That said, the process is not simply "open an account and invest." Specific account types, KYC documentation, tax deductions, and country-of-residence restrictions all shape how and where you can invest. Getting these details right before you start saves considerable compliance headaches later.

Key Takeaways

- NRIs, OCIs, and PIOs can invest in Indian mutual funds; investments must route through NRE or NRO bank accounts

- PAN card and KYC (passport, overseas address proof, photograph) are mandatory prerequisites

- AMCs deduct TDS at source, so no separate tax remittance is required from the investor

- DTAA relief is available to avoid double taxation — claim it by submitting a Tax Residency Certificate to your AMC

- US and Canada-based NRIs must meet FATCA compliance rules and can only invest through a limited set of eligible AMCs

Are NRIs Eligible to Invest in Indian Mutual Funds?

Who Qualifies Under FEMA and Income Tax Rules

FEMA governs where an NRI can invest and how money moves. The Income Tax Act governs how those investments are taxed — two frameworks, two distinct purposes.

For income tax purposes, the Income Tax Department's guidance for AY 2026-27 defines NRI status using the 182-day rule — an individual present in India for 182 or more days in a financial year is a tax resident. For Indian citizens or PIOs whose total Indian-source income exceeds ₹15 lakh, the threshold substitutes to 120 days.

OCIs and PIOs qualify alongside NRIs and can invest in Indian mutual funds under the same framework, subject to scheme-specific conditions.

What Indian Regulations Say About NRI Participation

SEBI's mutual fund FAQ confirms that non-resident Indians can invest in mutual funds, with specifics appearing in each scheme's offer document. No special RBI approval is required for NRI/PIO mutual fund investments.

Two operational rules apply across all AMCs:

- Investments must be made in Indian rupees — not directly in foreign currency

- Funds must be routed through a designated NRI bank account (NRE or NRO)

What You Need Before You Start Investing

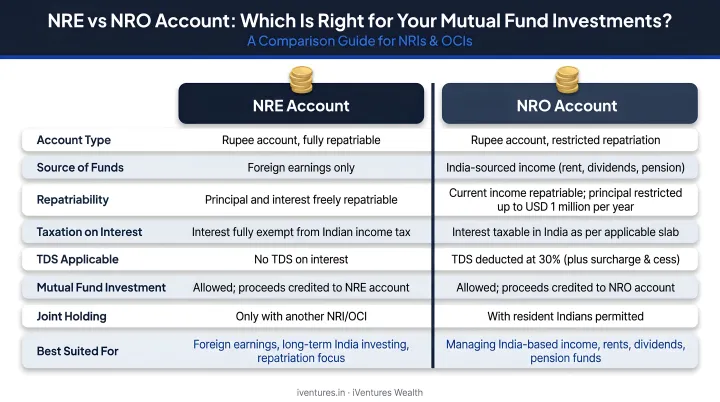

NRE or NRO Bank Account: Choosing the Right One

The account type you choose has direct implications for taxation and repatriation. Here's the practical difference:

| Feature | NRE Account | NRO Account |

|---|---|---|

| Purpose | Foreign earnings remitted to India | Indian-source income (rent, dividends, pension) |

| Interest tax in India | Tax-free | Taxable |

| Repatriation | Fully repatriable | Capped at USD 1 million per financial year |

| Best for mutual funds | Investing foreign income, intent to repatriate gains | Managing India-earned income |

Per RBI's master circular on non-resident accounts, NRE balances are freely repatriable, while NRO repatriation is subject to the USD 1 million annual cap and applicable conditions.

Practical guidance: If you're investing foreign earnings and want the flexibility to transfer gains abroad, use your NRE account. If your funds originate from Indian income sources, route through NRO.

Once your account is in place, two documentation prerequisites unlock access to every mutual fund in India.

PAN Card and KYC: One-Time Prerequisites

A PAN card is compulsory for all mutual fund investments. NRIs who don't already hold one can apply online. Without a valid PAN, the Income Tax Act applies higher TDS rates under Section 206AA.

KYC is a one-time submission through a SEBI-registered KRA (such as CAMS or CDSL) that covers all AMC investments — no repetition per fund house. AMFI's KYC document checklist for NRIs requires:

- Copy of passport (photo and address pages)

- Overseas address proof

- PAN card copy

- Recent passport-size photograph

- PIO/OCI card where applicable

For in-person verification (IPV) abroad: AMFI permits attestation by authorized officials of Indian bank overseas branches, a Notary Public, Court Magistrate, Judge, or the Indian Embassy/Consulate in your country of residence. Many AMCs also accept digital or video KYC.

How NRIs Can Invest in Mutual Funds: Step-by-Step

Step 1: Open an NRE or NRO Account

After acquiring NRI status, you cannot continue using a resident savings account for investment transactions — this is a FEMA requirement. Open the appropriate account based on your income source and repatriation intent. This becomes the channel for all mutual fund transactions.

Step 2: Obtain PAN and Complete KYC

Apply for PAN if you don't already hold one. Submit KYC documents to any SEBI-registered intermediary — a bank, broker, or AMC directly. Once registered with a KRA, your KYC record is valid across the entire mutual fund industry.

Step 3: Choose Your Investment Route

Direct route: You manage all transactions personally through normal banking channels. The application form requires you to specify whether the investment is on a repatriable or non-repatriable basis — this determines which account is used.

Power of Attorney (PoA) route: You authorise a trusted person in India to transact on your behalf. This route suits NRIs who can't manage Indian paperwork remotely. The PoA document must meet these requirements:

- Signed by all unit holders and the PoA holder

- Notary-attested in original (per standard AMC requirements such as those set by Nippon India MF)

Step 4: Verify AMC Eligibility and Select Funds

Not every AMC accepts NRI investors from all countries. US and Canada residents face the most restrictions due to FATCA compliance requirements.

Eligible NRIs can invest across fund categories:

- Equity funds — suited for long-term wealth creation

- Debt funds — for capital preservation and stability

- Hybrid funds — balanced exposure across asset classes

- Index funds — passive, low-cost market exposure

Before investing, review the fund's Scheme Information Document (SID) — it will list any NRI-specific conditions, country restrictions, or repatriation terms that apply.

Step 5: Invest via Lumpsum or SIP

NRIs can invest as a single lumpsum or through a Systematic Investment Plan (SIP), with periodic amounts debited directly from the NRE or NRO account.

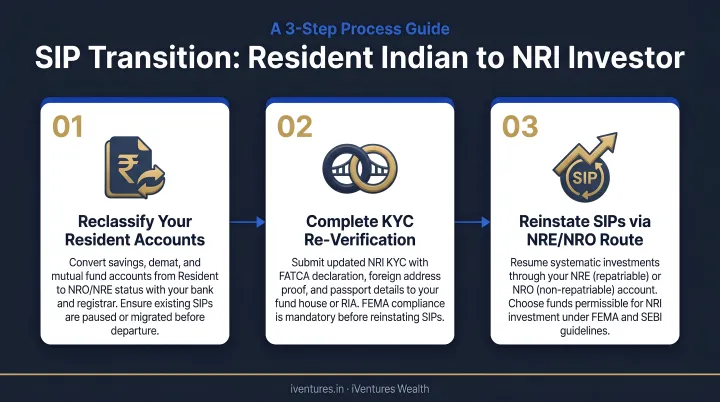

If you had active SIPs as a resident Indian and have since become an NRI, those SIPs don't automatically continue under the correct structure. You'll need to take these steps with each AMC:

- Notify each AMC of your change in residency status

- Update the linked bank account from your resident savings account to an NRO account

- Submit updated KYC documents reflecting NRI status

The AMC credits redemption proceeds — after TDS deduction — directly to the linked NRE or NRO account.

Tax Implications for NRIs Investing in Indian Mutual Funds

How TDS Works

AMCs deduct TDS directly from redemption proceeds or dividend payouts before crediting your account. You don't separately remit tax to the Indian government on mutual fund gains — it's handled at source. This differs from the resident Indian system, where advance tax and self-assessment obligations apply separately.

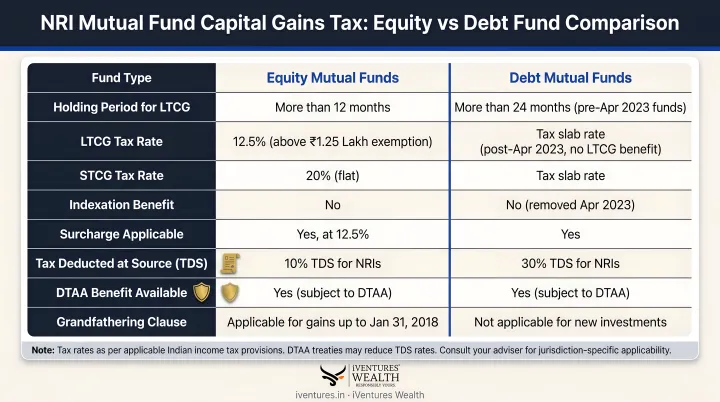

Capital Gains Tax Rates

Per AMFI's current tax regime guidance and Nippon India MF's FY 2025-26 tax reckoner, the applicable rates are:

Equity-oriented funds (>65% equity):

| Holding Period | Tax Rate | TDS Rate for NRIs |

|---|---|---|

| < 12 months (STCG) | 20% | 20% |

| > 12 months (LTCG) | 12.5% on gains above ₹1.25 lakh | 12.5% |

Rates applicable for transfers on or after July 23, 2024.

Debt-oriented and specified mutual funds:

Under Section 50AA, gains on funds acquired after April 1, 2023 — where domestic equity exposure doesn't exceed 35% — are treated as short-term regardless of holding period and taxed at the investor's applicable slab rate.

From FY 2025-26, "specified mutual funds" covers funds investing more than 65% in debt and money market instruments.

Note: All rates above are base rates. Surcharge and 4% Health and Education Cess apply additionally where relevant.

Avoiding Double Taxation Using DTAA

India has signed Double Taxation Avoidance Agreements with an extensive list of countries, accessible through the Income Tax Department's DTAA database. Relief is granted under Sections 90 and 90A of the Income Tax Act.

To claim treaty benefits, NRIs must submit:

- Tax Residency Certificate (TRC) from their country of residence

- Electronic Form 10F

- A self-declaration to the AMC

Treaty provisions vary significantly by country. A tax adviser familiar with both Indian and your resident-country obligations is essential — particularly for jurisdictions like the US, UK, UAE, or Singapore where treaty terms differ meaningfully.

FATCA and CRS: What US/Canada NRIs Must Know

FATCA requires Indian AMCs to report US account holder information to US tax authorities. Not all AMCs are equipped to handle this compliance, limiting US and Canada-based NRIs to a smaller pool of eligible fund houses.

AMCs confirmed to accept US/Canada NRI investments (with a signed declaration) include:

- PPFAS Mutual Fund

- Aditya Birla Sun Life MF

MF Utilities confirms that US/Canada residents must upload a signed declaration in each fund house's required format. Some AMCs also require offline transactions rather than purely digital processing.

FATCA is US-specific, but the Common Reporting Standard (CRS) casts a wider net. The OECD's 2024 peer review reports that tax authorities from 111 jurisdictions automatically exchanged financial account information covering over 134 million accounts. NRIs from CRS-participating countries should expect their Indian investment data to be reported to their resident country's tax authority.

Practical takeaway: Before investing from the US or Canada, verify directly with the AMC whether they accept your residency status and what additional declarations are required.

Common Mistakes NRIs Make

Not Notifying AMCs After Becoming an NRI

When resident Indians transition to NRI status, they must proactively update all existing AMCs and fund houses. AMFI's KYC change form includes residential status fields requiring an updated passport and overseas address proof. Existing SIPs don't self-convert — the bank account must be changed from resident savings to NRO, and the fund house must be formally notified.

Transacting Through the Wrong Bank Account

Investment applications linked to a foreign bank account are rejected outright. Continuing to use a resident savings account after acquiring NRI status is not permitted under FEMA. Only NRE or NRO accounts qualify as source and redemption accounts for mutual fund investments.

Missing DTAA Benefits and Paying Double Tax

Many NRIs are unaware they can claim Foreign Tax Credit (FTC) in their resident country for taxes already paid in India. Not submitting a Tax Residency Certificate (TRC) means paying full tax in both jurisdictions unnecessarily. Cross-jurisdictional tax planning — especially for NRIs in the US, UK, or UAE — is complex.

Navigating these complexities — account structuring, DTAA documentation, and multi-jurisdiction tax coordination — is where a dedicated advisory relationship pays off. iVentures Wealth, a SEBI-registered RIA (INA000019026) with 20+ years of experience and a dedicated NRI/OCI practice, helps clients structure investments across NRE/NRO accounts and manage cross-border tax obligations. The firm's fee-only model means conflict-free recommendations across all regulated products.

Frequently Asked Questions

Which mutual funds are best for NRIs?

The right fund type depends on your financial goals, risk tolerance, and investment horizon. Equity funds suit long-term wealth creation; debt funds offer stability; hybrid funds balance both. NRIs should also factor in TDS rates by fund category and repatriation requirements when selecting.

Can NRIs invest in mutual funds through SIPs?

Yes. SIPs can be set up with periodic amounts debited directly from an NRE or NRO account. If you had existing resident SIPs before becoming an NRI, you can continue them by updating the linked bank account and notifying the AMC of your changed residency status.

Do NRIs pay tax on mutual fund gains?

Yes, gains are taxable in India at the same rates applicable to resident investors. However, TDS is deducted at source by the AMC, so no separate payment is required. DTAA relief may reduce or eliminate double taxation in your resident country.

Can NRIs from the US or Canada invest in Indian mutual funds?

Yes, but with restrictions. Only select FATCA-compliant AMCs accept US and Canada-based NRIs, and some require offline transactions plus additional signed declarations. Always verify AMC eligibility before investing from these countries.

What is the difference between NRE and NRO accounts for mutual fund investment?

NRE accounts hold foreign earnings remitted to India: interest is tax-free and funds are fully repatriable. NRO accounts hold Indian-source income, where interest is taxable and repatriation is capped at USD 1 million per financial year. Both can fund mutual fund investments depending on where your money originates.

Can NRIs repatriate mutual fund returns abroad?

Investments linked to an NRE account are fully repatriable: both principal and gains can be transferred abroad without restriction. For NRO-linked investments, repatriation is capped at USD 1 million per financial year after applicable taxes are paid.