This scenario plays out constantly across Indian households. According to a PGIM India Mutual Fund survey, 51% of urban Indians have no formal retirement plan. The Axis Max Life IRIS study adds that 50% expect to rely on family wealth or children to fund retirement — a strategy that leaves both generations financially exposed.

For couples, the stakes are higher and the opportunity is greater. Two incomes mean two sets of tax deductions, two NPS accounts, two EPF streams, and the ability to structure investments across two tax profiles. Most couples leave this advantage completely untapped.

Key Takeaways

- Both spouses can independently claim ₹1.5 lakh under Section 80C — doubling the household's tax-saving capacity to ₹3 lakh annually

- Separate NPS Tier-1 accounts give each partner an additional ₹50,000 deduction under Section 80CCD(1B)

- Plan for the longer lifespan: Indian women are projected to outlive men by 3.5 years by 2031–36, so joint corpus targets must account for this gap

- Staggered retirements preserve cash flow, active health insurance, and EPF contributions during transition

- Estate planning — nominations, wills, survivor mandates — protects whichever spouse is less financially active

Build a Shared Retirement Vision Together

Most Indian couples avoid this conversation for three reasons: money remains a social taboo, one partner is assumed to "handle finances," and children are quietly expected to fill any gaps. None of these are plans.

The foundation of joint retirement planning is a written, shared vision — not an investment list.

The Questions That Matter

Start here:

- At what age does each partner want to retire? Simultaneously or in stages?

- What does post-retirement life look like — same city, tier-2 relocation, travel, a second career?

- What monthly income (in today's rupees) would sustain that lifestyle?

- Who covers aging parents, and for how long?

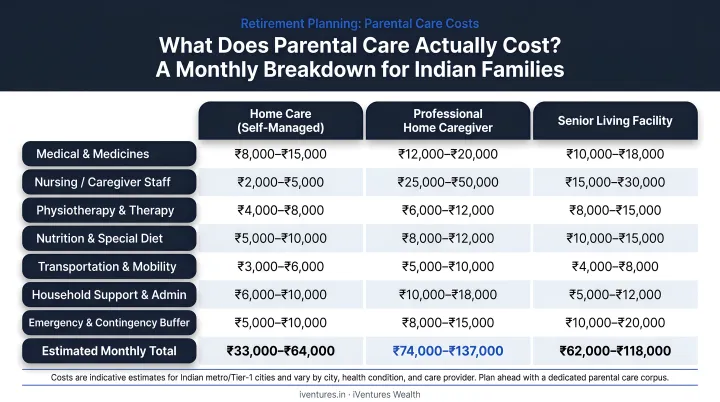

That last question deserves its own conversation. Many Indian couples must plan for their own retirement while simultaneously bearing the cost of parental care — costs that directly affect how large a corpus they need.

| Care Type | Monthly Cost Range |

|---|---|

| Basic home care | ₹15,000 – ₹30,000 |

| Live-in non-medical attendant | ₹35,000 – ₹50,000 |

| Nurse-led 24/7 care | ₹70,000 – ₹1,20,000 |

These figures can shift a retirement corpus target by ₹50 lakh to over ₹1 crore, depending on how long care is required.

Aligning Different Risk Appetites

Agreeing on a shared vision is one thing. Agreeing on how to invest toward it is another.

One spouse may be comfortable with equity-heavy portfolios; the other may prefer fixed deposits. Neither approach is wrong. Running two disconnected strategies within one household, though, creates allocation blind spots and tax inefficiencies that quietly erode returns over time.

The goal is not identical portfolios. It is a unified investment policy where the household's combined asset allocation reflects shared goals and a jointly agreed risk tolerance. That policy should be written down, revisited annually, and updated after every major life event — a job change, business exit, inheritance, or a child's overseas education admission.

iVentures Wealth structures this through a goal-based framework that ties each investment to a specific objective, timeline, and required corpus. For couples managing separate accounts, this keeps both partners aligned toward the same milestones — without either set of preferences dominating the other.

Maximise India-Specific Retirement Instruments for Both Spouses

India's statutory and voluntary retirement instruments are individually held — which means couples who plan together can access twice the capacity.

EPF: Your Statutory Foundation

Both salaried partners have individual EPF accounts. The current EPF interest rate is 8.25% for FY 2024–25, with employees contributing 12% of wages and employers contributing a combined 12% split between EPS (8.33%) and EPF (3.67%).

Key actions for couples:

- Track combined EPF balances annually

- Update nominations to each other immediately

- Avoid premature withdrawals — even partial withdrawals erode the compounding base significantly

PPF: Government-Backed, Tax-Exempt Growth

Each spouse can hold an independent PPF account — joint accounts are not permitted. This allows a household to invest up to ₹3 lakh per year (₹1.5 lakh each) in a scheme earning 7.1% p.a., with returns fully exempt from tax.

The 15-year lock-in is often cited as a drawback. For retirement planning, it is a feature: the illiquidity enforces discipline. After maturity, accounts can be extended in 5-year blocks — a useful structure for couples who start in their 30s and want a stable debt anchor through their 50s.

NPS: Individual Pension Streams for Each Partner

Both spouses should open separate NPS Tier-1 accounts. Each partner gets:

- Standard deduction under Section 80CCD(1) within the ₹1.5 lakh ceiling

- An additional ₹50,000 deduction under Section 80CCD(1B) — available to each individually

At retirement, subscribers can withdraw up to 60% as a lump sum; the remaining 40% must be used to purchase an annuity. If the corpus is below ₹5 lakh, full lump-sum withdrawal is permitted.

The NPS Tier-2 account offers flexibility — no lock-in, unrestricted withdrawals — but carries no additional tax benefits. Couples who want liquidity alongside their Tier-1 pension stream can use Tier-2 as a supplementary buffer.

SCSS: Quarterly Income Post-Retirement

Once both partners turn 60, each can individually invest up to ₹30 lakh in SCSS at the current rate of 8.2% p.a., with interest paid quarterly. This is particularly useful for the spouse who retires earlier or has lower pension income: it creates an immediate, predictable income stream without equity market exposure.

A couple with ₹30 lakh in SCSS each can generate ₹1.23 lakh per quarter (combined) in government-backed income. That quarterly payout can cover a significant portion of household fixed expenses, making SCSS one of the most practical instruments to activate in the first five years of retirement.

Use Your Combined Tax Benefits Wisely

Dual-income couples in India have access to one of the most underutilised tax advantages in personal finance: the ability to claim deductions independently across two PAN numbers.

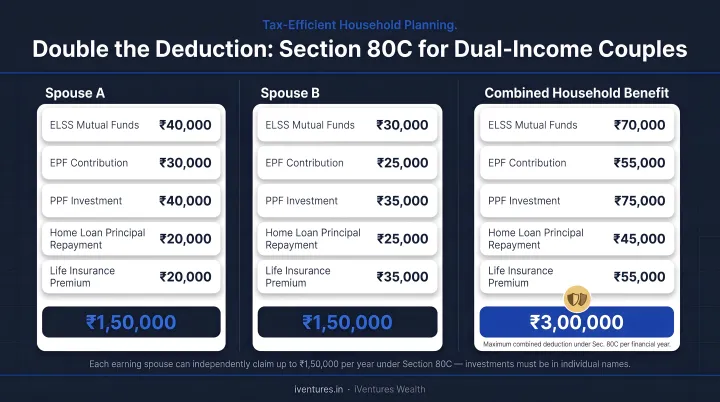

Doubling Section 80C

Each spouse can claim up to ₹1.5 lakh under Section 80C through instruments like EPF, PPF, ELSS, life insurance premiums, and home loan principal repayment. A practical example:

| Instrument | Spouse A | Spouse B |

|---|---|---|

| EPF contribution | ₹72,000 | ₹60,000 |

| PPF | ₹50,000 | ₹70,000 |

| ELSS | ₹28,000 | ₹20,000 |

| Total 80C | ₹1,50,000 | ₹1,50,000 |

Combined household tax deduction: ₹3 lakh annually, all within statutory limits.

Section 80D: Healthcare Deductions for the Family

Current 80D deduction limits per taxpayer:

- Self and family (below 60): ₹25,000

- Self or family as senior citizen: ₹50,000

- Parents below 60: additional ₹25,000

- Senior citizen parents: additional ₹50,000

A couple where one spouse covers the family floater and the other covers aging parents can together claim ₹75,000–₹1,00,000 in combined 80D deductions, depending on parent age. Each spouse must pay their respective premiums from their own income for the deduction to hold.

Income-Splitting and Section 64

If one spouse earns significantly more than the other, investing in the lower-taxed spouse's name can reduce overall household tax liability. However, the clubbing provisions under Section 64 of the Income Tax Act apply when assets are transferred to a spouse without adequate consideration — the Act clubs that income back with the transferor's income.

The practical approach: invest using each spouse's own earned income in their own name. Avoid gifting funds to a spouse purely to access lower tax rates — it rarely survives scrutiny and creates compliance risk.

For couples with significant family assets, an HUF (Hindu Undivided Family) structure is worth exploring. It creates a separate tax entity with its own basic exemption limit, capable of holding investments independently.

Key points before setting one up:

- Requires formal creation with legal documentation

- Works best when established before assets are introduced into the structure

- Professional guidance is strongly recommended at this stage

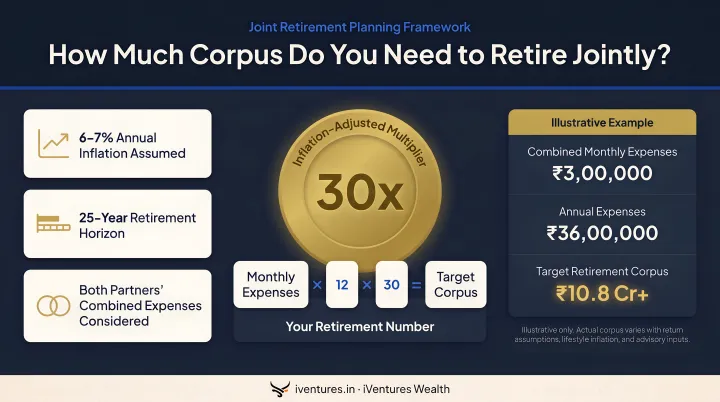

Calculate Your Joint Retirement Corpus Realistically

Unlike solo retirement planning, couples must model a retirement that could span 25–30 years, accounting for the longer-living spouse. According to MOSPI data, projected life expectancy for Indian women reaches 74.7 years by 2031–36, versus 71.2 years for men — a 3.5-year gap that directly extends the planning horizon your corpus must cover.

A Simple Corpus Framework

A commonly used starting point: 25–30 times expected annual retirement expenses.

- Estimate annual retirement expenses in today's rupees

- Apply a 6–7% inflation assumption as a conservative planning buffer (above the RBI's 4% target, accounting for lifestyle and healthcare cost escalation)

- Project over a 25-year horizon minimum

For a couple spending ₹12 lakh annually in retirement: a 30x corpus target implies ₹3.6 crore in today's money, before inflation adjustment. Adjusted forward 15 years at 6%, the actual corpus target exceeds ₹8 crore. Most couples are surprised by how wide that gap is — and how much of it opens up through expenses they never planned for.

Expenses Couples Consistently Underestimate

- Healthcare: India's medical inflation reached 12% in 2024 and was projected at 13% for 2025 — more than triple general CPI. Healthcare reserves need a separate, higher inflation assumption

- Household help: Domestic staff costs rise with age and reduced mobility

- Home maintenance: Ageing infrastructure, lifts, accessibility modifications

- Long-term care: Nursing or assisted-living costs if one partner's health declines

- Children's milestones: Weddings, overseas education support

iVentures Wealth models retirement scenarios using a 4% safe withdrawal rate framework calibrated to Indian inflation and tax structure, and in some cases a more conservative 3–3.5% rate depending on portfolio composition. The goal-based bucket approach separates retirement savings from parental care and education obligations, so each goal is funded with the right instruments and timeline without one priority crowding out another.

For couples with ₹10 Cr+ in investable assets, iVentures can model scenarios that account for existing assets, expected pension entitlements, potential inheritance, and business exits. The result is a corpus target grounded in your actual numbers — not a textbook multiple.

Prepare for Healthcare, Family Obligations, and Estate Planning

Manage Healthcare Costs Proactively

Healthcare is the retirement risk most couples plan for last. Household out-of-pocket health spending in India reached ₹3,56,254 crore in FY 2021–22 — 39.4% of total health expenditure. Without adequate coverage, a single hospitalisation can permanently disrupt a retirement corpus.

Practical steps:

- Maintain comprehensive individual or senior citizen health insurance policies (not just a family floater, which has shared limits)

- Build a dedicated healthcare emergency fund separate from the retirement corpus — 12–24 months of estimated medical expenses

- Review and increase coverage at retirement, since new policies for senior citizens carry waiting periods and exclusions

Plan for Multigenerational Financial Obligations

Indian couples often face competing pulls: children's higher education (including overseas costs), aging parent support, and retirement savings — all simultaneously. The oxygen mask principle applies: secure your retirement first, then plan for other obligations through separate goal-based buckets.

iVentures structures these as three distinct buckets: a Safety bucket for near-term needs, a Stability bucket for medium-term goals, and a Growth bucket for long-horizon objectives. Each obligation gets its own allocation, timeline, and instruments. With separate buckets, education and parent care costs stay ring-fenced from retirement savings.

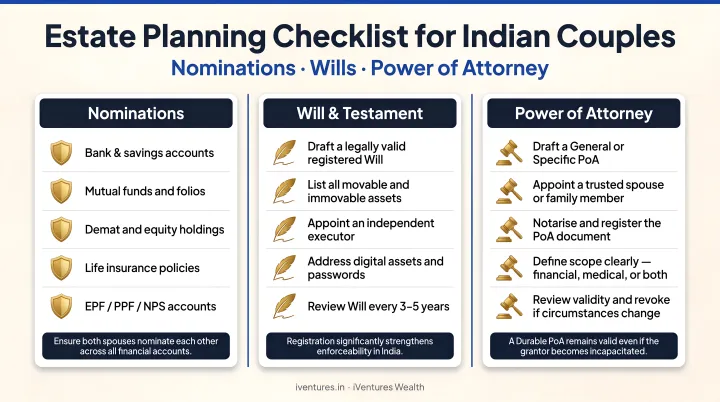

Secure Each Other Through Estate Planning

Estate planning is not morbid — it is the most direct way to protect whichever spouse is less financially involved. Checklist for couples:

- Nominations: Update EPF, PPF, NPS, insurance, mutual funds, and demat accounts separately — nominations are product-specific and do not automatically transfer across accounts

- Will: Draft a will to ensure assets flow as intended; nominations alone are insufficient for comprehensive estate transfer

- Joint bank account: Set up an "either or survivor" mandate for immediate liquidity access on death

- Power of attorney: Arrange for incapacitation scenarios, not just death

- Document inventory: The less financially active spouse must know where every account, document, and login is held

SEBI's revised nomination framework circular (January 2025) makes this a timely moment to audit every nomination across the household.

Frequently Asked Questions

What budgeting rules should couples use in retirement planning?

During the accumulation phase, Indian couples are typically advised to save at least 20–30% of combined income for retirement. Post-retirement, withdrawing no more than 4% of corpus annually (adjusted for inflation) is a widely used rule of thumb for sustaining savings over a 25–30 year horizon.

How can couples plan to thrive, not just survive, in retirement?

Build diversified income streams — pension, annuity, SWP from mutual funds, rental income, and SCSS payouts — to anchor financial security. Alongside that, plan how you'll spend time together: shared interests, travel, and social engagement matter as much as the corpus size.

What are the 3 R's of retirement planning for couples?

Three essential pillars: Resources (joint corpus through coordinated investments and tax planning), Relationships (aligned goals and open financial communication), and Resilience (planning for health emergencies, early spouse death, and market downturns through insurance and diversification).

Should both spouses have separate NPS accounts in India?

Yes. Each spouse with a Tier-1 NPS account gets an additional ₹50,000 tax deduction under Section 80CCD(1B), independent of the standard ₹1.5 lakh ceiling. Separate accounts also build individual pension streams , which is especially valuable if one spouse retires earlier or earns less.

How much retirement corpus does a couple in India typically need?

A common starting point is 25–30 times annual retirement expenses, adjusted for inflation across a 25–30 year horizon — with separate buffers for healthcare and family obligations. A personalised plan from a SEBI-registered adviser will give you a far more accurate target than any generic multiplier.