The confusion deepens with India's dual-regime tax structure. The old regime rewards deductions; the new regime offers lower rates but strips most exemptions away. Many investors aren't sure which instruments actually benefit them under which regime — and some conflate "tax-saving" with "tax-free," which are two very different things.

This article cuts through that confusion. It covers the six best tax-free investment options in India for 2026, explains how the old vs. new regime changes the equation, and offers a practical framework for choosing the right combination based on your income, goals, and risk profile.

Key Takeaways

- EEE status (Exempt-Exempt-Exempt) covers PPF, SSY, and EPF within limits — no tax at contribution, growth, or withdrawal

- ELSS is tax-efficient, not tax-free: gains above ₹1.25 lakh face 12.5% LTCG tax from FY2025–26

- Tax-free bonds and PPF/SSY maturity proceeds stay exempt under both old and new regimes — the most regime-agnostic options available

- Switching to the new tax regime removes Section 80C deductions, which reduces the upfront advantage of PPF, NPS, and SSY

- The right instrument depends on your income slab, investment horizon, liquidity needs, and regime — no single formula applies

What Does "Tax-Free Investment" Actually Mean in India?

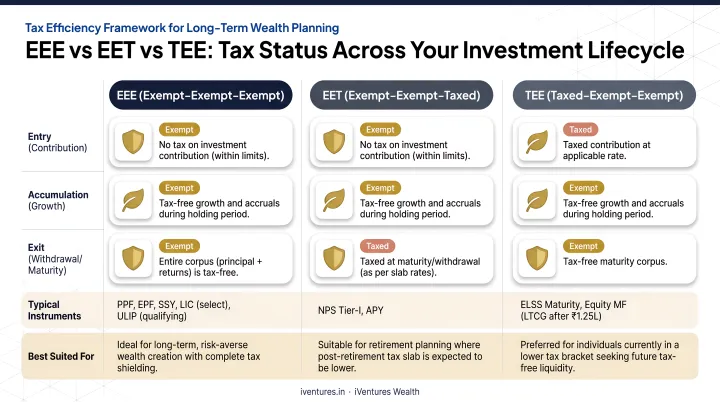

EEE, EET, and TEE — Explained Simply

Indian tax law doesn't use these labels formally — the Act works through specific sections like 80C, 10(11), and 112A. But EEE/EET/TEE are useful shorthand for understanding how an instrument is taxed across its lifecycle:

| Category | What It Means | Examples |

|---|---|---|

| EEE | Contribution deductible, growth tax-free, withdrawal tax-free | PPF (Sections 80C + 10(11)), SSY (Sections 80C + 10(11A)) |

| EET | Contribution and growth exempt, but exit is taxed | ELSS (80C deduction, 12.5% LTCG at redemption via Section 112A) |

| TEE | No upfront deduction, but growth/withdrawal exempt | Tax-free bonds (interest exempt under Section 10(15)(iv)(h)) |

Tax-Saving vs. Tax-Free — A Critical Distinction

Many investors use these terms interchangeably — but they describe fundamentally different outcomes.

- Tax-saving instruments reduce your taxable income at the point of investment (Section 80C deductions). The return may still be taxable.

- Tax-free instruments offer exempt returns — the interest, growth, or maturity proceeds are not added to your income at all.

- The gap between the two shows up at exit, not entry — and for large portfolios, that difference can run into lakhs.

An ELSS investment saves you tax on ₹1.5 lakh today. But when you redeem after three years, gains above ₹1.25 lakh face a 12.5% LTCG tax. A PPF investment saves the same ₹1.5 lakh — and the entire maturity proceeds come back to you completely tax-free.

That gap becomes more consequential as income rises. Under the new tax regime, the 30% slab kicks in above ₹24 lakh — a much higher threshold than the old regime's ₹10 lakh. Which bracket you fall into directly determines which instruments make mathematical sense.

Top 6 Tax-Free Investment Options in India for 2026

These six instruments are selected based on regulatory backing, tax treatment clarity, and suitability across investor profiles — from salaried CXOs to business owners and NRI families.

Public Provident Fund (PPF)

PPF remains one of the cleanest EEE instruments in India. The government-backed structure means zero credit risk, and the sovereign guarantee on returns removes any uncertainty about capital safety.

Key facts:

- Current interest rate: 7.1% per annum (as per DEA/India Post official small savings rate notification — verify the current quarter's notification before acting)

- Contributions qualify for Section 80C deduction under the old regime

- Interest accrues tax-free; maturity proceeds fully exempt under Section 10(11)

- Extendable in 5-year blocks after the initial 15-year term

The 15-year lock-in is the main constraint, but partial withdrawals are permitted from the 7th financial year onwards — useful for managing liquidity without breaking the entire corpus.

| Feature | Details |

|---|---|

| Tax Treatment | EEE (Exempt-Exempt-Exempt) |

| Annual Limit | ₹500 minimum to ₹1.5 lakh maximum |

| Lock-In | 15 years (partial withdrawals from Year 7) |

Equity Linked Savings Scheme (ELSS)

ELSS offers the shortest lock-in among Section 80C instruments — just three years — and equity-level return potential. But calling it "tax-free" is technically incorrect post-Budget 2024.

Under Section 112A (Finance (No. 2) Act, 2024), long-term capital gains above ₹1.25 lakh on equity-oriented funds are taxed at 12.5% for transfers on or after 23 July 2024. This makes ELSS EET in character — the upfront deduction is available, growth compounds without annual tax drag, but redemption gains above the ₹1.25 lakh threshold are taxable.

For investors in the accumulation phase with a 5–10 year horizon, ELSS still deserves consideration — particularly when gains are staggered across financial years to stay within or close to the ₹1.25 lakh exemption threshold. The 80C deduction is only available under the old regime.

| Feature | Details |

|---|---|

| Tax Treatment | EET (LTCG above ₹1.25 lakh taxed at 12.5%) |

| Section 80C Deduction | Up to ₹1.5 lakh (old regime only) |

| Lock-In | 3 years (shortest among 80C instruments) |

Tax-Free Bonds

Tax-free bonds are issued by government-backed entities — NHAI, REC, HUDCO, PFC — and the interest income is fully exempt under Section 10(15)(iv)(h) of the Income Tax Act. No fresh issuances have been announced recently, but existing bonds trade actively on the secondary market (NSE/BSE).

The real advantage shows up for 30% bracket investors. A taxable bond yielding 8% delivers roughly 5.5% post-tax. A tax-free bond at 5.5–6% (current secondary market range varies — check live NSE/BSE data before transacting) matches or exceeds that on a post-tax basis without any credit risk, since these are AAA-rated PSU bonds.

That yield-to-maturity comparison — factoring in duration and cash-flow timing, not just the headline coupon — is precisely how iVentures Wealth's bond advisory team evaluates tax-free PSU bond allocations for HNI clients in higher tax brackets.

| Feature | Details |

|---|---|

| Tax Treatment | Interest fully exempt under Section 10(15)(iv)(h) — both regimes |

| Typical Tenure | 10, 15, or 20 years (existing bonds on secondary market) |

| Minimum Investment | Typically ₹1,000 per bond face value on secondary market |

National Pension System (NPS)

NPS sits in a unique middle ground — not fully EEE, but offering the most generous deduction stack among retirement instruments.

Deduction layers available (old regime):

- Up to ₹1.5 lakh under Section 80CCD(1) — within the overall 80C ceiling

- Additional ₹50,000 under Section 80CCD(1B) — exclusive to NPS, over and above the 80C limit

- Employer contributions deductible under Section 80CCD(2) — available in both regimes (14% of salary for private sector under new regime)

At maturity, 60% of the corpus can be withdrawn tax-free as a lump sum. The remaining 40% must be converted to an annuity — and that annuity income is taxable as per your slab.

Even accounting for the taxable annuity portion, salaried professionals in the 30% bracket under the old regime save ₹15,000+ annually on the ₹50,000 additional deduction alone — worth capturing regardless of what else sits in the retirement portfolio.

| Feature | Details |

|---|---|

| Tax Treatment | Partial EEE: 60% lump sum tax-free; annuity income taxable |

| Additional Deduction | ₹50,000 under Section 80CCD(1B) over and above 80C limit |

| Exit Age | 60 years (partial withdrawal permitted earlier for specific reasons) |

Sukanya Samriddhi Yojana (SSY)

SSY is the highest-yielding small savings scheme in India right now, and it carries full EEE status — contributions qualify for Section 80C deduction under the old regime, interest accrues tax-free, and maturity proceeds are exempt under Section 10(11A).

Key facts:

- Current interest rate: 8.2% per annum (per DEA/India Post official notification — confirm the current quarter)

- Account matures when the girl child turns 21; deposits required for 15 years from opening

- Maximum two accounts per family; girl child must be below age 10 at account opening

For families with daughters, SSY combines goal-based savings (education or marriage) with one of the best guaranteed, tax-free rates available in the Indian market. At 8.2%, the post-tax equivalent yield for a 30% taxpayer works out to approximately 11.7% — a return few fixed-income instruments can match on a like-for-like basis.

| Feature | Details |

|---|---|

| Tax Treatment | EEE (Exempt-Exempt-Exempt) |

| Annual Limit | ₹250 minimum to ₹1.5 lakh maximum (up to 15 years of deposits) |

| Eligibility | Girl child below age 10; maximum 2 accounts per family |

Unit Linked Insurance Plans (ULIPs)

ULIPs offer life cover alongside market-linked investment, with maturity proceeds and death benefits exempt under Section 10(10D) — subject to a critical condition.

For policies issued on or after 1 February 2021, the Section 10(10D) exemption applies only if the annual premium does not exceed ₹2.5 lakh. Policies above this threshold are treated as capital gains — effectively taxed like equity mutual funds with 12.5% LTCG above ₹1.25 lakh under Section 112A logic.

ULIPs also carry a 5-year lock-in under IRDAI regulations. For HNI investors, the honest comparison is net-of-charge ULIP returns versus an ELSS plus term insurance combination. In iVentures Wealth's portfolio consolidation work, clients holding legacy ULIPs have frequently been paying high internal costs for mediocre returns — and restructuring into lower-cost alternatives has delivered materially better net returns.

| Feature | Details |

|---|---|

| Tax Treatment | Maturity exempt under Section 10(10D) if annual premium ≤ ₹2.5 lakh |

| Lock-In | 5 years |

| Key Condition | Annual premium must not exceed ₹2.5 lakh for full tax-free treatment |

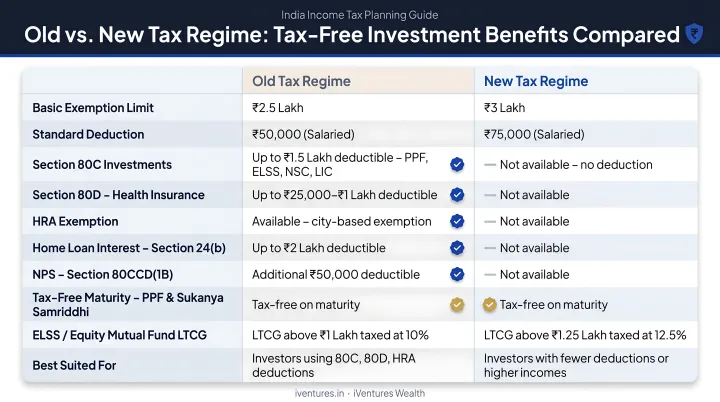

Old Tax Regime vs. New Tax Regime: What Changes for Tax-Free Investing?

The new regime offers lower slab rates but eliminates most deductions — including Section 80C, 80D, HRA, and the employee NPS deduction under 80CCD(1B). Here's what survives and what disappears:

| Benefit | Old Regime | New Regime |

|---|---|---|

| Section 80C deduction (PPF/ELSS/SSY) | ✅ Available (up to ₹1.5 lakh) | ❌ Not available |

| Employee NPS 80CCD(1B) — ₹50,000 | ✅ Available | ❌ Not available |

| Employer NPS 80CCD(2) | ✅ Available | ✅ Available (14% of salary) |

| PPF maturity exemption — Section 10(11) | ✅ Survives | ✅ Survives |

| SSY maturity exemption — Section 10(11A) | ✅ Survives | ✅ Survives |

| Tax-free bond interest — Section 10(15)(iv)(h) | ✅ Survives | ✅ Survives |

| Eligible ULIP maturity — Section 10(10D) | ✅ Survives | ✅ Survives |

The practical takeaway: PPF, SSY, and tax-free bond interest remain exempt in both regimes. The deduction on contributions disappears in the new regime, but the growth and maturity exemptions are preserved. This makes these instruments the most regime-agnostic options for investors who have already switched.

For salaried investors deciding between regimes: if total eligible old-regime deductions exceed roughly ₹8 lakh above the standard deduction (common at higher income levels), the old regime and EEE instruments often make mathematical sense. Below that threshold, the new regime's lower rates may produce a smaller tax bill even without deductions.

No universal break-even applies here. The right answer depends on your specific salary structure, applicable deductions, and which exemptions you can actually claim.

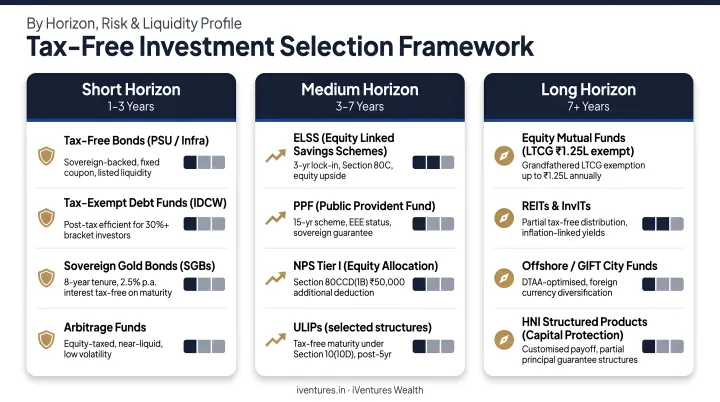

How to Choose the Right Tax-Free Investment for You

Match Instruments to Your Profile

The right choice isn't the instrument with the highest interest rate — it's the one that fits your horizon, liquidity needs, risk appetite, and regime.

By investment horizon:

- Long-term (15+ years): PPF, SSY, NPS

- Medium-term (5–15 years): Tax-free bonds, ULIPs

- Shorter accumulation (3–7 years): ELSS

By risk appetite:

- Capital-safe, guaranteed returns: PPF, SSY, tax-free bonds

- Market-linked with lock-in: ELSS, ULIPs

By liquidity needs:

- Moderate liquidity available: PPF (partial withdrawals from Year 7)

- Locked until maturity/age: SSY (till age 21), NPS (till age 60)

- Tradeable on exchange: Tax-free bonds (secondary market)

For Complex, High-Value Portfolios

For UHNIs, CXOs, and family offices managing multi-crore portfolios, tax-free investing works best when it's integrated into a whole-portfolio strategy — not chosen in isolation for a single deduction.

In practice, that includes:

- Combining EEE instruments with tax-efficient equity holdings

- Calibrating LTCG harvest timing on ELSS to minimize tax drag

- Matching tax-free bond duration to actual cash flow requirements

- Factoring in NRI tax residency and applicable DTAA provisions

iVentures Wealth structures this kind of tax-aware portfolio architecture through its SEBI-registered, fee-only advisory model — where advice is driven by client outcomes, not product commissions.

Conclusion

Genuine tax-free investing in India requires understanding the full lifecycle of each instrument — not just the deduction at entry. The right instruments depend on your income slab, which regime you've chosen, your investment horizon, and your liquidity requirements.

If you're in the 30% bracket, a focused allocation to true EEE instruments like PPF and SSY — combined with tax-free bonds and a regime-aware NPS strategy — can compound returns substantially over a 10–15 year horizon, often saving lakhs in tax drag.

Check whether your existing portfolio holds instruments that looked tax-efficient at entry but carry hidden tax costs at exit. iVentures Wealth's CFA-qualified, SEBI-registered advisory team works with affluent investors to identify exactly those gaps and build portfolios around genuine tax efficiency — with no commissions, no product conflicts, and no one-size-fits-all recommendations.

Frequently Asked Questions

What types of investments are tax-free in India?

Instruments with EEE status — PPF, SSY, and EPF (within the ₹2.5 lakh annual contribution limit) — are tax-free at all three stages. Tax-free bond interest, eligible ULIP maturity proceeds (annual premium ≤ ₹2.5 lakh), and life insurance death benefits are also exempt under specific Income Tax Act provisions. These are tax-free by law, not merely tax-deferred.

How much money can I invest tax-free in India?

PPF and SSY each cap at ₹1.5 lakh per year; NPS adds a separate ₹50,000 deduction under Section 80CCD(1B). Tax-free bonds on the secondary market carry no fixed cap. Note that the combined Section 80C limit is ₹1.5 lakh, so PPF, ELSS, SSY, and employee NPS all compete for that same ceiling.

Can I deposit ₹20 lakh in a bank without tax?

No — bank deposit interest is taxable income. Savings account interest up to ₹10,000 per year is exempt under Section 80TTA for non-senior citizens (₹50,000 for senior citizens under Section 80TTB). Cash deposits aggregating ₹10 lakh or more in savings accounts also trigger mandatory reporting to the Income Tax Department under Statement of Financial Transactions (SFT) rules.

Is PPF still a good investment in 2026 under the new tax regime?

PPF maturity proceeds and interest remain fully tax-free under the new regime, as the Section 10(11) exemption survives. However, the Section 80C deduction on contributions is unavailable in the new regime, so you lose the upfront tax benefit. For new-regime investors, PPF functions best as a capital-preservation and legacy instrument rather than a deduction vehicle.

What is the difference between EEE, EET, and TEE tax status?

These three categories describe when tax applies across the investment lifecycle: EEE (exempt at contribution, growth, and withdrawal) applies to PPF and SSY. EET (exempt on contribution and growth, taxed at exit) fits ELSS, where 12.5% LTCG applies above ₹1.25 lakh. TEE (taxed on contribution, exempt on growth and withdrawal) covers tax-free bonds, where there's no 80C deduction but interest remains fully exempt.