The premise is straightforward: why route capital through Dubai, Singapore, or Mauritius when a globally aligned financial centre sits on Indian soil? Yet many sophisticated investors still treat GIFT City as unfamiliar territory — uncertain about who qualifies, what instruments are available, how the tax framework actually works, and where the genuine risks lie.

This guide covers all four dimensions. By the end, you'll have a clear picture of whether GIFT City belongs in your portfolio and what it takes to get started.

Key Takeaways

- GIFT City accepts NRIs, OCIs, FPIs, and Indian resident investors — open to both residents and non-residents

- All transactions are USD-denominated, removing INR currency risk for NRI investors

- Tax advantages are real but instrument-specific, not a blanket tax-free regime

- Minimum investment for most GIFT City AIFs starts at USD 150,000, making this primarily a UHNI and family office product

- Resident Indians can invest via the LRS route, up to USD 250,000 per financial year

What Is GIFT City and Why Does It Matter Now

GIFT City hosts India's only operational IFSC, regulated by the International Financial Services Centres Authority (IFSCA), established on 27 April 2020 as the unified regulator for all IFSC business in India. Before IFSCA, multiple regulators — RBI, SEBI, IRDAI, and PFRDA — each governed their respective domains within the IFSC, creating friction that a single unified regulator has since resolved.

What Makes It Structurally Different

GIFT City operates as a distinct financial jurisdiction within India, but outside the standard domestic regulatory and tax framework. Three characteristics define it:

- Foreign currency transactions — all banking, fund, and exchange activity is conducted in specified foreign currencies (primarily USD), not INR

- International regulatory standards — IFSCA aligns its oversight with globally accepted frameworks, not domestic Indian norms

- Separate tax and compliance regime — IFSC entities and investors operate under specific Income Tax Act provisions that differ materially from mainstream Indian investing

The goal is to bring offshore financial activity — capital that would otherwise flow through Mauritius, Singapore, or the Cayman Islands — back onto Indian soil under a credible, internationally aligned framework.

Scale That Signals a Maturing Hub

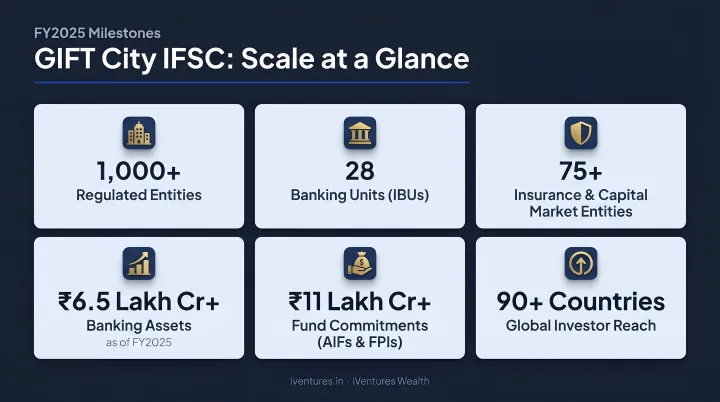

This is no longer a pilot project. According to IFSCA's FY2024-25 Annual Report, as of 31 March 2025:

- 864 entities registered across 35 business segments

- 29 IFSC Banking Units with USD 88.51 billion in banking assets

- 162 Fund Management Entities (FMEs), 229 schemes, and USD 15.74 billion in fund commitments

- Regulated entities facilitated nearly USD 50 billion in inward capital flows, including USD 20 billion in FY2024-25 alone

By March 2026, the IFSCA homepage shows the entity count crossed 1,147 registrations. For investors evaluating where serious cross-border capital is consolidating, that trajectory is hard to ignore.

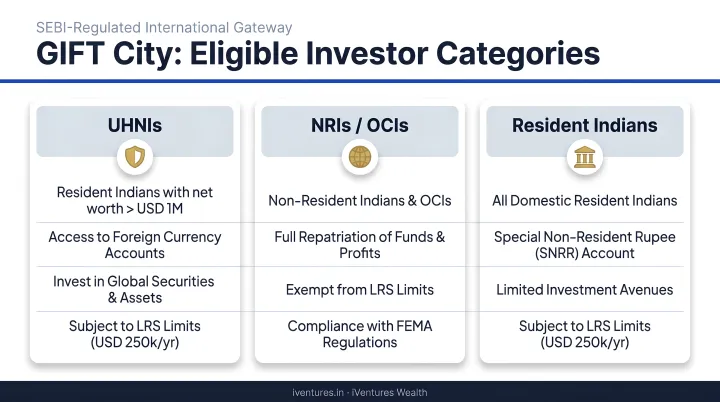

Who Can Invest in GIFT City?

GIFT City is open to a wider range of investors than most people expect — not just non-residents, but domestic institutions, family offices, and resident individuals as well.

Eligible Investor Categories

- NRIs and OCIs — can invest through IFSC-licensed entities using funds remitted from NRE accounts or overseas bank accounts, in foreign currency

- Foreign Portfolio Investors (FPIs) — eligible foreign investors from FATF-compliant jurisdictions participate in IFSC capital markets

- Indian resident individuals — can invest under the Liberalised Remittance Scheme (LRS) up to USD 250,000 per financial year, per RBI's current LRS guidelines

- Domestic institutions and family offices — can access GIFT City fund structures through appropriate regulatory routes

NRI and OCI Specifics

NRIs and OCIs face no major restrictions on repatriation for eligible IFSC investments. A notable regulatory development: a SEBI circular dated 27 June 2024 permits up to 100% aggregate NRI/OCI contribution in IFSC FPIs that are regulated as investment vehicles by IFSCA and meet specified disclosure conditions. The general 25%/50% limits continue to apply to other IFSC FPI structures, so this does not apply universally across all IFSC FPI structures.

Who Is Best Suited

GIFT City is structurally most appropriate for:

- UHNIs and family offices — given minimum investment thresholds of USD 150,000 for most AIF structures

- NRIs seeking India-aligned, USD-denominated investing — those managing wealth across multiple jurisdictions who want India exposure without INR-denominated instruments

- Domestic investors seeking global diversification — resident UHNIs and family offices using the LRS route to access international strategies within India's regulatory framework

That said, GIFT City is not for everyone. The documentation requirements, fund complexity, and minimum ticket sizes make it a poor fit for investors below these thresholds or those without established wealth management infrastructure.

GIFT City Investment Options: What You Can Invest In

GIFT City brings equity funds, alternatives, fixed income, exchange-traded products, and banking under a single USD-denominated regulatory framework — all governed by IFSCA rather than SEBI.

Mutual Funds and GIFT City Funds

Several AMCs have established IFSCA-registered fund entities at GIFT City. DSP Fund Managers IFSC Private Limited holds an IFSCA FME Retail registration; Motilal Oswal Alternative IFSC Private Limited operates GIFT City IFSC fund offerings. These funds:

- Are regulated by IFSCA, not SEBI — a critical distinction for NRI investors

- Can be denominated in multiple currencies, with USD being primary

- Avoid the TDS complications common in domestic mutual fund investing for NRIs

- Offer cleaner repatriation structures compared to INR-denominated domestic funds

Alternative Investment Funds (AIFs)

GIFT City AIFs — operating under IFSCA's Fund Management Regulations 2025 (notified 19 February 2025) — are the primary vehicle for UHNI and sophisticated NRI investors. Key parameters:

| Feature | Detail |

|---|---|

| Standard minimum investment | USD 150,000 |

| Accredited investor threshold | USD 50,000 (where applicable) |

| Category II (PE-style) | Defined lock-in, typically 4–7 years; limited liquidity |

| Category III (active equity) | Greater liquidity; marked-to-market valuations |

| Strategies available | Active listed equity, flexi-cap, secondary PE, mid-market PE |

Selecting the right AIF requires assessing fund-house track record, GP pedigree, fee structures, and lock-in terms against a client's liquidity needs — not just the strategy headline.

IFSC Banking Units and Fixed Income

29 IFSC Banking Units (IBUs) operate within GIFT City, offering:

- Foreign currency term deposits and savings products

- Interest income on deposits that qualifies for non-resident tax benefits under Indian income tax provisions

- Competitive rates compared to offshore banking alternatives

For capital parking alongside equity allocations, IBU deposits offer a useful complement within a GIFT City portfolio.

REITs and InvITs

Beyond fixed income, IFSCA has established a framework for REITs and InvITs to list and trade on IFSC exchanges. Key thresholds: minimum asset value of USD 75 million and a minimum offer size of USD 37.5 million. The framework is in place — but investors should confirm active listings with NSE IX or India INX before committing capital here, as this category is still maturing.

Key Benefits of Investing in GIFT City

Tax Efficiency

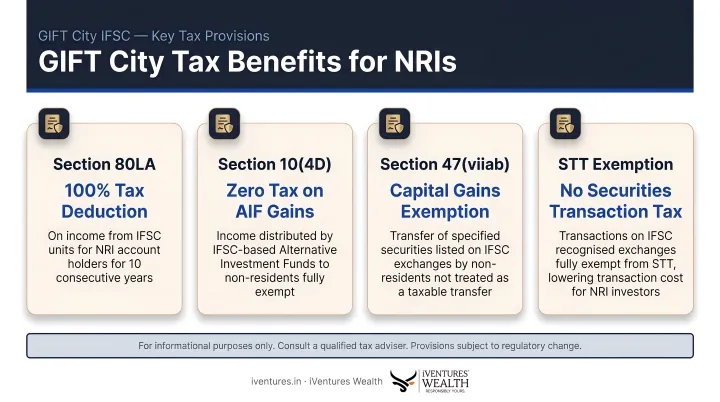

GIFT City's tax framework is instrument-specific — not a blanket exemption — but the advantages are material:

- No STT, CTT, or stamp duty on transactions carried out on IFSC exchanges

- Section 80LA — eligible IFSC units receive a 100% income tax deduction for any 10 consecutive assessment years out of 15

- Section 10(4D) — specified fund income attributable to non-resident unit holders is exempt, subject to conditions

- Section 47(viiab) — capital gains exemption for specified securities transferred by non-residents on recognised IFSC exchanges where consideration is in foreign currency

- Tax-free interest — non-resident interest income on money lent to IFSC units qualifies for exemption under applicable Income Tax provisions

- DTAA applicability — investors in treaty countries can apply Double Taxation Avoidance Agreement relief, though applicability is investor-country and instrument-specific

iVentures Wealth integrates GIFT City tax structuring within its broader DTAA, FEMA, and LRS planning framework — coordinating with external tax counsel in India and overseas where treaty documentation or home-country tax analysis is required.

Currency and Repatriation Advantages

For NRI investors, the USD denomination of GIFT City investments eliminates the INR currency risk that affects returns from domestic Indian funds. Capital and returns from eligible IFSC investments are generally repatriable in foreign currency under applicable FEMA and IFSCA guidelines — without the complex documentation procedures often associated with traditional NRI investment repatriation.

For resident Indian investors accessing GIFT City through LRS, the dynamic works differently. Converting INR to USD introduces currency exposure — gains or losses translate directly into rupee-equivalent return differences. iVentures Wealth addresses this through portfolio construction calibrated for currency exposure, using natural diversification or selective hedging based on each client's portfolio size and outlook.

Global Diversification Without Offshore Complexity

GIFT City provides access to international equities, global bonds, and cross-border strategies without requiring offshore structures in Mauritius, Singapore, or the Cayman Islands. Traditional offshore routes carry risks that GIFT City sidesteps entirely:

- Treaty renegotiation exposure that can unwind existing tax positions

- Blacklisting risk from shifting FATF or OECD classifications

- Multi-regulator compliance demands spanning multiple jurisdictions

GIFT City consolidates all of this within a single, IFSCA-regulated framework — materially reducing structural complexity for both NRI and resident investors.

How to Start Investing in GIFT City: A Practical Roadmap

GIFT City investment follows a structured onboarding process — regulated, mostly digital, and requiring documentation that crosses Indian and international compliance frameworks.

- Identify an IFSCA-licensed entity offering the relevant product — a registered Fund Management Entity, AIF manager, or IFSC Banking Unit

- Complete KYC documentation — passport, overseas or Indian address proof, PAN, Tax Residency Certificate (if applicable), and FEMA-compliant declarations

- Open a foreign currency account with an IFSC Banking Unit or use an NRE/overseas account for fund transfers

- Select the investment product aligned to your risk profile, investment horizon (3–5 years for equity AIFs, 4–7 years for PE structures), and minimum threshold

- Transfer funds in USD and complete onboarding documentation with the fund or platform

Before committing capital, engage a SEBI-registered investment adviser or IFSC-licensed distributor. The product complexity, cross-jurisdictional tax implications, and minimum ticket sizes of USD 150,000 mean unadvised investing here carries real risk.

iVentures Wealth, operating as a fee-only SEBI-registered RIA (INA000019026), provides research-driven, fiduciary-grade guidance on GIFT City fund selection and portfolio construction for UHNIs, NRIs, and family offices. With no placement commissions and a CFA-led open-architecture research process, the firm's guidance remains unconflicted — which matters in a product category where distributor incentives often shape recommendations.

Risks and Important Considerations

Market, Currency, and Liquidity Risks

- GIFT City funds are market-linked — equity AIFs carry standard equity risk; PE structures carry illiquidity and valuation risk

- Category II PE structures typically have lock-in periods of 4–7 years with very limited secondary market exit options

- For resident Indian investors, INR-to-USD conversion introduces currency exposure that can add to or subtract from rupee-equivalent returns

Regulatory and Tax Complexity

- Tax treatment varies by investor category (NRI vs. Indian resident), country of residence, fund type, and income nature (capital gains vs. dividend vs. interest)

- DTAA applicability and home-country tax obligations require case-by-case evaluation — no single framework applies across all fund structures and investor profiles

- IFSCA Fund Management Regulations were updated as recently as February 2025 — LRS rules, FEMA provisions, and tax sections are living regulations, not fixed rules

Suitability and Due Diligence

Given this regulatory and structural complexity, suitability assessment is as important as fund selection. Before committing capital, review:

- The fund manager's track record and strategy clarity

- Fee structure and expense ratios

- Lock-in terms and exit mechanisms

- The fund's compliance standing with IFSCA

- Your own cross-border tax position and home-country reporting obligations

GIFT City structures carry high minimum investments (often $150,000–$1M+), multi-year lock-ins, and significant documentation requirements. They suit investors who have the capital, the patience, and access to qualified advisory — not those looking for liquid or short-term exposure.

Frequently Asked Questions

Can Indian residents invest in GIFT City?

Yes. Indian residents can invest in GIFT City instruments under the Liberalised Remittance Scheme up to USD 250,000 per financial year. This gives domestic UHNIs and family offices access to GIFT City fund structures and USD-denominated strategies that would otherwise require offshore setups.

Is it good to invest in GIFT City?

GIFT City can be a strong option for UHNIs, NRIs, and family offices seeking global diversification, tax efficiency, and USD-denominated returns. Suitability depends on capital size, risk appetite, investment horizon, and cross-border tax position. It is not the right fit for every investor.

What is the minimum investment required for GIFT City funds?

Most GIFT City AIFs require a minimum of USD 150,000. Select funds offer entry from USD 50,000 for accredited investors. IFSCA-registered mutual fund structures within GIFT City may have lower thresholds depending on the AMC.

Are GIFT City investments tax-free for NRIs?

Not entirely, but the advantages are significant: no STT or stamp duty on IFSC exchange transactions, Section 10(4D) exemptions for specified fund income, and tax-free interest on IFSC deposits. NRIs must also factor in home-country tax obligations and DTAA treaty position, so a qualified adviser should assess the full picture before investing.

How is GIFT City different from domestic mutual fund investing in India?

GIFT City funds are USD-denominated, regulated by IFSCA (not SEBI), and exempt from TDS complications that affect NRI investors in domestic funds. They offer offshore-style structures within India's regulatory framework — structurally distinct from INR-denominated domestic mutual funds subject to standard Indian tax and withholding rules.

Can NRIs freely repatriate money from GIFT City investments?

Capital and returns from eligible GIFT City investments are repatriable in foreign currency under applicable FEMA and IFSCA guidelines, with far less friction than traditional NRI repatriation routes. That said, "freely repatriable" should always be verified against specific product terms and FEMA conditions at the time of repatriation.