics — simple frameworks that remove the daily decision fatigue of "how much should I spend on this?" No rule fits everyone perfectly, but having any framework is better than having none.

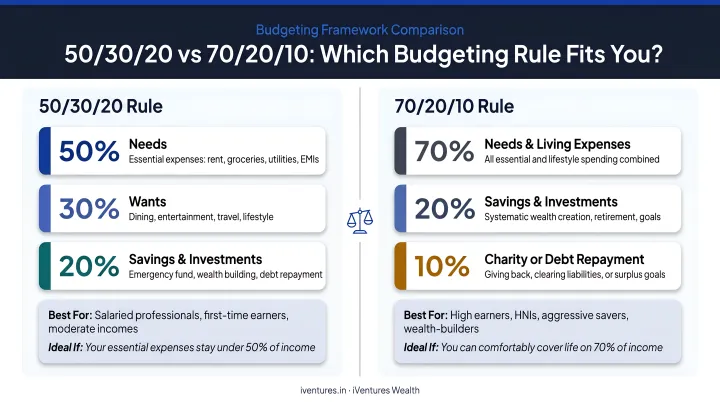

The 50/30/20 Rule

Popularised by Elizabeth Warren and Amelia Warren Tyagi, this rule splits your take-home income into three buckets:

- 50% → Needs: Rent, groceries, EMIs, utilities, insurance premiums

- 30% → Wants: Dining out, entertainment, travel, subscriptions

- 20% → Savings and investments: Emergency fund, SIPs, PPF

Practical example with ₹1,00,000 monthly take-home:

| Category | Allocation | Monthly Amount |

|---|---|---|

| Needs | 50% | ₹50,000 |

| Wants | 30% | ₹30,000 |

| Savings/Investments | 20% | ₹20,000 |

Works best for: Earners with moderate EMI loads and mid-to-high incomes where 30% on wants is actually achievable.

The 70/20/10 Rule

This framework is more practical for those with existing loan obligations:

- 70% → Living expenses: Both needs and moderate wants combined

- 20% → Savings and investments: Fixed savings, SIPs, long-term wealth

- 10% → Debt repayment or giving: Prepaying loans faster or charitable contributions

With the same ₹1,00,000 income, this gives you ₹70,000 for combined living costs, ₹20,000 toward wealth-building, and ₹10,000 for accelerated debt paydown.

Zero-Based Budgeting

For detail-oriented individuals who want tighter control: every rupee of income is assigned a specific purpose so that income minus all allocations equals zero. It's more effort to maintain but works well for those who have struggled with the broader percentage rules.

Choosing the Right Framework

Each of the three approaches above suits a different financial situation. Pick based on:

- Monthly income level and how much flexibility you genuinely have

- Existing EMI burden as a percentage of take-home

- Number of financial dependants

- Proximity to major goals (e.g., buying a home in 2 years requires aggressive savings)

A framework you follow imperfectly for years will outperform a theoretically optimal one you abandon in three months.

Building Your Financial Safety Net

Emergency Funds — First Priority, Always

An emergency fund is not an optional extra. It's the single most important financial step before you begin investing.

Without one, any crisis (job loss, medical emergency, urgent repair) forces you to liquidate investments at the wrong time. Markets don't care about your timing; you'll sell when prices are down and miss the recovery.

Sizing your emergency fund:

- General benchmark: 3–6 months of total monthly expenses (not income); 6–12 months for those with variable compensation, business income, or equity-linked pay

- Larger fund needed if: Self-employed, irregular income, single-income household, or significant EMI obligations

Where to park it:

- Savings accounts or sweep-in FDs for instant access

- Liquid mutual funds for slightly better returns with T+1 withdrawal

Do not put your emergency fund in PPF, FDs with lock-ins, or equity — liquidity is the point.

Good Debt vs. Bad Debt

Not all debt is equal. The distinction matters enormously for your financial plan.

Productive debt (can build net worth or earning potential):

- Home loan — builds an asset, interest partially tax-deductible

- Education loan — increases future earning capacity

Consumer debt (erodes wealth):

- Credit card revolving debt: SBI Card and ICICI Bank both charge up to 45% p.a. on outstanding balances. No investment in India reliably beats that cost, which makes repayment the highest-return move available.

- Personal loans for consumption: 10–16.5% p.a. at major banks, still high relative to expected investment returns

Does the interest cost exceed the likely return on an alternative use of those funds? If yes, paying off the debt first is the better financial decision.

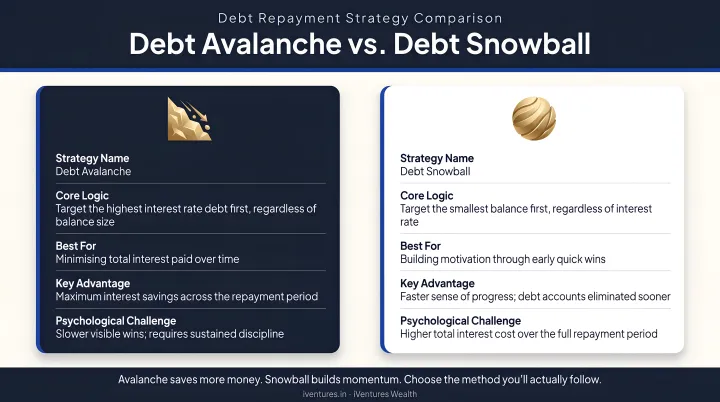

Two Debt Repayment Strategies

Avalanche method — pay off the highest-interest debt first while making minimum payments on others. Mathematically optimal; saves the most money over time. Best for analytical personalities comfortable with delayed gratification.

Snowball method — pay off the smallest balance first regardless of interest rate. Builds psychological momentum through quick wins. Better for those who need visible progress to stay motivated.

Both methods work — the difference is behavioral, not mathematical. For high earners juggling multiple debt obligations, the avalanche method typically saves more in absolute rupee terms; the snowball method wins if motivation is the real bottleneck.

Saving vs. Investing: Why You Need Both

The Core Distinction

- Saving = capital preservation and liquidity, for money you may need within 0–3 years

- Investing = capital growth over 3+ years, accepting some volatility for higher long-term returns

They're not interchangeable. Putting all your money in savings is as problematic as putting all of it in equity.

The Cost of Staying in Savings Only

SBI and ICICI savings accounts currently offer 2.50% p.a. However, World Bank data shows India's average CPI inflation ran at 4.99% per year between 2015 and 2024.

To put that gap in concrete terms: ₹1 lakh in a savings account at 2.50% p.a. grows to approximately ₹1,28,000 in nominal terms after 10 years. In real purchasing power (adjusted for ~5% inflation), it's worth roughly ₹78,600. You've technically gained money while actually losing purchasing power.

Investing, even at moderate risk levels, is therefore not optional for long-term wealth building. It's the difference between staying ahead of inflation and quietly falling behind it.

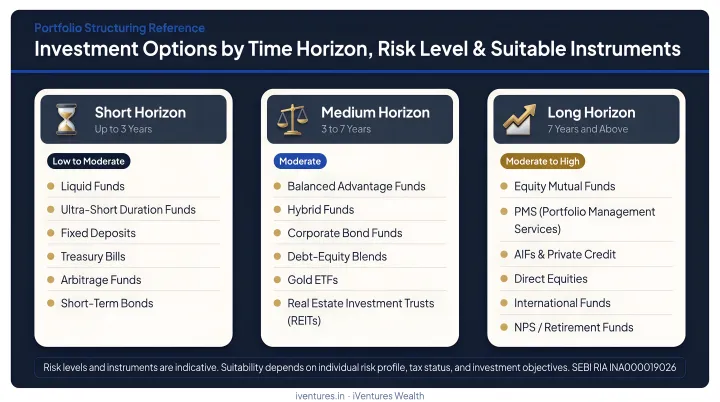

Investment Options by Time Horizon

| Time Horizon | Risk Level | Suitable Instruments |

|---|---|---|

| 0–1 year | Low | Liquid/overnight funds, high-yield savings |

| 1–3 years | Low–Medium | Ultra-short & short-duration debt funds, FDs |

| 3–7 years | Medium | SIPs in balanced/hybrid mutual funds, ELSS |

| 7+ years | Medium–High | Equity mutual funds, direct equity, ETFs |

| Long-term + tax benefit | Medium–High | ELSS (Section 80C), PPF |

Knowing these categories exist is a start. Knowing which combination suits your income stage, goals, and risk tolerance is where the real work begins. A SEBI-registered adviser like iVentures Wealth maps each allocation to a defined purpose — so your money isn't just parked somewhere, it's working toward something specific.

Setting Financial Goals You'll Actually Achieve

The SMART Framework Applied to Finance

Vague goals don't get funded. The difference between "I want to retire comfortably" and "I want ₹5 crore in 20 years, starting SIPs today" is everything. One is a wish; the other is a plan you can actually execute.

SMART goals are:

- Specific: State the exact rupee amount

- Measurable: Track progress monthly or quarterly

- Achievable: Realistic given your current income and commitments

- Relevant: Aligned with what actually matters to your life

- Time-bound: A clear deadline drives action

Here's how the SMART framework translates across different financial horizons:

| Type | Goal |

|---|---|

| Short-term (0–2 years) | Build ₹3 lakh emergency fund in 18 months via ₹16,667/month transfer |

| Medium-term (3–7 years) | Accumulate ₹25 lakh for home down payment in 5 years via monthly SIPs |

| Long-term (10+ years) | Create ₹2 crore retirement corpus in 20 years through consistent equity SIPs |

Prioritising When Resources Are Limited

Trying to pursue all goals simultaneously — without a hierarchy — leads to underperformance on all of them. Follow this order:

- Emergency fund (3–6 months of expenses)

- Eliminate high-interest debt (credit cards first)

- Tax-efficient savings (PPF, ELSS within 80C limits)

- Long-term wealth-building investments (equity SIPs, diversified portfolio)

Review Regularly

Financial goals should be revisited at least once a year, or after any major life event. Tracking progress — whether through a spreadsheet or a portfolio app — keeps goals front of mind and progress measurable.

Trigger a review after any of these:

- Salary change or job switch

- Marriage or divorce

- Birth of a child

- A property purchase or major inheritance

When to Work With a Professional Wealth Manager

DIY personal finance works well when your situation is straightforward. Once complexity builds — multiple accounts, cross-border obligations, business exits — it outpaces what a spreadsheet and annual review can handle.

Signs You Need Professional Guidance

- Portfolio spread across multiple accounts, brokers, and asset classes with no consolidated view

- ESOP vesting, business exit proceeds, or inheritance requiring structured deployment

- NRI or cross-border tax obligations

- Growing income with no clear investment strategy beyond "FDs and a few mutual funds"

- Repeated return-chasing behaviour — moving between hot funds without a plan

What to Look for in a Financial Adviser

- **SEBI registration as an Investment Adviser** (verifiable on SEBI's public registry)

- Fiduciary duty — adviser's income must not depend on commissions from products sold to you

- Credentials: CFA charterholder, CFP, or equivalent

- Transparent fee structure: You pay a direct advisory fee; the adviser earns nothing from product manufacturers

iVentures Wealth (SEBI RIA: INA000019026) operates on this model. With ₹1,200+ crore in assets under management since 2005, their open-architecture approach means recommendations span the full regulated product universe — mutual funds, PMS, AIFs, bonds, global funds — without commission-driven bias. Research is led by Krishna Makhariya, CFA, whose team's analysis drives every recommendation rather than product incentives.

The "Only for the Ultra-Wealthy" Misconception

Many people assume wealth managers are reserved for the very rich. The reality is that building a professional advisory relationship early — ideally when you begin investing meaningfully — produces better outcomes: sharper goal alignment, proactive tax planning, and the behavioural discipline that prevents costly mistakes during volatile markets.

iVentures serves clients from HNIs upward (minimum thresholds: ₹5 crore for NRIs/OCIs, ₹10 crore for CXOs and professionals). If you're approaching those thresholds, that's the right time to structure an advisory relationship — while your options are still open, not after complexity forces the decision.

Frequently Asked Questions

What is personal finance and money management?

Personal finance refers to how an individual manages income, expenses, savings, debt, and investments to meet specific life goals. Money management is the day-to-day practice — budgeting, tracking spending, and making conscious financial decisions — that puts that broader plan into action.

What are the four pillars of personal finance?

The four pillars are earning, budgeting, saving, and investing. Protection through insurance is widely considered a fifth cross-cutting pillar. Each pillar supports the others: strong earnings are wasted without budgeting, and savings without investing lose real value to inflation.

What is the 70/20/10 rule in money management?

The 70/20/10 rule allocates 70% of take-home income to living expenses, 20% to savings and investments, and 10% to debt repayment or charitable giving. It's practical for those balancing everyday costs with existing EMI obligations, making it a useful alternative to the 50/30/20 rule.

What are the seven steps in personal finance?

A logical sequence to follow:

- Assess your current financial position

- Set clear, time-bound goals

- Build a working budget

- Create an emergency fund

- Eliminate high-interest debt

- Start saving and investing consistently

- Protect and review your plan regularly

How much should I save from my monthly salary?

The commonly cited benchmark is at least 20% of take-home pay. The right percentage depends on your income level, existing debts, life stage, and goals. The key discipline is saving first, before discretionary spending, rather than saving whatever remains at month-end.

When should I start investing in India?

The best time is as soon as you have a basic emergency fund in place and high-interest debt is under control. Starting early matters more than starting with a large amount. A longer investment horizon gives compounding more time to work in your favour.