Key Takeaways

- A financial advisor begins with a complete audit of all liabilities, income, and financial goals before recommending any strategy.

- Repayment strategies — avalanche, snowball, consolidation, or refinancing — are matched to both the numbers and the client's actual behaviour.

- Effective debt management integrates with investment planning, tax optimisation, and liquidity — it cannot be handled in isolation.

- SEBI registration, fiduciary status, and relevant credentials are non-negotiable when selecting an advisor for debt guidance.

- Early advisor engagement preserves more restructuring options — waiting narrows what's possible.

Why Managing Debt Alone Is Harder Than It Looks

Affluent Indians rarely have just one debt. A typical HNI profile might include a home loan, a business overdraft, a loan against securities, and one or two credit card balances — all carrying different interest rates, tax treatments, and repayment structures. Managing that mix without a framework is where most mistakes happen.

The Behavioural Problem

Research published in the Journal of Marketing Research identified what academics call "debt account aversion" — borrowers tend to prioritise closing the smallest accounts even when that directly conflicts with minimising total interest paid. The instinct to reduce the number of debts, rather than the cost of debt, is a deeply human response. It feels like progress, even when it isn't.

Unplanned repayment — paying whichever loan feels most pressing — can cost far more over three to five years than a structured approach would.

The Complexity Problem

Different debt types require completely different treatment:

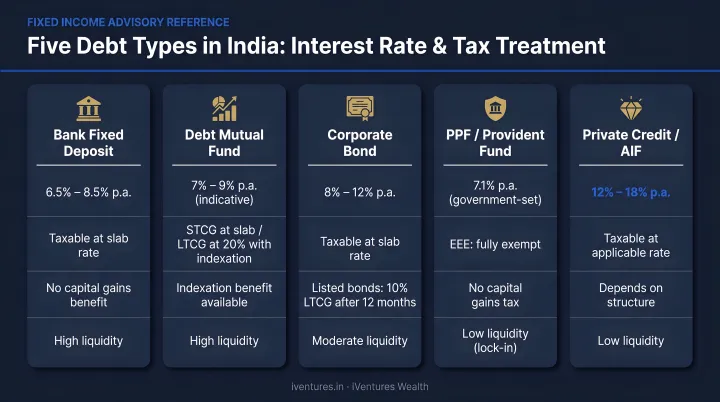

- Home loans — interest deductible up to ₹2,00,000 per year under Section 24(b); principal repayment eligible under Section 80C

- Credit card revolving debt — ICICI charges 3.75% per month (45% p.a.) on unpaid dues; HDFC can reach 3.4% per month

- Personal loans — high flat rates, no tax benefit, no collateral offset

- Loan against securities (LAS) — SBI charges 9.95% p.a. on mutual fund units; ICICI's mean rate is 10.15% p.a.

- Business overdrafts — linked to working capital cycles, require tenor matching

Each of these demands a different repayment priority. Treating them uniformly is one of the most expensive mistakes affluent borrowers make.

That complexity makes the next problem worse.

The Either/Or Trap

Many clients frame debt repayment and investing as competing choices — every rupee going to a loan is a rupee not compounding in markets. A good advisor rejects that framing. The real question is which allocation produces the better after-tax outcome. For a borrower holding both a 45% p.a. credit card balance and an equity portfolio generating 12% CAGR, the answer is obvious. For someone with a tax-deductible home loan at 8.5% against the same portfolio, it isn't — and getting it wrong in either direction can quietly erode lakhs over a decade.

What a Financial Advisor Does for Debt Management

Before recommending any repayment method, an advisor maps the client's full financial picture — liabilities, cash flows, assets, and credit health — so that any strategy is grounded in reality rather than assumption.

Financial Assessment

The initial engagement typically involves a full audit of the client's financial position:

- All outstanding liabilities: home loans, personal loans, vehicle EMIs, credit card balances, business credit lines, LAS/LAP

- Monthly cash flows: salary, business income, rental income, investment returns

- Asset base: liquid investments, real estate, securities portfolio

- Debt-to-income ratio and overall debt serviceability

- CIBIL score review (300–900 scale) — identifying any inaccuracies that can be disputed and corrected before restructuring begins

Documents typically needed: loan statements, recent bank statements, salary slips or P&L, ITR filings from the past 2–3 years, and a CIBIL credit report.

Comprehensive Debt Analysis and Prioritisation

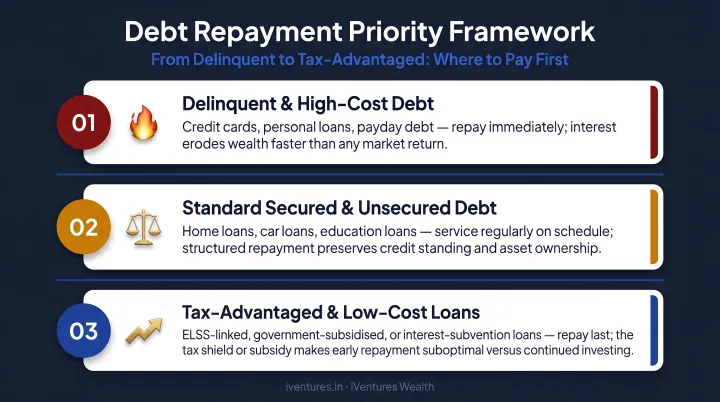

Once the full picture is clear, an advisor ranks debts strategically — not arbitrarily. The framework generally looks like this:

- Delinquent accounts first — missed payments damage CIBIL scores and trigger penalty interest

- High-interest unsecured debt next — credit card balances at 40%+ p.a. erode wealth faster than most investments can recover

- Tax-advantaged debt last — home loans with Section 24(b) deductions have a meaningfully lower post-tax interest cost

For HNI clients, advisors also review consolidation opportunities. Using a Loan Against Property (LAP) or LAS to retire high-interest unsecured debt can reduce the effective rate dramatically — replacing credit card debt at 40%+ p.a. with secured debt at 10–12% p.a. is a structural improvement that consistently justifies the restructuring effort.

Budgeting and Cash Flow Planning

Identifying the right strategy is only half the job. The other half is freeing up cash to execute it. Advisors restructure monthly budgets to:

- Identify discretionary cuts that don't compromise lifestyle materially

- Optimise EMI schedules to avoid payment misalignment

- Build a payment calendar that protects CIBIL scores while accelerating paydown

Negotiation and Creditor Communication

In distressed situations, advisors — or the restructuring teams they coordinate with — engage directly with lenders. The scope of support typically covers:

- Negotiating lower interest rates or restructured EMI schedules

- Securing temporary hardship provisions during cash flow stress

- Reviewing term sheets and renegotiating covenants for promoter-led businesses

iVentures Wealth's Corporate Debt Restructuring advisory covers all of the above, with particular depth for family enterprises and promoter-owned businesses navigating lender conversations.

Debt Repayment Strategies a Financial Advisor Will Recommend

The right repayment strategy depends on three variables: the client's debt profile, their behavioural history with money, and their broader financial goals. Advisors don't recommend a single method — they match the approach to the person.

Avalanche vs. Snowball

Debt Avalanche — Pay the highest interest rate debt first while maintaining minimum payments on others. Fidelity notes this method minimises total interest paid over time.

Debt Snowball — Pay the smallest balance first. Research confirms that small wins build intrinsic motivation and improve repayment adherence — making this method more sustainable for some clients even if it costs slightly more in interest.

The deciding factor is usually behavioural, not mathematical. Clients who have previously abandoned repayment plans often need the snowball's momentum to stay consistent — even if the avalanche saves more in the long run.

Debt Consolidation

Combining multiple high-interest debts into a single lower-rate loan reduces complexity and total interest burden. Common approaches:

- Credit card balance transfers — HSBC India charges a 1.5% processing fee (minimum ₹200) on EMI balance transfers; SBI Card requires a minimum transfer of ₹5,000

- Personal loan consolidation — replacing multiple high-rate personal loans with a single facility

- LAP/LAS to retire unsecured debt — converting 40%+ credit card debt into 10–12% secured debt

One caution: always factor in processing fees, tenure changes, and prepayment penalties before consolidating. The math needs to work across the full tenure, not just the first year.

Refinancing

Switching an existing home loan from a higher-rate lender to a lower-rate one can reduce EMI outgo substantially. HDFC Bank's balance transfer facility and similar options from other lenders exist for this purpose. Under RBI's floating-rate reset guidelines, existing borrowers also have the right to switch between fixed and floating rates, change tenure, or prepay — options many clients don't know they hold.

Advisors calculate the break-even point on refinancing before recommending it:

- Interest savings vs. switching costs — how long until savings exceed processing fees and legal charges

- Remaining tenure — shorter remaining tenures rarely justify the cost of switching

- Exit plans — if the client intends to sell or prepay within the break-even window, refinancing doesn't make financial sense

Debt Settlement

When the preceding strategies aren't viable — typically in cases of severe distress or liquidity crisis — advisors may help negotiate a one-time settlement for less than the outstanding amount. It's a last resort, and it carries real consequences. Two serious caveats:

- CIBIL marks the account as "settled" — indicating the bank accepted less than full payment. This status should be cleared by paying the balance in full and requesting removal.

- For business liabilities, Section 41(1) of the Income Tax Act taxes the remitted amount as business income if the liability was previously deducted.

Balancing Debt Payoff with Long-Term Wealth Building

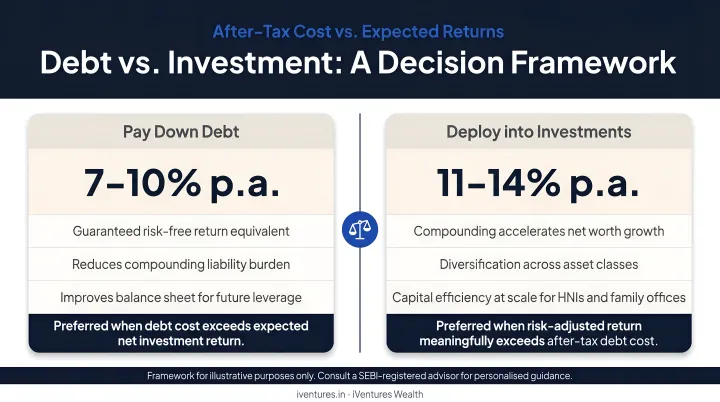

Every rupee directed at loan prepayment is a rupee not compounding in equity or mutual funds. This trade-off is where experienced advisors add the most value, because the answer depends on numbers that shift with interest rates, tax positions, and investment horizons.

The Core Calculation

The calculation comes down to one comparison: the after-tax interest cost of the debt versus the expected post-tax return on investment.

A home loan at 8.5% with a Section 24(b) deduction has an effective post-tax cost closer to 6–7% for clients in the 30% bracket. If a well-structured equity portfolio is expected to deliver 12–15% over a 10-year horizon, the math favours investing surplus capital rather than prepaying aggressively. Credit card debt at 45% p.a. is a different story: no investment reliably outperforms that cost of capital, so elimination takes priority.

That reduction changes the prepayment calculus entirely.

In practical terms, the tax benefits mean:

- A 8.5% home loan may carry an effective post-tax cost of 6–7% for a 30% bracket taxpayer

- Prepaying aggressively forfeits Section 24(b) benefits on remaining interest

- The capital redirected to prepayment loses its compounding potential in equity or debt instruments

- Each year of deduction foregone has a real opportunity cost that compounds over the loan tenure

What to Look for in a Financial Advisor for Debt Help

Debt advice can be found everywhere. The question is whether the advice is structurally sound, conflict-free, and integrated with broader wealth strategy.

Credentials and SEBI Registration

In India, look for:

- SEBI-registered Investment Advisers (RIAs) — governed by the SEBI Investment Advisers Regulations 2013, with a fiduciary obligation to act in the client's best interest. As of August 2024, only 927 Investment Advisers were registered with SEBI — a number that reflects how selective this designation is.

- CFA charterholders — bound by CFA Institute Standard III(B) on fair and objective dealing with clients

- CFPs (Certified Financial Planners) — with demonstrated experience in comprehensive financial planning

iVentures Wealth holds SEBI RIA registration (INA000019026) and is led by a CFA-qualified research team. This combination means debt advice is grounded in both regulatory accountability and investment-grade analytical rigour.

Fiduciary vs. Commission-Based

In debt advisory specifically, this distinction has direct financial consequences. A commission-based advisor may be incentivised to recommend certain loan products, refinancing arrangements, or consolidation vehicles that generate fees — not necessarily those that serve your financial situation.

A fee-only fiduciary advisor charges you directly for advice. Their recommendation is driven entirely by what the analysis shows, not by which lender or product pays them more. iVentures Wealth operates on this model — SEBI regulations prohibit registered RIAs from accepting commissions or trail fees from product manufacturers, ensuring recommendations are structurally conflict-free.

Holistic vs. Transactional

Debt advice in isolation is incomplete. An advisor who only looks at your loan statements without considering your investment portfolio, tax position, and long-term goals will optimise the wrong variable. The right advisor treats debt as one lever in a larger wealth strategy, with the analytical depth to run scenarios across liabilities, liquidity, and long-term net worth simultaneously.

Frequently Asked Questions

How can a financial advisor help with debt?

A financial advisor audits all your liabilities, recommends a prioritised repayment strategy — avalanche or snowball — and restructures where possible through consolidation or refinancing. Debt paydown is then integrated with your investment portfolio and tax planning to reduce total interest paid without compromising broader wealth goals.

How to clear ₹25 lakh debt in 5 years?

Apply the avalanche method to high-interest debt, explore consolidation to lower the blended rate, and direct annual bonuses toward systematic prepayment. A financial advisor can model the exact monthly figures and identify the fastest path based on your specific cash flow.

Will a financial advisor pull up my debts?

Your advisor will not independently pull your loans — they review documents you share directly. In some cases, with your consent, they may review your CIBIL report to get a complete picture of all outstanding liabilities before building a strategy.

What documents should I bring to a financial advisor for debt management?

Bring all loan statements (home, personal, vehicle), recent credit card bills, 3–6 months of bank statements, salary slips or income proof, ITR filings from the past 2–3 years, and a current CIBIL report. The more complete the picture, the more precise the advice.

Should I pay off debt or invest first?

Compare the after-tax interest rate on your debt against the expected post-tax return on investment. Home loan interest net of Section 24(b) deduction may cost 6–7% effectively — potentially less than long-term equity returns. Credit card debt at 45% p.a. almost always warrants repayment first. A financial advisor can model both scenarios with your specific numbers.

What is the difference between debt snowball and debt avalanche?

The snowball method pays the smallest balance first, creating psychological wins that improve adherence. The avalanche method targets the highest interest rate first, minimising total interest paid. Advisors select between them based on the numbers and the client's actual repayment track record.