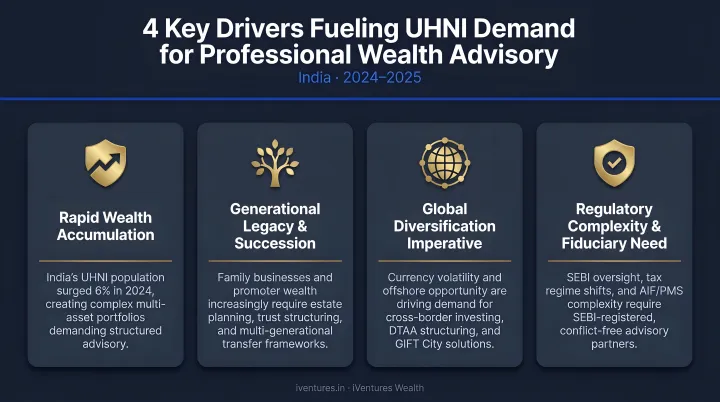

For UHNIs, family offices, startup founders, and NRIs navigating this environment, the stakes in choosing the right advisor have never been higher. Market volatility, revised capital gains tax rates, LRS outflows of approximately US$30 billion in FY25, and growing cross-border complexity all demand more than a relationship manager with a product brochure.

The difference between a fiduciary advisor and a commission-driven distributor can translate directly into better outcomes — and this distinction is what separates the firms on this list from the rest.

This article covers India's top financial advisory firms for 2026, selection criteria, and what to look for when choosing a wealth partner aligned with your goals.

Key Takeaways

- SEBI-registered RIAs operate as fiduciaries — legally required to act in clients' best interests with no undisclosed commissions or trail income from product manufacturers

- The best firms combine regulatory standing, CFA/CFP-credentialled teams, transparent fees, and services beyond just portfolio management

- For UHNIs and family offices, look specifically for estate planning, NRI advisory, and consolidated cross-entity reporting — these separate full-service firms from product sellers

- Verify SEBI registration before engaging any advisor — it confirms regulatory oversight and confirms fiduciary accountability

- iVentures Wealth (SEBI RIA No. INA000019026) is one example of an independent, fee-based firm serving UHNIs, family offices, and corporates with 20+ years of fiduciary advisory

Overview of Financial Advisory in India in 2026

What Type of Advisor Are You Actually Dealing With?

Not all financial advisors in India operate under the same regulatory framework — and this matters enormously for the quality of advice you receive.

| Role | Regulator | Compensation | Fiduciary Standard |

|---|---|---|---|

| SEBI-Registered RIA | SEBI IA Regulations 2013 | Client-paid fees only | Full fiduciary duty |

| Mutual Fund Distributor (MFD) | AMFI | Trail commissions from AMCs | Code of conduct; not fiduciary |

| PMS Provider | SEBI Portfolio Managers Regs | Portfolio management fees | SEBI regulated; min ₹50L investment |

| Private Bank Wealth Arm | RBI + SEBI | Product fees + referral arrangements | Disclosure-based; varies by structure |

SEBI's Investment Advisers Regulations 2013 (last amended December 16, 2024) require registered RIAs to act in a fiduciary capacity, disclose conflicts, and not accept any compensation from anyone other than the client being advised. Distributors and bank wealth managers, by contrast, earn trail income on the products they recommend — a structural conflict the fiduciary model eliminates entirely.

What's Driving Demand for Professional Advisory

Several converging forces are pushing HNIs and UHNIs toward professional advisors:

- Startup and PE exits: India's PE-VC exit activity reached approximately US$33 billion in 2024, generating founder liquidity that requires disciplined, structured deployment

- NRI inflows: NRI deposit inflows rose 23% to US$14.55 billion from April 2024 to February 2025

- Tax complexity: Revised capital gains rates — 20% STCG and 12.5% LTCG on specified financial assets — require active tax-efficient portfolio structuring

- Cross-border complexity: LRS outflows of approximately US$30 billion in FY25 reflect rising demand for DTAA structuring and global investment advisory

Given these pressures, choosing the right advisor matters as much as choosing the right investment. The firms listed below were evaluated on fiduciary standards, team credentials, AUM, breadth of services, and fee transparency.

Top Financial Advisors and Firms in India for 2026

Each firm below was assessed on regulatory standing, team qualifications, assets under advice, client segment focus, and depth of advisory services — giving you a structured basis for comparison rather than rankings based on brand name alone.

iVentures Wealth

Founded in 2005 by Nirmal A Bansal (UCLA Anderson alumnus, former DSP Merrill Lynch professional), iVentures Wealth is a Gurugram-based SEBI-registered investment adviser (RIA No. INA000019026) with a CFA-credentialled research team led by Krishna Makhariya, Head of Research and Executive Director.

The firm manages ₹1,146+ Cr in assets for 150+ affluent client relationships — UHNIs, CEOs, CXOs, family offices, NRIs/OCIs, and corporates across India. As a fee-only RIA, the firm is prohibited from earning commissions or trail income from product manufacturers — a structural commitment to conflict-free, fiduciary advice.

The firm was recognised as Preferred Wealth Partner of 2022 by Mr. Vikram Yadav, Deputy Commissioner, IAS, Government of Haryana.

| Detail | Information |

|---|---|

| Key Credentials | SEBI-Registered RIA (INA000019026), CFA Charterholder, NSE & CDSL accredited |

| Client Segments | UHNIs, HNIs, CEOs, CXOs, Founders, Family Offices, NRIs/OCIs, SMEs & Corporates |

| Core Services | Portfolio management, family office advisory, tax optimisation, NRI advisory, estate planning, Wealth Monitor App, real estate advisory |

| Fee Model | Fee-only; no commissions or trail income |

Kotak Mahindra Private Wealth

Kotak Private is the private banking and wealth arm of Kotak Mahindra Bank, one of India's largest private sector banks. The firm reported a Relationship Value/AUM of ₹10,80,000 Cr as of March 31, 2026, and manages wealth for a significant share of India's top families.

Euromoney named Kotak Private Banking Best Private Bank: India, 2026. Investment advisory is provided through Kotak Alternate Asset Managers Ltd (KAAML), a SEBI-registered investment adviser.

The firm's core strength is the integration of private banking, wealth management, and credit solutions under one ecosystem — including structured products, direct equity research, and estate planning with access to banking credit facilities that standalone advisory firms cannot replicate.

| Detail | Information |

|---|---|

| Key Credentials | Kotak Mahindra Bank-backed; SEBI-registered advisory via KAAML; Euromoney Best Private Bank India 2026 |

| Client Segments | UHNIs, HNIs, business families |

| Core Services | Portfolio management, structured products, estate planning, credit solutions, private banking |

HDFC Securities Private Wealth

HDFC Securities holds SEBI Investment Adviser registration INA000011538, alongside stock-broker and research analyst registrations. Its private wealth division serves HNIs and corporates through a dedicated wealth advisory team with access to HDFC Group's banking, insurance, and lending ecosystem.

The firm differentiates through its research backbone, multi-asset investment approach, and the brand trust of the HDFC Group. Notably, HDFC Securities is not a SEBI-registered PMS provider — a distinction worth understanding when comparing service structures.

| Detail | Information |

|---|---|

| Key Credentials | SEBI IA registration INA000011538; part of HDFC Group |

| Client Segments | Affluent individuals, HNIs, and corporates |

| Core Services | Financial planning, multi-asset portfolio management, investment advisory, estate and succession planning |

Motilal Oswal Private Wealth

Motilal Oswal Wealth Ltd holds SEBI Portfolio Manager registration INP000004409 and AIF Category III registration. As of FY26, group Assets under Advice were reported at ₹6.6 lakh Cr; ICRA's October 2025 rating report puts Motilal Oswal Wealth Ltd's standalone AUA at approximately ₹4.9 lakh Cr.

The firm is built on Motilal Oswal's equity research heritage — including its annual Wealth Creation Study — making it particularly well-regarded among clients seeking research-backed, equity-heavy portfolios with AIF and PMS access.

| Detail | Information |

|---|---|

| Key Credentials | SEBI PMS (INP000004409); AIF Category III; equity research pedigree |

| Client Segments | HNIs, UHNIs focused on equity and alternative investments |

| Core Services | PMS, AIF, equity advisory, wealth planning, succession planning |

Anand Rathi Wealth Limited

Anand Rathi Wealth is a listed entity on NSE and BSE with a private wealth business operating since 2002. As of March 2025, the firm reported AUM of ₹75,084 Cr with 11,732 active client families — an 18% year-on-year increase in client numbers.

The firm's network of relationship managers enables broad geographic coverage across India. Its strength lies in combining mutual fund distribution and financial product access with systematic, goal-based financial planning for HNIs and business families.

| Detail | Information |

|---|---|

| Key Credentials | Listed entity (NSE/BSE); AMFI-registered (ARN-111569); large RM network |

| Client Segments | HNIs, business families, affluent individuals |

| Core Services | Mutual funds, financial planning, PMS, structured products |

How We Chose the Best Financial Advisors

Firm selection was based on five key factors:

- SEBI registration status — RIA registration is the clearest marker of fiduciary accountability. PMS and distribution licences operate under different conflict standards

- Team credentials — CFA and CFP designations indicate rigorous, professionally validated investment expertise

- AUM and client base — where officially published, AUM and client numbers serve as evidence of established trust and operating scale

- Service breadth — firms offering estate planning, NRI advisory, tax optimisation, and consolidated reporting rank higher for UHNI and family office suitability

- Fee model — fee-only structures eliminate the principal-agent conflict inherent in commission-led advisory

Brand name and firm size are not proxies for advice quality. A smaller, independent SEBI-RIA firm often delivers more personalised, conflict-free advice than a large institutional player whose revenue model depends on product distribution. Clients should evaluate fit based on their own financial complexity — not a firm's marketing presence or AUM headline.

Before choosing any advisor, ask one question: how does this advisor get paid? If the answer involves commissions or trail income from product manufacturers, the recommendation is not structurally independent — regardless of how trusted or well-known the firm appears.

Conclusion

Choosing a financial advisor in 2026 is about finding a long-term partner whose interests are structurally aligned with yours. SEBI registration, credential quality, fee transparency, and the ability to navigate complex financial situations — not just bull-market portfolio construction — are the real tests.

Look beyond brand recognition. Ask about track record through different market cycles, communication style, and whether the advisor's services genuinely match your financial complexity. An advisor who served you well at ₹5 Cr in investable assets may not be the right partner at ₹50 Cr with cross-border assets, a business, and succession planning to address.

That complexity is exactly where the right firm earns its place. iVentures Wealth is a SEBI-registered advisory firm (INA000019026) with 20+ years of experience, ₹1,200 Cr+ in assets under advice, and a CFA-led research team serving HNIs, UHNIs, NRIs, and family offices across India. Reach out for a confidential, no-obligation consultation to explore how personalised wealth management can work for your goals.

Frequently Asked Questions

Who are the top financial advisor firms in India for 2026?

Leading firms include SEBI-registered independent advisers like iVentures Wealth and private wealth divisions of large institutions including Kotak Mahindra Private Wealth, HDFC Securities Private Wealth, Motilal Oswal Private Wealth, and Anand Rathi Wealth. The best firm depends on your net worth, goals, and preference for independent fiduciary advisory versus institutional wealth management.

What is a SEBI Registered Investment Adviser (RIA)?

A SEBI-registered RIA is licensed under the Securities and Exchange Board of India's Investment Advisers Regulations 2013 to provide investment advice as a fiduciary. RIAs are legally required to act in the client's best interest and cannot earn undisclosed commissions — making SEBI RIA status the strongest marker of conflict-free advisory in India.

How do I choose the right financial advisor in India?

Verify SEBI registration, check team credentials (CFA, CFP), and understand how the advisor is compensated — fee-only versus commission-based. Assess whether services match your needs (estate planning, NRI advisory, tax optimisation), and evaluate their track record with clients at a similar wealth level and complexity.

What is the difference between a financial advisor and a wealth manager?

A financial advisor typically focuses on investment planning and specific financial goals. A wealth manager offers more comprehensive services — investments, tax planning, estate structuring, succession planning, and family office advisory — making it the right fit for HNIs and UHNIs managing layered, cross-generational financial structures.

How much does a financial advisor charge in India?

SEBI caps RIA fees at 2.5% of assets under advice per annum per family, or ₹1,25,000 fixed fee per family per year — whichever mode the adviser operates under. Actual fees vary by firm and mandate complexity. Commission-based distributors do not charge clients directly but earn trail income from product manufacturers, which is worth accounting for in total cost comparisons.

What should I look for in a financial advisor for UHNIs or family offices?

Look for experience in multi-generational wealth planning, estate and succession structuring, cross-border tax optimisation, and consolidated portfolio reporting. At this level of complexity, genuine fiduciary commitment — SEBI RIA status plus a fee-only model — matters more than firm size.