The market is crowded with mutual fund distributors, insurance agents, stock brokers, and self-styled "wealth managers"—many of whom earn commissions on the products they recommend to you. For affluent investors managing ₹5 Cr or more, the cost of choosing the wrong advisor isn't just a suboptimal return. It's mis-sold products, commission-driven portfolios, and financial goals that quietly never get met.

The right advisor, by contrast, can be a generational wealth-building partner. Someone who structures your exit from a business, manages your NRI compliance across three countries, and helps your children inherit a plan rather than a problem.

This guide gives you a practical, India-specific framework for evaluating and selecting a financial advisor—what credentials to verify, how fee structures work, what red flags look like, and what questions to ask before you sign anything.

Key Takeaways

- SEBI-Registered Investment Advisers (RIAs) are legally bound to act as fiduciaries; distributors and brokers are not.

- Define your goals first—retirement, wealth creation, succession, NRI repatriation—before shortlisting any advisor.

- Verify SEBI registration directly on SEBI's intermediary portal before any money changes hands.

- A good advisor listens before recommending—treat the first meeting as a two-way interview.

- Annual reviews of the advisor relationship itself matter as much as portfolio reviews—this is a long-term partnership.

What Is a Financial Advisor and What Can They Help You With?

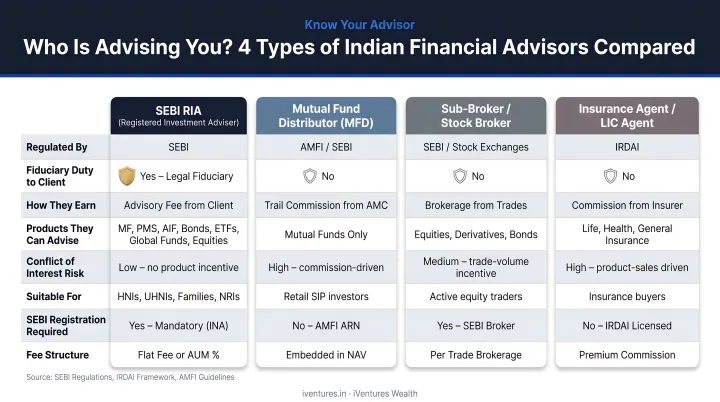

In the Indian context, "financial advisor" is not a protected term. Almost anyone can use it. What actually matters is the regulatory category a professional falls under: that determines who they legally work for — you, or the product manufacturer.

Types of Financial Advisors in India

| Type | Registered With | How They Earn | Fiduciary? |

|---|---|---|---|

| SEBI-Registered Investment Adviser (RIA) | SEBI | Fees paid by client only | Yes (Regulation 15(1)) |

| Mutual Fund Distributor (MFD) | AMFI | Trail commissions from fund houses | No |

| Stock Broker | NSE/BSE/SEBI | Brokerage and transaction fees | No |

| Certified Financial Planner (CFP) | FPSB India | Varies (can be fee or commission) | Depends on structure |

SEBI's Investment Advisers Regulations, 2013 (last amended December 2024) require any person charging fees for investment advice to hold SEBI RIA registration under Regulation 3(1). This is the single clearest legal line between an advisor and a salesperson.

What Financial Advisors Typically Help With

Knowing what you need before you start looking saves weeks of misdirected conversations — and narrows the field considerably.

Core service areas include:

- Portfolio construction across equities, debt, mutual funds, PMS, and AIFs

- Goal-based and retirement planning with specific corpus targets and timelines

- Tax optimisation for founders with ESOPs, NRIs with dual-jurisdiction income, and promoters post-exit

- Estate and succession planning — trust structuring, will drafting, family governance

- NRI/OCI cross-border advisory covering FEMA compliance, DTAA structuring, and repatriation

- Family office services including consolidated reporting and personal CFO functions

Mapping your needs to the right advisor type is, in practice, the first decision in this process — everything else follows from it.

How to Choose a Financial Advisor: A Step-by-Step Guide

Step 1: Define Your Financial Goals and the Kind of Help You Need

Before reaching out to anyone, write down your top three to five financial priorities. Be specific.

Examples by life stage:

- A 38-year-old founder approaching a liquidity event needs ESOP exercise-timing advice, tax structuring, and a deployment plan for ₹50–100 Cr in a short window.

- A 55-year-old CXO needs succession planning, retirement corpus modelling, and possibly estate structuring for children in different cities or countries.

- An NRI returning to India needs FEMA compliance, NRE/NRO account restructuring, and a rebalanced India-global portfolio.

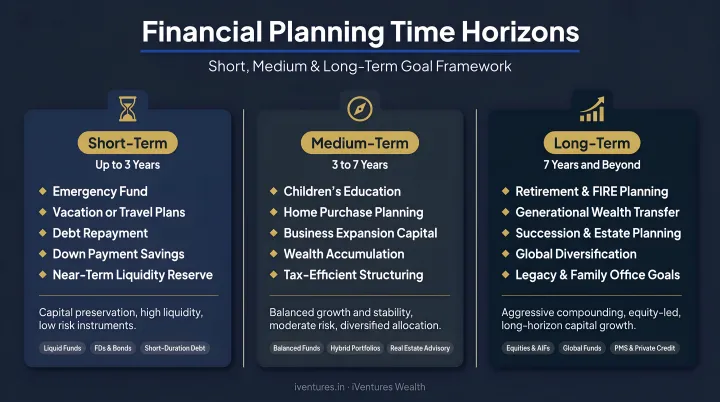

Think across three horizons:

- Short-term (0–3 years): Liquidity needs, near-term goals, debt obligations

- Medium-term (5–10 years): Education funding, property, business transition

- Long-term (20+ years): Retirement, legacy, generational transfer

The clearer you are about your needs, the faster you'll identify whether a shortlisted advisor actually has the depth to help—or just the confidence to sound like they do.

Step 2: Verify SEBI Registration and Relevant Credentials

This step takes less than ten minutes and is the single most important filter in the Indian market.

The critical distinction: Under Regulation 15(1) of the SEBI Investment Advisers Regulations, SEBI-RIAs are legally obligated to act as fiduciaries. They cannot receive commissions, trail income, or referral payments from product manufacturers. Mutual fund distributors and brokers operate under no such obligation—they are compensated by the products they sell.

Verification sources:

- SEBI RIA registration → SEBI Intermediary Portal or SEBI Investment Adviser list

- CFA Charterholder status → CFA Institute Member Directory

- CFP certification → FPSB India CFP Directory

- Complaints or regulatory actions → SEBI SCORES portal

Ask directly: "Are you a SEBI-registered RIA? What is your registration number?" Any legitimate advisor will provide this immediately.

As of June 2026, SEBI's recognised intermediaries data shows only 1,039 registered Investment Advisers across India. That scarcity is itself informative—the overwhelming majority of people calling themselves financial advisors are not SEBI-registered RIAs.

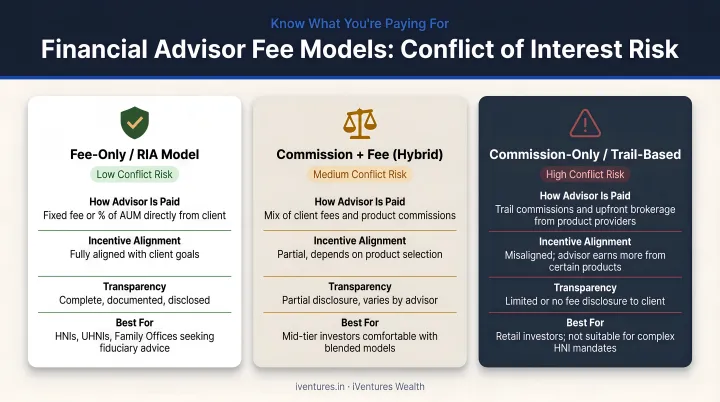

Step 3: Understand the Fee Structure and Potential Conflicts of Interest

How an advisor earns money shapes every recommendation they make. There are three models in the Indian market:

| Fee Model | How It Works | Conflict Risk |

|---|---|---|

| Fee-only | Flat fee, AUM percentage, or hourly — paid by client | Low |

| Commission-based | Earns trail commissions from fund houses or insurers | High |

| Fee-and-commission hybrid | Combination of both | Moderate to high |

SEBI mandates that RIAs operate on a fee-only basis, making them structurally conflict-free. The 2020 SEBI IA Amendments explicitly require segregation between advisory and distribution activities. An advisor cannot hold both roles simultaneously.

SEBI guidelines cap AUA-based fees at 2.5% of assets under advisory per annum, providing a ceiling for what fee-only RIAs can charge.

Questions to ask every advisor:

- What is your total fee, and how is it calculated?

- Do you earn any trail commissions, referral income, or placement fees?

- Will you provide a written fee disclosure before we engage?

A transparent advisor welcomes these questions. One who deflects them is likely earning money from sources they'd prefer you not examine.

Step 4: Evaluate Track Record, Experience, and Client Specialisation

An advisor who primarily serves salaried individuals in the ₹50–75 lakh income bracket may not be equipped to manage the complexity of a UHNI's multi-entity portfolio or a founder's ₹100 Cr+ liquidity event. Specialisation matters enormously at higher wealth levels.

What to assess:

- Years in practice and AUM managed

- The profile of their typical client—is it comparable to your situation?

- Whether they can provide anonymised case studies relevant to your needs

- Depth in specific domains: NRI advisory, family office structuring, founder liquidity, business exit planning

A founder who has just exited a majority stake, for instance, needs an advisor with documented experience structuring multi-crore deployments: safety-stability-growth frameworks, family trust setup, and liquidity event tax planning. Generic portfolio advice won't cut it at that level of complexity.

Step 5: Assess Communication Style, Accessibility, and Long-Term Fit

Beyond credentials, the advisory relationship requires genuine compatibility. You'll be sharing your financial anxieties, family dynamics, and long-term intentions with this person. That demands trust.

Use the first consultation as a two-way interview. A good advisor will ask about your values, risk tolerance, life stage, and goals before recommending anything. If someone starts pitching products in the first meeting, that's a signal.

Practical questions on fit:

- How often will we communicate, and through what channels?

- Will I have a dedicated advisor, or be managed by a rotating team?

- Do you offer real-time portfolio visibility (app, consolidated dashboard)?

- How do you communicate during market downturns: reactively or proactively?

The best advisors reach out before clients panic, not after. They share specific analysis and deployment guidance during volatility, not generic reassurance.

Red Flags to Watch Out For When Selecting a Financial Advisor

Investor complaints in India's advisory market are rising sharply. According to a report citing SEBI's Annual Report 2024–25, 68,132 complaints were filed on the SCORES platform in FY2024–25, with nearly 38% directed at stock brokers.

SEBI has also taken direct enforcement action against unregistered advisors — including a 2025 order against Lifeinspire Knowledge Solutions for operating without RIA registration. Knowing what to screen for can protect you from similar situations.

Disqualify immediately if an advisor:

- Pushes specific products (ULIPs, structured notes, particular fund schemes) in the first meeting before understanding your goals

- Cannot produce a SEBI RIA registration certificate when asked

- Claims to offer "advisory services" without formal RIA registration

- Guarantees returns or promises market-beating performance — SEBI explicitly prohibits this

- Provides no written engagement letter, fee agreement, or investment policy statement — every legitimate advisory relationship begins with signed paperwork

- Rushes you to decide — that urgency serves the advisor, not you; a trustworthy advisor welcomes a second opinion

Why iVentures Wealth Is Built for the Discerning Indian Investor

iVentures Wealth is a SEBI-Registered Investment Adviser (INA000019026) with 20+ years of experience and ₹1,200+ Cr in assets under management. The firm serves 150+ affluent families, UHNIs, CEOs, CXOs, NRIs, family offices, and corporates across India — each criterion in this guide maps directly to how the firm operates.

How iVentures maps to the selection criteria in this guide:

- Fee-only model — No commissions, trail income, or placement fees from product manufacturers. All fees are disclosed in writing before engagement, as required under SEBI's Investment Advisers Regulations.

- Research led by a CFA Charterholder — Krishna Makhariya (Head of Research, Executive Director) brings structured equity research and macro analysis to every portfolio decision.

- Fiduciary since 2010 — SEBI-registered from 2010, with a founding principle that wealth management is a partnership, not a transaction.

- Specialised client depth — founders navigating liquidity events, NRIs with cross-border tax complexity, and family offices requiring multi-entity governance each receive dedicated advisory. Minimum thresholds (₹5 Cr for NRIs, ₹10 Cr for professionals, ₹50 Cr for corporates) keep the client-to-advisor ratio low.

- Proactive communication — quarterly portfolio reviews as standard, real-time monitoring between reviews, and structured outreach during periods of market volatility.

- Wealth Monitor App (launched 2020) — consolidated portfolio views across mutual funds, equities, bonds, PMS, AIFs, and FDs, with unified dashboards, CAGR tracking, and family-level access.

Whether you're reassessing an existing advisor or starting from scratch, schedule an initial consultation with iVentures Wealth to see what conflict-free advisory looks like in practice.

Conclusion

The right financial advisor compounds value over decades—across market cycles, liquidity events, succession, and legacy planning. The wrong one doesn't just cost returns. It costs years of misaligned strategy that takes time to unwind.

That's why the process doesn't end at onboarding. Verify credentials before you engage. Review the relationship annually. Ask the hard questions about fees, conflicts, and communication—not just once, but consistently. Advisors who operate with genuine transparency will always welcome that scrutiny. Those who resist it have already given you your answer.

Frequently Asked Questions

What is the average cost of a financial advisor in India?

SEBI-registered RIAs typically charge an AUA-based fee capped at 2.5% of assets under advisory per annum, or a fixed annual fee (capped under SEBI guidelines). Commission-based distributors may appear free but earn embedded trail commissions from fund houses—which can create conflicts. Always ask for a full written fee disclosure before engaging.

How do you choose a financial advisor?

Five steps guide the process: define your goals, verify SEBI RIA registration, understand the fee structure and conflicts of interest, evaluate track record and client specialisation, and assess communication fit. In India, SEBI RIA registration is the single most important first filter.

What are the 3 C's of selecting a financial advisor?

The three C's break down as: Credentials (qualifications and regulatory registration, such as SEBI RIA, CFA, CFP), Compensation (how the advisor is paid and whether it creates conflicts), and Communication (clarity, accessibility, and listening skills).

What is the difference between a SEBI-registered investment adviser and a mutual fund distributor?

A SEBI-RIA is legally obligated to act as a fiduciary—they charge the client directly and cannot earn product commissions. A mutual fund distributor earns trail commissions from fund houses, which may influence product recommendations. SEBI mandates these two roles remain separate and cannot be combined by the same entity.

What should I prepare for my first meeting with a financial advisor?

Bring (or share digitally): current investment statements, monthly income and expenses, outstanding liabilities, and a written list of your top financial goals. Also prepare five to seven questions covering the advisor's fee model, investment philosophy, and communication frequency.

How do I verify if a financial advisor is legitimate in India?

Check their SEBI registration number on the SEBI Intermediary Portal. Verify CFA credentials through the CFA Institute and CFP status via FPSB India. Search for complaints or regulatory actions on SEBI's SCORES portal. This takes under ten minutes and should be done before signing any agreement.