Introduction: The Tax Complexity HNIs in India Can't Afford to Ignore

Earning more in India doesn't just mean paying more tax — it means paying disproportionately more. Under the old tax regime, income exceeding ₹5 crore attracts a 37% surcharge, pushing the effective marginal tax rate to 42.744% (30% base rate × 1.37 surcharge × 1.04 cess). That's not a rounding error — it's a structural penalty for high earners who don't plan ahead.

HNIs face a dual burden: income from multiple sources (equity, rental, business distributions, dividends, foreign assets) compounds an already complex filing picture, while elevated transaction values trigger automatic scrutiny through Statement of Financial Transactions reporting thresholds. That scrutiny doesn't wait for filing season — and neither should your strategy.

The strategies that meaningfully reduce tax liability — regime switching, capital gains timing, trust structuring, DTAA claims — require decisions made months in advance, not days before the due date.

What follows is a practical guide to the frameworks HNIs can act on now: how to choose the right tax regime, time capital gains effectively, structure investments for efficiency, and deploy advanced planning tools before the opportunity closes.

Key Takeaways

- HNIs earning above ₹5 crore face an effective rate of 42.744% under the old regime — making strategy, not compliance, the real priority

- The old vs. new regime decision must be re-evaluated every financial year based on deductions, income mix, and surcharge exposure

- Family trusts, HUF structures, and DTAA claims can significantly cut family-level tax outgo — but only with deliberate structuring

- Capital gains timing, tax-loss harvesting, and Sections 54/54F/54EC reinvestment are among the highest-impact levers for HNI tax reduction

Why HNI Tax Planning in India Demands a Different Approach

Who Qualifies as an HNI and What Makes Their Tax Profile Complex

In the Indian wealth management context, HNIs typically hold investable assets above ₹5 crore. Their income profiles rarely resemble a salaried employee's: distributions from business entities, equity capital gains, rental income across multiple properties, dividend receipts, and income from overseas investments or employment.

This diversity creates both opportunity and exposure. Each income stream carries its own tax treatment, and the aggregate picture — across multiple PANs, HUFs, partnership firms, and family trusts — can be genuinely difficult to manage without a structured approach.

iVentures Wealth addresses this fragmentation directly. Tax data spread across spreadsheets, PDFs, and multiple entity statements is consolidated into clean, standardised reports for each PAN, reducing filing errors and the weeks of back-and-forth that typically precede the ITR deadline.

Why Proactive Management Matters More at This Wealth Level

Three structural realities separate HNI tax planning from standard filing:

- Elevated scrutiny thresholds: Property transactions above ₹30 lakh, cash deposits above ₹10 lakh in savings accounts, and equity or mutual fund acquisitions above ₹10 lakh trigger automatic reporting to the Income Tax Department via SFT

- Multiple entity complexity: Income from LLPs, private limited companies, partnership firms, and family trusts creates interdependencies that must be managed at the family level, not per individual

- Year-round deadlines: Major tax-saving actions — 54EC bond investments (within 6 months of asset sale), NPS contributions, trust formations — have fixed windows that can't be addressed retroactively

Old vs. New Tax Regime: The HNI Decision Framework

For HNIs, the choice between the old and new tax regime is often the single largest tax decision of the year — and it deserves that weight.

Structural Differences That Matter at High Income

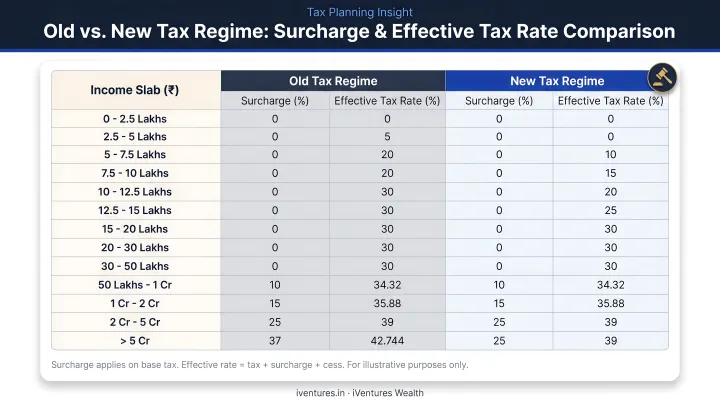

The new regime (Section 115BAC) caps surcharge at 25% for income above ₹2 crore. The 37% surcharge that applies in the old regime for income above ₹5 crore simply does not exist under the new structure. For UHNIs, this differential alone can be decisive.

The old regime allows deductions that, for the right income profile, substantially reduce taxable income:

- Section 80C/80CCC/80CCD(1): Up to ₹1.5 lakh aggregate

- Section 80CCD(1B): Additional ₹50,000 NPS deduction above the 80C ceiling

- Section 80D: Health insurance premiums

- Home loan interest (self-occupied and let-out property)

- HRA exemption for those in rented accommodation

The new regime eliminates most of these but offers lower slab rates and removes the surcharge cliff at ₹5 crore.

Surcharge and Effective Tax Rate Comparison

| Income Level | Old Regime Surcharge | New Regime Surcharge | Old Regime ETR (Approx.) | New Regime ETR (Approx.) |

|---|---|---|---|---|

| ₹50L – ₹1 crore | 10% | 10% | ~34.32% | ~31.20% |

| ₹1 crore – ₹2 crore | 15% | 15% | ~35.88% | ~33.99% |

| ₹2 crore – ₹5 crore | 25% | 25% | ~39.00% | ~35.88% |

| Above ₹5 crore | 37% | 25% (capped) | ~42.74% | ~39.00% |

Note: Surcharge on LTCG and STCG from listed equity and equity-oriented mutual funds is capped at 15% in both regimes. Dividend income surcharge is also capped at 15%. New regime ETR figures are approximate and assume no deductions claimed.

When Each Regime Wins

Old regime suits HNIs who:

- Have substantial 80C-eligible investments, insurance premiums, and home loan interest

- Use NPS actively (the extra ₹50,000 under 80CCD(1B) remains valuable)

- Hold HRA-eligible rental arrangements

- Have total income in the ₹2–5 crore range where deductions can offset the surcharge disadvantage

New regime suits HNIs who:

- Earn above ₹5 crore and lack sufficient deductions to offset the 37% surcharge

- Prefer predictability over complex exemption management

- Have simple income structures (primarily equity gains or salary)

The strategic choice above carries procedural consequences that business income earners cannot afford to overlook.

Taxpayers with business or professional income who switch to the old regime must file Form 10-IEA by the Section 139(1) due date. Once they revert to the new regime, the old regime is permanently unavailable to them. This irreversibility makes it critical to model both regimes at the start of each financial year — before any structural changes are locked in.

Proven Tax Optimisation Strategies for HNIs in India

Capital Gains Tax Management

Capital gains represent one of the most significant and most controllable components of an HNI's annual tax bill.

Key rates for AY 2025-26:

- LTCG on listed equity and equity mutual funds (held 12+ months): 12.5%, with a ₹1.25 lakh annual exemption threshold

- STCG on listed equity and equity mutual funds: 20%

- LTCG on real estate (held 24+ months): 12.5% without indexation, with an option for resident individuals to choose 20% with indexation for properties acquired before July 23, 2024

The gap between LTCG and STCG rates — 12.5% vs. 20% on equity — makes holding period management a concrete tax-saving exercise, not just portfolio theory.

Tax-loss harvesting works in the Indian context as follows: short-term capital losses can be set off against both short-term and long-term gains; long-term losses can only offset long-term gains. Unused losses carry forward for up to 8 assessment years. HNIs with diversified portfolios typically carry positions with unrealised losses that can be harvested to offset gains from other realisations in the same year.

Reinvestment exemptions remain among the most valuable provisions available:

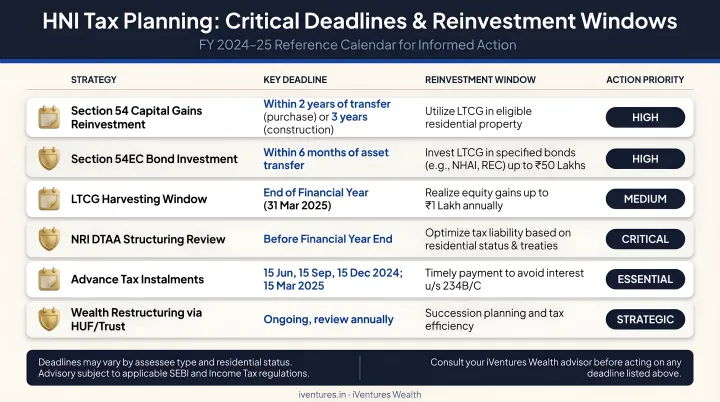

- Section 54: Reinvest LTCG from residential property into another residential property (purchase within 1 year before or 2 years after, or construct within 3 years)

- Section 54F: Reinvest LTCG from any long-term capital asset into a residential house — subject to the condition that the investor does not own more than one other house at the time of transfer

- Section 54EC: Invest up to ₹50 lakh in specified government bonds (REC, PFC, NHAI, IRFC) within 6 months of the asset sale — bonds are locked in for 5 years

For clients following property transactions, iVentures Wealth advises on 54EC bond investments — including access to AAA-rated PSU issuers and structuring the 6-month reinvestment window correctly.

Tax-Efficient Investment Structuring

The post-April 2023 amendment to debt mutual fund taxation changed the calculus for HNI fixed-income portfolios. Under Section 50AA, gains from funds where less than 35% of proceeds are invested in domestic equity shares are now treated as short-term capital gains and taxed at slab rate — regardless of holding period.

For an HNI at the 30% slab plus surcharge, this significantly cuts the after-tax appeal of traditional debt funds.

Portfolio construction implications:

- Equity mutual funds and listed equity: Still eligible for LTCG at 12.5% after 12 months — tax-efficient for long-term wealth compounding

- Tax-free bonds (picked up in secondary markets): Interest is exempt under Section 10(15)(iv)(h) — useful for HNIs seeking tax-free income at higher tax brackets

- NPS: Section 80CCD(1B) provides ₹50,000 in additional deduction over the 80C ceiling — and remains accessible only under the old regime

- Private credit AIFs: iVentures Wealth's HNI clients have increasingly shifted toward senior secured private credit AIFs offering 13–16% gross returns with LTCG-eligible tax treatment — a structurally superior alternative to debt funds now taxed at slab rate

For HNIs in higher surcharge brackets, the difference between pre-tax and after-tax yield can exceed 10 percentage points — making asset selection, not just asset allocation, the core of tax-efficient portfolio construction.

Gifting Strategies and Clubbing Rules

Beyond portfolio structuring, strategic intergenerational transfers can reduce the family-level tax burden — provided the clubbing rules are understood and respected.

What's exempt: Gifts from specified relatives — spouse, siblings, parents, lineal ascendants and descendants, and their spouses — are fully exempt from tax under Section 56(2)(x). Gifts from non-relatives are taxable if the aggregate value exceeds ₹50,000 in a financial year.

What to watch — Section 64 clubbing provisions:

- Income from assets transferred to a spouse is clubbed back to the transferor's income — rental income and interest from such gifts are taxed in the donor's hands

- Income from assets gifted to a minor child follows the same clubbing treatment

- Adult children are not subject to automatic clubbing, making them a cleaner vehicle for intergenerational wealth transfer where the amounts and tax context support it

Advanced Planning Tools: Trusts, HUF Structures, and DTAA

Trust Structures for Wealth Protection and Tax Efficiency

Private family trusts allow HNI families to hold investments, real estate, and business interests in a single structure, with income distributed among beneficiaries who may be in lower tax brackets, reducing the family's combined tax outgo while maintaining asset protection.

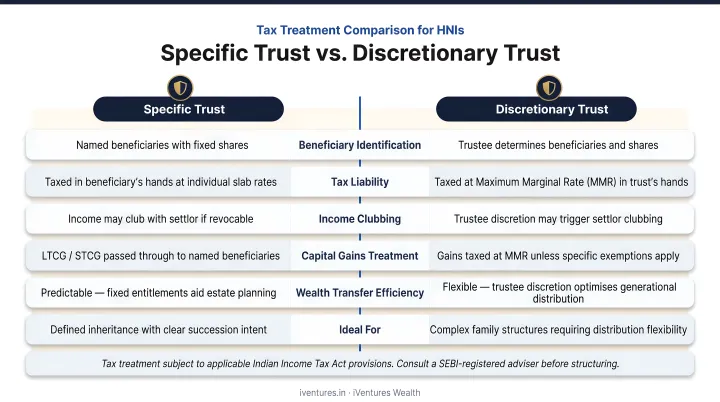

Two tax considerations are critical:

- Specific/determinate trusts (where beneficiary shares are fixed) are taxed in the hands of the beneficiaries under Section 161 — enabling income splitting across family members

- Discretionary/indeterminate trusts (where shares are unknown or the trustee decides) are taxed at the maximum marginal rate under Section 164, removing most tax efficiency unless statutory exceptions apply

The succession benefits are equally significant. iVentures Wealth has structured family trusts for first-generation promoters following large business exits — ring-fencing the corpus, formalising distribution rules for spouses and children, and establishing cross-border succession clarity.

In one such case, the restructured trust reduced inheritance-related tax exposure by over ₹2 crore while ensuring seamless wealth transfer across generations.

iVentures coordinates with senior legal counsel, including Supreme Court-level practitioners, for trust formation and documentation, ensuring structures are both tax-efficient and legally sound.

HUF: A Legally Distinct Tax Entity

While trusts operate at the family corpus level, an HUF works differently — as a fully separate taxpayer in the eyes of Indian tax law. A Hindu Undivided Family has its own PAN, its own basic exemption limit (₹2.5 lakh under the old regime for AY 2025-26), and its own entitlement to Chapter VI-A deductions including Sections 80C and 80D.

In practical terms, an HNI family can use an HUF to:

- Hold investments and earn income taxed independently of individual members

- Claim deductions separately from the individual's own 80C and 80D limits

- Split income across the individual and HUF tax structures, reducing aggregate tax liability

Note: HUF formation applies to Hindus, Buddhists, Jains, and Sikhs under the Hindu Succession Act — it is not available to Muslims, Christians, Parsis, or Jews.

Documentation is critical. Incorrect setup, particularly around the source of HUF assets and the distinction between individual and HUF income, can trigger clubbing disputes or compliance issues during scrutiny.

DTAA Benefits for NRIs and HNIs with Global Income

India has comprehensive double taxation avoidance agreements with 95 countries, allowing HNIs and NRIs with foreign income to claim credit in India for taxes paid abroad, preventing the same income from being taxed twice.

Common scenarios iVentures Wealth advises on:

- US/UK dividends attracting withholding tax (for example, 25% in the US), claimable as foreign tax credit in India via Form 67

- Overseas capital gains where treaty provisions may reduce or eliminate Indian tax liability

- NRO/NRE/FCNR account income, property sale proceeds, and mutual fund redemptions requiring TDS management and Form 15CA/15CB compliance

Residency tracking is non-negotiable for global HNIs. Under current rules, an Indian citizen or person of Indian origin visiting India is considered resident if their stay exceeds 120 days in a financial year where India-sourced income exceeds ₹15 lakh. Below that threshold, the standard 182-day rule applies.

A separate "deemed resident" provision applies to Indian citizens not liable to tax in any country by reason of domicile or residence. For HNIs with global mobility, this makes inadvertent Indian tax residency a genuine risk — one that requires proactive tracking, not reactive damage control.

Common Tax Planning Mistakes HNIs Make (and How to Avoid Them)

1. Defaulting to the same regime year after year

Income mix changes — a business exit, a large property sale, or a shift in salary structure can swing the optimal regime decisively. Run a comparison simulation at the start of each financial year before any investment or filing decisions are made.

2. Inadequate disclosure of high-value transactions and foreign assets

Undisclosed foreign assets carry severe consequences. The Black Money Act imposes tax at 30% plus a penalty equal to three times the tax payable — effectively 90% of the undisclosed amount. Under Section 270A, under-reporting attracts a 50% penalty on tax due; misreporting triggers 200%.

Foreign assets must be declared in Schedule FA. ITR-1 and ITR-4 do not contain this schedule, so HNIs with overseas holdings must file the correct ITR form or risk non-compliance penalties on top of the underlying tax.

3. Last-minute planning that misses critical windows

| Strategy | Deadline |

|---|---|

| 54EC bond investment | Within 6 months of asset sale |

| NPS contributions (old regime) | Before March 31 of the financial year |

| Section 54/54F reinvestment | 2 years after transfer (purchase) or 3 years (construction) |

| Form 67 for foreign tax credit | Within due date of ITR filing |

Missing any of these windows forfeits the benefit entirely — there is no catch-up provision. Engaging a SEBI-registered advisor at the start of the financial year, rather than scrambling in February or March, is the most reliable way to keep every deadline in view. iVentures Wealth integrates tax optimisation planning within its wealth management mandates so these deadlines are tracked and acted on throughout the year, not flagged as an afterthought at filing time.

Frequently Asked Questions

What is the best tax strategy for high-net-worth individuals?

The most effective approach combines regime optimisation, capital gains timing, tax-efficient investment selection, and advanced structures like trusts or HUF — calibrated annually to the individual's income mix, deductions, and financial goals.

What are the 5 D's of tax planning?

The five D's are: Deduct (maximise legitimate deductions), Defer (delay tax through reinvestment or retirement vehicles), Divide (split income across family members or entities), Diminish (reduce taxable income through exemptions), and Dodge (legally restructure income into lower-taxed categories).

Which tax regime is better for HNIs in India — old or new?

HNIs with significant deductions (investments, insurance, housing loan, NPS) often benefit from the old regime. Those earning above ₹5 crore with limited deductions frequently find the new regime's 25% surcharge cap more advantageous. An annual comparison before the financial year starts is advisable.

How can HNIs reduce capital gains tax in India?

Key strategies include holding assets for 12+ months (equity) or 24+ months (property) to qualify for LTCG rates, reinvesting under Sections 54/54F/54EC, harvesting losses to offset gains, and timing asset sales across financial years to manage aggregate taxable income.

What is the surcharge applicable to HNIs in India?

Under the old regime, surcharge reaches 37% for income above ₹5 crore, producing an effective marginal rate of 42.744%. The new regime caps surcharge at 25% for income above ₹2 crore. Surcharge on LTCG and STCG from listed equity is capped at 15% in both regimes.

How do trust structures and HUF help in tax planning for HNIs?

Trusts allow income to be distributed among beneficiaries in lower tax brackets while protecting assets across generations. HUF is taxed as a separate entity with its own exemption limits and deductions — both are legitimate, widely used tools for reducing combined family tax liability in India.