Introduction

Many NRIs earn income in India — rent from a property in Delhi, dividends from equity holdings, or proceeds from selling an ancestral home — yet struggle to move those funds to their overseas bank account without running into documentation requirements, tax clearances, and FEMA restrictions they weren't expecting.

NRO account repatriation is the process of converting INR-held funds in a Non-Resident Ordinary account and transferring them to a foreign currency account in the NRI's country of residence. The RBI's USD 1 million annual cap, mandatory tax settlement requirements, and multi-form filings make it one of the more complex cross-border financial processes NRIs encounter.

Here's what this guide covers:

- What NRO repatriation means and which income qualifies

- The exact step-by-step transfer process

- Every document you'll need at each stage

- Tax implications — including where DTAA treaties can reduce your burden

Key Takeaways

- NRO accounts hold India-sourced income; repatriation transfers those funds overseas under FEMA and RBI rules

- The annual limit is USD 1 million per financial year (April–March), covering all capital and current account transactions combined

- Four forms are required: Form 15CA (self-declaration), Form 15CB (CA certificate), Form A2 (FEMA declaration), and the bank's transfer request form

- All NRO funds must be tax-cleared before transfer — interest income typically attracts TDS at 30% plus surcharge and cess

- NRE accounts are freely repatriable with no cap; NRO repatriation has a USD 1 million annual cap, requires more documentation, and unused limits do not carry forward

What Is NRO Account Repatriation?

An NRO account is a rupee-denominated account where NRIs deposit income earned within India — rent, interest, dividends, pension payments, or proceeds from selling property. Repatriation is the act of converting these INR-held funds into foreign currency and transferring them to the NRI's overseas bank account.

What Income Qualifies?

Not all NRO funds are eligible in the same way. The RBI distinguishes between two categories:

- Current income — salary (where applicable), rental income, dividends, pension, and interest earned in India

- Capital receipts — proceeds from the sale of immovable property (capped at two residential properties) and other legitimate Indian assets

One category that catches many NRIs off guard: investments made from NRO funds into mutual funds or equity shares are generally classified as non-repatriable under FEMA Non-Debt Instruments Rules, 2019 (Schedule IV). The income earned on those investments — dividends, for example — may qualify, but the invested capital itself typically does not.

Always verify the latest RBI circular before assuming repatriability on NRO-routed investments.

NRO vs. NRE Repatriation: The Key Difference

Understanding where NRO ends and NRE begins matters — the compliance burden and tax treatment differ sharply between the two.

| Feature | NRO Account | NRE Account |

|---|---|---|

| Source of funds | India-earned income | Foreign-sourced income |

| Annual repatriation cap | USD 1 million | None |

| Indian tax on interest | Yes (~30% TDS) | Exempt under Section 10(4)(ii) |

| Forms required | 15CA, 15CB, A2 | Not required |

NRE balances are fully repatriable, with no forms and no Indian tax on interest. Treating NRO funds as NRE-equivalent — and skipping Form 15CA/15CB — is what leads to compliance notices and delayed transfers.

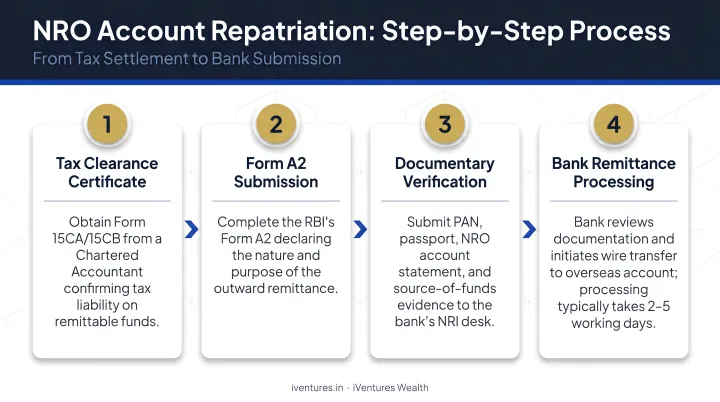

How NRO Repatriation Works: Step-by-Step Process

The process runs through four sequential stages: tax settlement, CA certification, online self-declaration, and bank submission.

Step 1: Settle All Tax Dues on NRO Funds

Before initiating any transfer, every applicable Indian tax must be paid or deducted on the funds being repatriated.

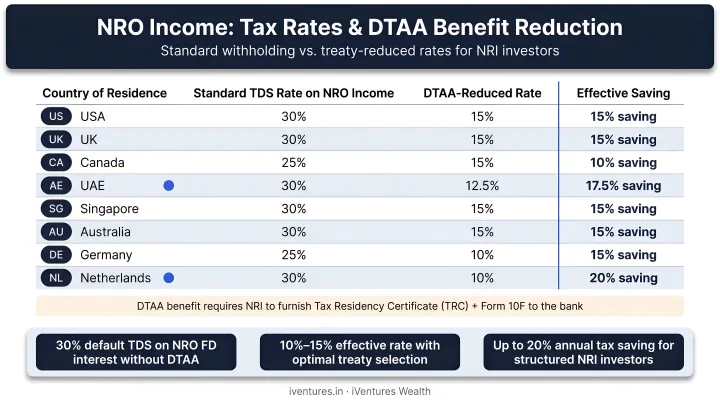

Interest income in NRO accounts is subject to TDS at 30% plus applicable surcharge and health and education cess under Section 195 of the Income Tax Act.

If India has a Double Taxation Avoidance Agreement (DTAA) with your country of residence, you may claim a reduced TDS rate. To do so, submit a Tax Residency Certificate (TRC) and Form 10F to your bank. The USA, UK, Canada, and UAE all have active DTAAs with India.

For property sale proceeds, capital gains tax applies. Property held for more than 24 months qualifies as long-term; transfers on or after July 23, 2024 attract LTCG tax at 12.5% without indexation under the Finance (No. 2) Act, 2024.

Step 2: Obtain Form 15CB from a Chartered Accountant

Form 15CB is the CA's certification that taxes have been correctly deducted and deposited on the remittance amount. Your CA reviews the source of funds, verifies tax compliance, and certifies:

- The amount being remitted

- The nature of payment

- Applicable DTAA provisions (if claimed)

- The TDS rate applied

The CA uploads Form 15CB on the Income Tax e-filing portal and e-verifies it. This generates an acknowledgement number that you will need for the next step.

Note on threshold: Under CBDT Notification No. 93/2015 (Rule 37BB), Form 15CB is required when the chargeable remittance or aggregate chargeable remittances exceed ₹5 lakh in a financial year. Below this threshold, Part A of Form 15CA applies without a CA certificate.

Step 3: File Form 15CA Online

Form 15CA is your self-declaration filed on the Income Tax e-filing portal. It records:

- Your identity as the remitter

- The nature and amount of remittance

- Overseas bank account details

- The CA's Form 15CB acknowledgement number

The form is e-verified using DSC or EVC, and a system-generated acknowledgement number is issued upon submission. Print and sign this form — you'll need to physically submit it to the bank.

Step 4: Submit Documents to the Bank

Submit all documents to the branch where your NRO account is held. The bank confirms tax clearance and initiates the outward remittance to your designated overseas account.

For larger transactions (particularly property sale proceeds), the bank may request additional source-of-funds documents (sale deed, registered agreement, etc.) beyond the standard forms.

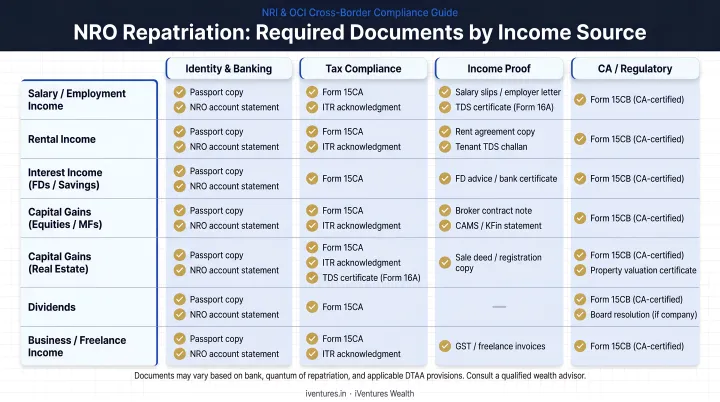

Documents Required for NRO Account Repatriation

NRO repatriation requires more paperwork than NRE or FCNR transfers because every rupee being sent abroad must be traceable to a tax-cleared India source. All copies should be self-attested unless your bank specifies originals.

Form 15CA

Your online self-declaration filed on the Income Tax e-filing portal before the bank processes the transfer. It captures remitter identity, remittance amount and purpose, overseas account details, and the CA's Form 15CB reference. The acknowledgement receipt must accompany your bank submission.

Form 15CB

The CA's signed and sealed certificate confirming that TDS has been correctly calculated, deducted, and deposited. Mandatory for aggregate chargeable remittances exceeding ₹5 lakh in a financial year. Without this, the bank cannot process the transfer.

Form A2 (FEMA Declaration)

Form A2 is the RBI-prescribed declaration for all outward foreign exchange transactions. It records the purpose of the remittance and your confirmation that the transfer is for a FEMA-permitted purpose. Your bank provides this form and processes it as your Authorised Dealer.

Bank Repatriation Request Form and Supporting Documents

In addition to the regulatory forms, your bank will require:

- Bank's own repatriation request form (specifying amount, destination account, and currency)

- Passport copy for identity verification

- PAN card

- Visa or OCI card

- Source-of-funds documents, which vary by income type:

| Income Source | Document Required |

|---|---|

| Property sale | Registered sale deed |

| Rental income | Rent agreement + Form 16A or Form 26AS |

| Dividend income | Dividend warrant or bank statement |

| Inherited assets | Will, succession certificate, or court order |

FEMA Rules, Limits, and Tax Implications for NRO Repatriation

The USD 1 Million Annual Cap

Per RBI guidelines under FEMA 13(R)/2016-RB consolidated in Master Direction No. 13, NRIs can repatriate up to USD 1 million per financial year (April to March) from NRO balances and other eligible assets. This is an aggregate annual facility — not a per-transaction limit. All repatriations in a given year count toward it.

Two additional restrictions apply:

- Sale proceeds from a maximum of two residential properties qualify for repatriation

- Proceeds from more than two residential properties fall outside this facility

If you need to repatriate more than USD 1 million, you must apply to the Chief General Manager-in-Charge, Foreign Exchange Department, Reserve Bank of India, Central Office, Mumbai with specific grounds — medical emergencies and overseas property acquisition are cited circumstances in the RBI's FAQ.

Current Income vs. Capital Receipts

The distinction between current income and capital receipts matters for repatriation planning:

- Current income (rent, dividends, interest, pension) can be repatriated in the year it is earned or carried forward and repatriated in subsequent years

- Capital receipts (property sale proceeds) are subject to the USD 1 million cap and do not have a separate unlimited facility

Tax Implications

| Income Type | Tax Treatment |

|---|---|

| NRO interest | TDS at ~30% + surcharge + cess (Section 195) |

| Long-term property gains (post July 23, 2024) | 12.5% without indexation |

| Short-term property gains | Normal rates applicable to the assessee |

NRIs with residency in DTAA countries — including the USA, UK, Canada, and UAE — can reduce the effective withholding rate by submitting a Tax Residency Certificate and Form 10F to their bank before the transfer is processed. This step alone can substantially reduce the tax outflow on NRO income.

Where DTAA claims intersect with Indian TDS rules and overseas filing obligations, coordinated cross-border advice makes a material difference. iVentures Wealth (SEBI RIA: INA000019026) works with NRIs on DTAA structuring, Form 15CA/15CB compliance, and FEMA-compliant repatriation planning across key NRI geographies.

Common Misconceptions About NRO Repatriation

"NRO-invested mutual funds and equity shares are repatriable"

This is incorrect. Under FEMA Non-Debt Instruments Rules, 2019 (Schedule IV), investments made from NRO funds — including mutual fund units and equity instruments — are on a non-repatriation basis. Sale and maturity proceeds are credited back to the NRO account, not remitted abroad directly.

Any outward movement must still go through the standard NRO repatriation process, subject to the USD 1 million annual cap and full tax compliance. Only income earned on such investments — such as dividends — may separately qualify for repatriation. Consult a qualified CA or tax advisor, and refer to RBI's Master Directions, before acting on this.

"NRO and NRE repatriation work the same way"

They do not. The two accounts operate under fundamentally different rules:

- NRE account: No forms required, no tax clearance, no annual ceiling on repatriation

- NRO account: Requires Form 15CA, Form 15CB (above the ₹5 lakh threshold), Form A2, bank-specific forms, and full tax settlement

Treating them as equivalent is one of the most common reasons for bank rejections and compliance gaps.

"Unused repatriation limits accumulate year to year"

The RBI states the USD 1 million facility as a per-financial-year cap. No primary RBI source confirms that unused limits carry forward to the next year. NRIs planning large repatriations across multiple years — for example, property sale proceeds above USD 1 million — should plan the sequencing carefully within each April-to-March window rather than assuming unused capacity rolls over.

Frequently Asked Questions

What does NRO repatriation mean?

NRO repatriation is the process of transferring funds from a Non-Resident Ordinary account (which holds income earned within India) to an overseas bank account in the NRI's country of residence. FEMA governs the process, and tax clearance is required before any transfer can proceed.

Can funds from an NRO account be repatriated?

Yes. NRIs can repatriate up to USD 1 million per financial year from their NRO account after paying applicable Indian taxes. For comparison, NRE and FCNR accounts offer unrestricted repatriation with no annual cap and no Indian tax on interest.

What is the repatriation rule for NRO account principal?

Principal in an NRO account (such as property sale proceeds or inherited assets) can be repatriated up to USD 1 million per financial year under FEMA. This covers proceeds from a maximum of two residential properties; additional properties fall outside this facility.

What are the documents required for NRO account repatriation?

The core documents required are:

- Form 15CA — online self-declaration of remittance

- Form 15CB — CA certificate confirming tax payment (required when aggregate chargeable remittances exceed ₹5 lakh)

- Form A2 — FEMA declaration submitted to the bank

- Bank's repatriation request form and source-of-funds proof (sale deed, rent agreement, or dividend statement)

Is NRO repatriation taxable in India?

Yes. Interest income faces TDS at around 30% (plus surcharge and cess), while property sale proceeds attract short-term or long-term capital gains tax. NRIs can lower their effective rate by claiming DTAA benefits where a treaty exists between India and their country of residence.

Can the USD 1 million NRO repatriation limit be carried forward?

No. The RBI states this as a per-financial-year facility running from April to March. NRIs needing to repatriate amounts above USD 1 million must either spread transfers across multiple financial years or apply to the RBI for special permission, citing specific hardship grounds.