Introduction

Running a business creates a paradox most founders discover too late: the harder you work to grow the company, the more concentrated your personal wealth becomes — and the more exposed it is to a single point of failure.

Generic financial planning assumes a salary, an employer-provided retirement plan, and diversified savings. Business owners have none of that by default. They manage a personal balance sheet and a business balance sheet, typically without a clear boundary between the two.

The mistakes that erode wealth here aren't unusual. They follow a pattern:

- Mixing personal and business accounts until both become opaque

- Reinvesting every rupee back into the business, treating growth as the only wealth strategy

- Assuming the business itself will fund retirement

- Delaying succession conversations until a health event or family dispute forces the issue

Left unaddressed, these aren't just planning gaps — they become liquidity crises, family disputes, and lost decades of wealth-building. This guide works through five pillars that directly counter them: financial separation, portfolio diversification, tax optimisation, risk management, and succession planning.

Key Takeaways

- Legally separating personal assets from business liabilities — through a Pvt Ltd, LLP, or private trust — is the non-negotiable first step

- With 80–90% of a business owner's net worth tied up in the business, building disciplined investments outside it isn't optional

- Proactive tax planning covers business income, director remuneration, capital gains, and exit structuring — not just year-end adjustments

- Personal life, disability, and key-person insurance are chronically underutilised, especially among Indian HNIs

- Succession planning needs a 5–10 year runway, not a last-minute conversation triggered by a pending sale

Separating Personal and Business Finances

Why Commingling Is a Structural Risk

In many Indian SMEs and family businesses, business accounts and personal accounts are effectively the same thing. Money flows freely between them based on immediate need rather than financial logic. This creates two distinct problems.

The first is legal. When personal and business finances are intertwined, business creditors can potentially attach personal assets. According to the International Finance Corporation's MSME risk-capital report, Indian financial institutions regularly use promoter personal assets as collateral for MSME secured lending — meaning the boundary between personal and business balance sheets is already blurred even before a default event.

The second is practical. Commingled accounts make it nearly impossible to assess your true personal net worth, file clean ITRs, or present credible accounts during a business valuation or sale process.

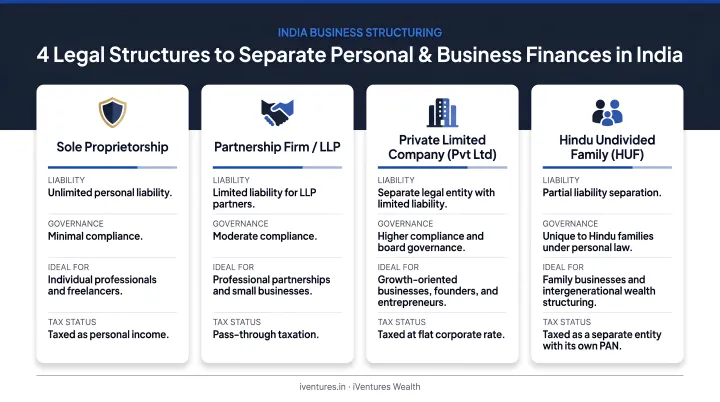

Structures That Create Legal Separation

Indian business owners have several practical tools:

- Private Limited Company or LLP for business operations — both are separate legal entities under the Companies Act, 2013 and the LLP Act, 2008 respectively, meaning business obligations are not personal obligations (with limited exceptions for fraud)

- Private Family Trust under the Indian Trusts Act, 1882 for holding personal wealth — trust property is legally distinct from the trustee's personal estate

- HUF (Hindu Undivided Family) as a separate taxpayer category for family-pooled assets, though it carries no limited liability protection for business debts

- Separate bank accounts and PAN-linked investment accounts for each entity — a basic step that many founders skip

Clean separation delivers three concrete compliance advantages: cleaner ITR filings, reduced audit exposure, and documentation that holds up when a buyer or investor requests a formal valuation.

At iVentures Wealth, one of the first steps in advising business owner clients is establishing a clear profit-allocation policy: separating working capital, business reserves, and the promoter's personal drawings into distinct structures. That clarity removes the guesswork from tax planning, succession discussions, and any future capital raise.

Building a Diversified Investment Portfolio Beyond Your Business

The Concentration Risk Problem

The Exit Planning Institute estimates that 80–90% of a business owner's net worth is tied up in the value of the business. That figure isn't surprising — but it should be alarming. A single regulatory change, sectoral downturn, or key client loss can devastate personal wealth when there's no financial life outside the business.

This is the core wealth risk for Indian founders and promoters: not market volatility, but concentration.

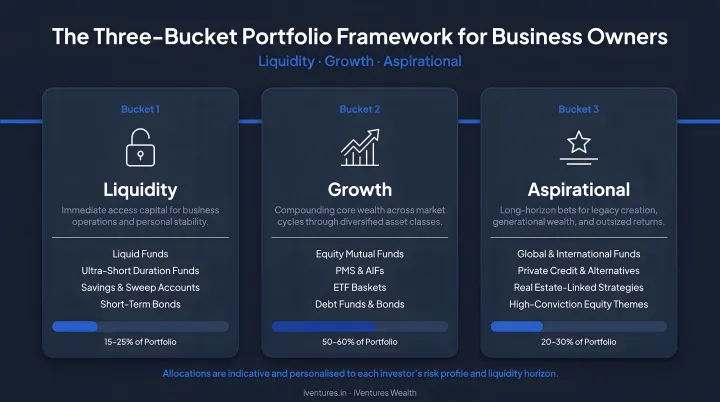

The Three-Bucket Portfolio Framework

A structured approach that works well for business owners divides investable assets into three distinct buckets:

Bucket 1 — Liquidity (Safety)

- 12–18 months of personal expenses in liquid funds, short-duration debt, or high-quality fixed income

- Purpose: covers family needs and emergencies without touching business capital or forcing untimely asset sales

- At iVentures, this is structured as 5–7 years of expenses for post-exit founders, given the unpredictability of business cash flows

Bucket 2 — Core Growth

- Diversified equities, mutual funds, or PMS products for long-term compounding

- Horizon: 8–15 years

- Goal: build personal retirement corpus entirely independent of business performance

Bucket 3 — Aspirational

- Higher-risk, higher-return opportunities: AIFs, pre-IPO deals, private equity, REITs/InvITs

- Sized appropriately to risk tolerance — not the primary wealth vehicle

SEBI-Regulated Products for HNI Business Owners

Business owners with meaningful investable assets can access vehicles unavailable to retail investors:

| Product | Minimum Investment | Suitable For |

|---|---|---|

| Portfolio Management Services (PMS) | ₹50 lakh (SEBI mandated) | Core equity exposure with active management |

| Category II AIFs (PE, debt, real estate funds) | ₹1 crore (SEBI mandated) | Mid-conviction, illiquid growth allocation |

| Category III AIFs (hedge/complex strategies) | ₹1 crore (SEBI mandated) | Sophisticated return-seeking strategies |

| REITs / InvITs | Listed on exchanges | Liquid real estate income, 6–8% quarterly yields |

Choosing the right products across these categories is only half the equation. What often goes undetected is how holdings across personal accounts, HUF structures, and business-linked investments interact with each other. At iVentures Wealth, our CFA-led research team uses the Wealth Monitor App to consolidate this view across all your entities — so rebalancing decisions are based on your actual total exposure, not just one account in isolation.

Tax Optimisation Strategies for Business Owners in India

Business owners face a multi-layered tax burden that salaried professionals simply don't encounter. Managing it requires planning across four distinct dimensions simultaneously.

Business Income and Director Remuneration

The applicable corporate tax rate depends on company type:

| Company Type | Section | Tax Rate |

|---|---|---|

| Domestic companies (opt-in) | 115BAA | 22% |

| New manufacturing companies | 115BAB | 15% |

Dividends paid to shareholders have been taxable in shareholders' hands since April 1, 2020 — the earlier DDT regime no longer applies.

This creates a meaningful optimisation question: how much should a founder-director take as salary versus declare as dividends? The answer depends on individual tax brackets, company structure, and cash flow needs. A wealth advisor who understands both personal and corporate tax structures can model the split specific to your situation — the right ratio shifts significantly based on your effective marginal rate.

Capital Gains Tax Planning for Personal Portfolios

Post-Budget 2024, the capital gains framework changed in ways that affect most business owners' personal portfolios:

- Section 112A (listed equity LTCG): Exemption threshold raised to ₹1.25 lakh; rate updated to 12.5%

- Other LTCG (including unlisted shares): Rationalised to 12.5% without indexation under Section 112 (previously 20% with indexation)

Key personal portfolio tax strategies:

- Hold investments beyond 12–24 months to access LTCG rates rather than STCG

- Use tax-loss harvesting to offset gains within the same financial year

- Invest up to ₹1.5 lakh annually in ELSS funds under Section 80C (3-year lock-in, equity returns, tax deduction)

- Claim the additional ₹50,000 deduction under Section 80CCD(1B) through NPS contributions

Business Exit Tax Planning

Capital gains planning for personal portfolios is one layer — but a business exit adds another. When a founder sells equity in a private company, tax treatment depends on the holding period, transaction structure (asset sale vs. share sale), and whether any reinvestment provisions apply.

Two provisions worth understanding with your tax advisor:

- Section 54F: Applies to LTCG from any long-term capital asset (other than a residential house) if net consideration is reinvested in one residential property within specified time limits

- Section 54EC: Applies to LTCG from land or building — allows investment of up to ₹50 lakh in specified bonds (NHAI, REC) within 6 months to defer tax. Note this applies specifically to land/building, not founder equity.

One recent development that removes a material concern: angel tax has been abolished for all classes of investors effective April 1, 2025 (Finance (No. 2) Act, 2024), eliminating a significant hurdle for founders raising capital.

Retirement Structures Through the Business

NPS contributions offer self-employed business owners:

- Deduction up to 20% of gross income under Section 80CCD(1), within the ₹1.5 lakh Section 80CCE ceiling

- Additional deduction of up to ₹50,000 under Section 80CCD(1B)

PPF contributions also qualify under Section 80C and receive EEE tax treatment (exempt at contribution, accumulation, and withdrawal stages).

Risk Management and Asset Protection

Two Categories of Risk

Business owners face risks that fall into two categories — each demanding a different response:

Insurable risks:

- Personal liability

- Business liability and professional indemnity

- Key-person events (death or incapacitation of a critical founder or employee)

- Property and asset damage

Uninsurable risks:

- Over-concentration in a single private business

- Overdependence on a single major client or contract

- Poor debt structure that leaves personal assets exposed

- Succession failure that leaves the business without leadership

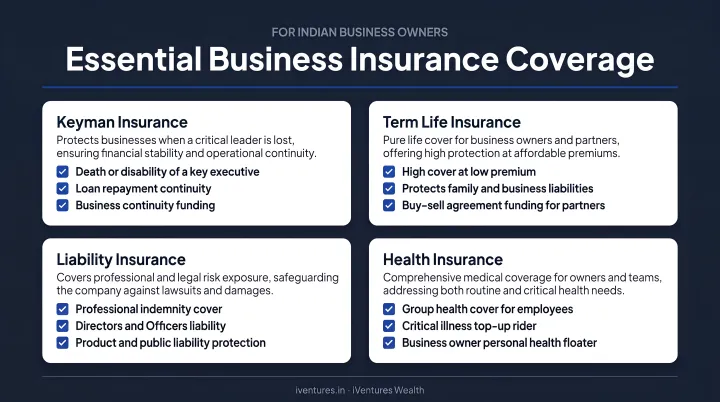

Insurance Coverage for Indian Business Owners

India's overall insurance penetration stood at 3.7% (life at 2.7%, non-life at 1.0%) according to PIB releases citing IRDAI data — which reflects a chronic underinsurance problem that affects HNIs and business owners as much as the broader population.

The minimum insurance coverage a business owner should have:

- Key-person (keyman) insurance: Protects the business against the financial impact of losing a founder or critical employee — premiums are a business expense, and the policy proceeds flow to the company

- Personal term plan: Sized to replace income for 10–15 years for dependents; separate from any business-linked coverage

- Business liability insurance: Essential for sectors with high litigation or regulatory exposure

- High-sum health and critical illness cover: Many business owners rely on group covers that lapse when they step back from day-to-day operations

Asset Protection Through Legal Structuring

Holding personal assets — property, securities, liquid savings — in a private family trust creates a structural barrier between personal wealth and business creditors. Under the Indian Trusts Act, 1882, trust property is legally distinct from the trustee's own estate.

This structure is most relevant for:

- Capital-intensive businesses carrying significant debt

- Industries with meaningful litigation or regulatory exposure

- Promoters who want a clean separation between personal and operational risk

Getting this structure right early — before a dispute or credit event — is what separates proactive wealth protection from reactive damage control.

Retirement and Succession Planning: Building a Legacy Beyond the Business

Retirement Planning for Business Owners

The most dangerous assumption a business owner can make is that the business will fund retirement. Business valuations fluctuate. Planned exits fall through. Health may force an early departure. The next generation may have different priorities.

Retirement savings vehicles worth structuring now:

- NPS: Deductions under 80CCD(1) and the additional ₹50,000 under 80CCD(1B) make this the most tax-efficient retirement vehicle for self-employed individuals

- PPF: EEE treatment makes it a useful lower-risk accumulation vehicle, though the annual cap limits it to a supplementary role in larger portfolios

- Formal superannuation or gratuity fund through the business: Creates a retirement corpus while reducing company taxable income — worth exploring with a tax advisor for businesses with stable employee structures

The goal: build a retirement corpus that can fully sustain personal lifestyle even if the business were worth zero on exit day.

Succession Planning and Business Exit

According to the PwC India Family Business Survey 2019, only 21% of Indian family businesses had a robust, documented, and communicated succession plan — meaning nearly four in five were operating without one.

A functional succession plan for an Indian family business or founder-led company involves:

- Independent business valuation to establish a fair baseline for ownership transfer, buy-sell agreements, and tax calculations

- Ownership transfer structure chosen from a buy-sell agreement, private trust, or ESOP framework under Companies Act Section 62(1)(b) — each with distinct tax and control implications

- Exit tax structuring around asset sale vs. share sale, holding period, and reinvestment provisions to minimise capital gains liability

- Leadership continuity — identifying and preparing successors, whether family members or professional management, well before the transition date

Legacy and Estate Planning

Estate planning gaps are surprisingly common among affluent business owners — and the consequences surface at the worst possible time. The most frequent: missing nominees on financial accounts, no Will in place, and family members operating under the misconception that a nominee is a legal heir. A nominee is a custodian only; legal ownership follows succession law and a registered Will.

The key components of a complete estate plan:

- A registered Will covering all financial and digital assets (defined under Indian Succession Act, 1925 Section 2(h) as a legal declaration of intent with respect to property)

- A private family trust for inter-generational wealth transfer, especially useful when there are multiple beneficiaries or blended family structures

- Nominees designated on every investment account, insurance policy, and bank account — cross-checked against the Will to ensure consistency

Starting this process 5–10 years before any planned exit avoids the legal delays and family disputes that inadequate planning creates. iVentures Wealth has worked with 150+ affluent families and founders on succession and legacy strategies — from Will drafting vetted by senior legal counsel to private trust establishment — integrating these steps into a broader wealth plan rather than treating them as a last-minute checklist.

Frequently Asked Questions

How is wealth management for business owners different from regular financial planning?

Business owners carry two balance sheets at once — personal and business — with no employer retirement plan, complex tax structures, and most of their wealth locked in a single illiquid entity. Generic financial planning, built for salaried individuals, cannot address that complexity. An integrated approach is essential.

How can a business owner in India separate personal and business finances?

Use distinct legal entities (LLP or Pvt Ltd for business operations, a private trust or HUF for personal wealth), maintain separate bank accounts for each, and keep all personal investments under your individual PAN. This separation protects personal assets from business creditors and simplifies ITR filing.

What tax-saving strategies are available for business owners in India?

Core options for business owners in India include:

- Salary vs. dividend optimisation to reduce total tax outflow

- NPS contributions under Section 80CCD(1B) for an additional ₹50,000 deduction

- ELSS investments within the ₹1.5 lakh Section 80C limit

- Tax-loss harvesting in your personal portfolio

- Structuring business exit transactions to manage capital gains

When should a business owner start succession planning?

Start 5–10 years before any expected exit or ownership transfer. Business valuation, legal structuring, tax planning, and leadership continuity all demand extended preparation that cannot be compressed into a few months before a transaction closes.

How much of a business owner's wealth should be invested outside the business?

A practical benchmark: your retirement security and lifestyle expenses should be fully fundable even if the business were worth zero. For most owners, that means building meaningful investable assets outside the business well before any planned exit — the exact proportion depends on business size, stage, and personal income needs.

Do I need a SEBI-registered advisor to manage my wealth as a business owner?

SEBI-registered advisors operate under a fiduciary standard, legally bound to act in your interest — an obligation distributors and unregistered advisors do not carry. For business owners managing multi-entity, multi-asset structures, that distinction matters considerably.