Under the Foreign Exchange Management (Non-debt Instruments) Rules, 2019, OCIs are treated on par with NRIs for most investment purposes. You can open NRE/NRO accounts, invest in mutual funds and equities, buy property, and follow the same repatriation rules. A few restrictions apply, and the compliance setup across two tax jurisdictions adds complexity — but the investment universe is wide open.

This guide covers everything OCI cardholders need to know: which instruments are permitted, which aren't, how banking and taxation work, and how to get started.

Key Takeaways

- OCIs are treated like NRIs under FEMA and can invest in mutual funds, equities, fixed deposits, and residential/commercial property

- NRE or NRO accounts are mandatory before investing — Indian AMCs and brokerages cannot accept foreign currency directly

- Restricted categories include agricultural land, PPF, Sukanya Samriddhi Yojana, Sovereign Gold Bonds, and NPS Tier 2

- DTAA shields against double taxation, but benefits require a Tax Residency Certificate (TRC) and Form 10F to claim

- Repatriation is unlimited from NRE accounts; NRO repatriation is capped at USD 1 million per financial year

OCI vs NRI: What It Means for Your Investments

OCI (Overseas Citizen of India) status is granted under Section 7A of the Citizenship Act, 1955. OCI cardholders hold foreign passports and are classified as foreign nationals — not Indian citizens.

What the status does provide is lifelong visa-free travel, the right to work and study in India, and investment parity with NRIs across most financial and economic activities.

Where the Parity Actually Sits

SEBI's investor education material confirms that "investments by OCI card holders are treated at par as NRIs" for securities-market purposes. The FEMA Non-debt Instruments Rules, 2019 use the formulation "NRI or OCI" consistently across permitted investment routes: listed equity, mutual fund units, and others. For investment purposes, any NRI guide applies directly to OCIs.

What OCI Does NOT Cover

A few restrictions carry directly into the investment domain:

- No voting rights or government job eligibility

- No agricultural land — OCI cardholders cannot purchase agricultural land, plantation property, or farmhouses under FEMA (inheritance through permitted routes is an exception)

- No resident-only schemes — PPF, SSY, and Sovereign Gold Bonds are restricted to resident Indian citizens

Outside these carve-outs, OCI investment rights are nearly identical to NRI rights.

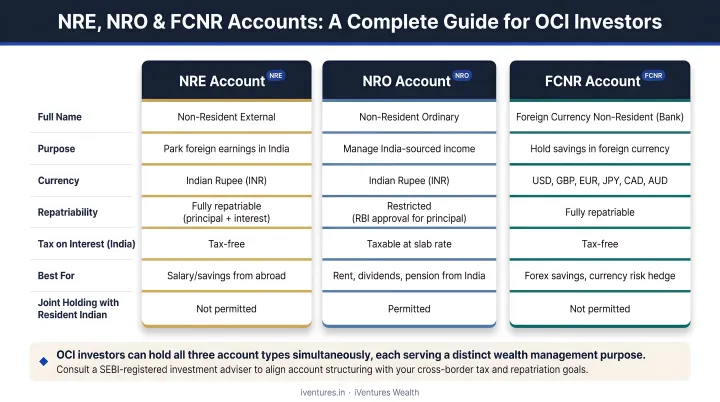

Essential Banking Setup: NRE, NRO, and FCNR Accounts

Before making any investment in India, OCIs must hold India-based bank accounts. Indian AMCs and brokerages cannot accept direct foreign currency investments — OCIs must route funds through regulated non-resident accounts.

There are three account types to know:

NRE (Non-Resident External) Account

The primary account for parking foreign earnings in India in INR.

- Interest is tax-free in India under Section 10(4)(ii) of the Income Tax Act

- Funds are fully repatriable — principal and returns can be transferred abroad without limits

- Most commonly used for OCI investments in mutual funds and equities

- The default choice for OCIs investing from foreign income

The NRE account handles foreign income cleanly. For money already earned inside India, a different account applies.

NRO (Non-Resident Ordinary) Account

Designed for India-sourced income — rent, dividends, pension, or freelance earnings from Indian clients.

Interest is taxable at 30% plus surcharge and cess (TDS deducted at source)

Repatriation is capped at USD 1 million per financial year (April–March)

Repatriation requires a CA certificate via Form 15CA/15CB

Less flexible than NRE for investors prioritizing easy repatriation

For OCIs who want to avoid rupee exposure entirely, there is a third option.

FCNR (Foreign Currency Non-Resident) Account

A fixed deposit account held in foreign currencies — USD, GBP, EUR, CAD, AUD, JPY, and SGD.

- Eliminates rupee exchange-rate exposure entirely

- Interest is tax-free in India and fully repatriable

- Most useful when rupee depreciation is a concern and funds will eventually return abroad

Practical recommendation: Most OCIs need both — an NRE account for investing foreign income, and an NRO account if they receive any India-sourced income. FCNR becomes worth considering specifically when currency risk is a priority — for instance, if you're holding a significant fixed-deposit corpus that you plan to redeploy abroad within 1–3 years.

What OCI Cardholders Can (and Cannot) Invest In

Permitted Investments

Mutual Funds

OCIs can invest in Indian equity, debt, and hybrid mutual funds using NRE or NRO accounts, subject to KYC and FATCA compliance. Both lump sum investments and SIPs are available.

One important caveat: some AMCs decline applications from US- and Canada-based investors due to FATCA and securities-law compliance complexity. Zerodha's NRI mutual fund guide confirms this is AMC-specific, not a blanket regulatory ban.

Several major fund houses — including SBI Mutual Fund and ICICI Prudential Mutual Fund — do accept US/Canada investors.

Direct Equity (Stocks)

OCIs can buy NSE/BSE-listed shares through the Portfolio Investment Scheme (PIS) route via a designated bank. Key requirements:

- An NRE PINS account with a designated bank

- A demat and trading account with a SEBI-registered broker

- Delivery-based trades only — intraday trading, STBT, and BTST are not permitted under PIS accounts

Fixed Deposits

OCIs can open FDs under NRE, NRO, or FCNR accounts. Current indicative rates from major banks:

| Account Type | Representative Rate (2026) | Tax Treatment |

|---|---|---|

| NRE FD (SBI, 1–2 years) | ~6.25%–6.45% p.a. | Tax-free in India |

| NRO FD (ICICI, 2–3 years) | ~6.45%–6.50% p.a. | Taxable at 30% + cess |

| FCNR USD (SBI) | ~2.95%–4.40% p.a. | Tax-free in India |

Rates are indicative and change frequently — verify directly with banks before investing.

Real Estate

Per RBI guidelines, OCIs can purchase residential and commercial property in India without RBI approval, with no limit on the number of properties. Funds must come from NRE/NRO/FCNR accounts or direct foreign remittance — not foreign currency notes or traveller's cheques.

Other Permitted Instruments

- Government securities and RBI bonds (via NRE/NRO accounts)

- Tax-free bonds and ETFs

- NPS Tier 1 accounts (same exit rules as residents)

- REITs and InvITs for real estate exposure without direct ownership

Not every asset class is open to OCI cardholders, however. Several categories remain off-limits under FEMA and sector-specific regulations.

Investments OCIs Cannot Make

| Restricted Instrument | Reason |

|---|---|

| Agricultural land, farmhouses, plantation property | Prohibited under FEMA to protect India's agricultural resources |

| PPF (Public Provident Fund) | Restricted to resident Indians; new accounts cannot be opened by OCIs |

| Sukanya Samriddhi Yojana | Requires resident Indian citizen status; account closes if holder becomes non-resident |

| Sovereign Gold Bonds | Available only to resident Indian entities |

| NPS Tier 2 accounts | PFRDA rules prohibit NRIs/OCIs from activating Tier 2 |

On PPF specifically: existing accounts opened while the OCI was a resident Indian may continue to maturity, but cannot be extended — new accounts are closed to OCIs.

Taxation and Repatriation Rules for OCI Investors

Tax Residency: The Starting Point

OCIs are tax residents of the country where they live — the US, UK, UAE, or elsewhere. India is not their tax domicile. However, India taxes India-sourced income: interest, dividends, and capital gains from Indian investments. This creates potential double taxation, which DTAA addresses.

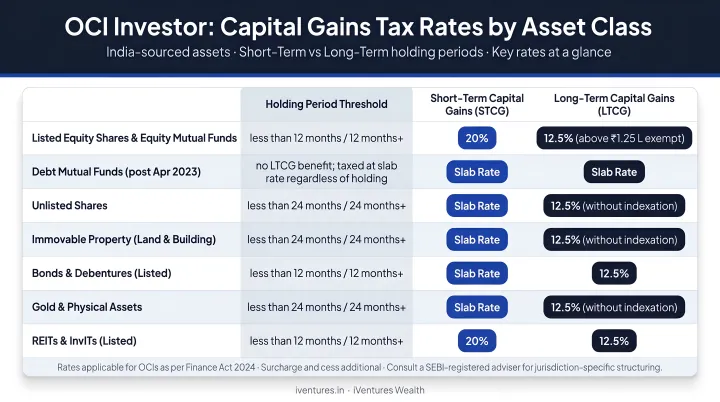

Capital Gains Tax Rates for OCIs

Post-23 July 2024, the following rates apply:

| Asset Class | Holding Period | Tax Rate |

|---|---|---|

| Listed equity / equity mutual funds (STCG) | ≤12 months | 20% |

| Listed equity / equity mutual funds (LTCG) | >12 months | 12.5% on gains above ₹1.25 lakh |

| Debt mutual funds | Any | Taxed at slab rate (deemed short-term under Section 50AA) |

| Real estate (LTCG) | >24 months | 12.5% without indexation (post July 2024) |

TDS is deducted at source by AMCs and banks — for most instruments, OCIs do not need to calculate or remit this separately.

DTAA: Avoiding Double Taxation

India has tax treaties with numerous countries. Under DTAA, OCIs who have paid tax in India can claim a foreign tax credit in their country of residence. DTAA benefits are not automatic. To claim them:

- Obtain a Tax Residency Certificate (TRC) from your country of residence

- Submit Form 10F to Indian tax authorities

- Provide a DTAA declaration to banks before they deduct NRO TDS at the standard 30% rate — without this, banks default to the higher withholding rate regardless of any treaty benefit you're entitled to

Repatriation: NRE vs NRO

The account type determines how easily you can move money back:

- NRE account funds: Fully repatriable , no limits, no paperwork, no CA certificate required

- NRO account funds: Up to USD 1 million per financial year, after paying applicable taxes and obtaining Form 15CA/15CB from a CA

OCIs who anticipate repatriating investment proceeds should route those investments through NRE accounts wherever possible.

International Reporting Obligations

Regardless of India's tax treatment, OCIs must report Indian assets and income in their country of residence. US-based OCIs face two specific requirements:

- FBAR: Required if aggregate foreign account balances exceed USD 10,000 at any point in the calendar year (filed via FinCEN's BSA E-Filing system)

- Form 8938 (FATCA): Required for unmarried US-resident individuals with foreign assets above USD 50,000 on the last day of the year (or USD 75,000 at any point)

Reporting requirements differ substantially by country of residence. Given these complexities, iVentures Wealth's cross-border advisory services help OCI investors map their obligations across jurisdictions before they become compliance gaps.

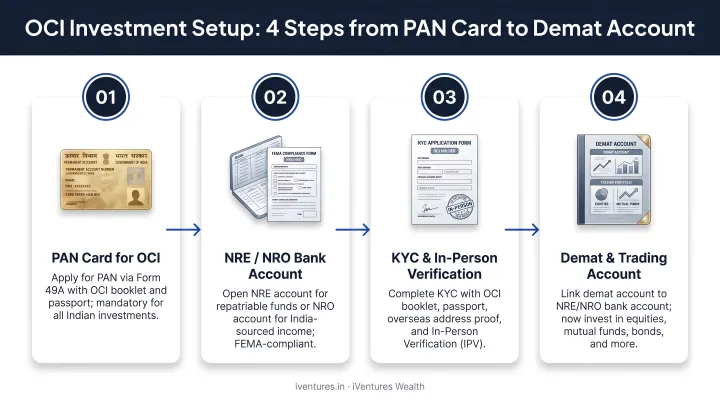

How to Start Investing in India as an OCI Cardholder

The Four-Step Setup

- Get a PAN card — Mandatory for all investment transactions in India. Apply using Form 49AA with your OCI card, foreign passport, and overseas address proof via the Protean (formerly NSDL) portal

- Open NRE and/or NRO accounts with an Indian bank that supports non-resident accounts (SBI, HDFC, ICICI, and Axis all have dedicated NRI/OCI banking teams)

- Complete OCI KYC — Submit OCI card, foreign passport, overseas address proof, and recent photographs. FATCA declarations are also required

- Open a demat and trading account with a SEBI-registered broker that supports NRI/OCI PIS accounts (required for equity investments)

Using a Power of Attorney

OCIs who cannot travel to India can authorise a trusted person to manage investments through a notarised Power of Attorney. The PoA holder can buy/sell mutual funds, sign investment documents, and manage account-level transactions. The PoA must be attested by the Indian consulate in your country of residence before it's valid in India.

Getting Expert Help

Cross-border investment involves layered compliance — DTAA claims, FEMA-compliant account structures, Form 15CA/15CB filings, and repatriation rules that differ by account type and asset class. Getting this wrong can trigger tax complications in both countries.

iVentures Wealth (SEBI RIA: INA000019026) has worked with OCI investors for 20+ years, handling this full compliance stack in-house — including DTAA structuring, FEMA-compliant setup, and repatriation planning. The team coordinates with clients' existing CAs where applicable. All assets remain in the client's own accounts. Minimum threshold: ₹5 Cr for OCI clients.

Frequently Asked Questions

Is OCI treated the same as NRI for investment purposes?

For most investment purposes under FEMA, yes. OCIs can open NRE/NRO accounts, invest in mutual funds, equities, and real estate, and follow the same tax and repatriation rules as NRIs. The main exceptions are agricultural land, PPF, SSY, and Sovereign Gold Bonds, which are restricted to resident Indians.

Can I buy property in India if I have OCI?

OCIs can purchase both residential and commercial property without RBI approval and with no limit on the number of properties. Agricultural land, farmhouses, and plantation property remain prohibited under FEMA.

Can OCI invest in FD in India?

OCIs can open fixed deposits under NRE, NRO, or FCNR accounts. NRE and FCNR FD interest is tax-free in India and fully repatriable. NRO FD interest is taxable at 30% plus cess, with repatriation subject to the USD 1 million annual cap and CA documentation.

Can OCI use Zerodha?

OCIs can use Zerodha through an NRI demat and trading account linked to an NRE PINS or NRO account. Check directly with Zerodha for current documentation requirements, as restrictions may apply for US- or Canada-based investors.

Do OCIs need a PAN card to invest in India?

A PAN card is mandatory under Rule 114B for demat accounts, mutual fund investments above ₹50,000, property transactions, and other specified financial transactions. Apply using Form 49AA with your OCI card and foreign address proof.

Can OCIs repatriate their investment proceeds from India?

It depends on the account used. NRE account investments are fully repatriable with no limits or additional paperwork. NRO account proceeds can be repatriated up to USD 1 million per financial year after paying applicable taxes and filing CA-certified Form 15CA/15CB.