Introduction

Picture two families. In the first, a successful entrepreneur passes away unexpectedly — no Will, no Trust, no succession plan. Within weeks, bank accounts are frozen, children are in dispute over property, and a business built over three decades sits in legal limbo.

In the second family, the patriarch had spent a few hours with his advisors years earlier. Assets transfer cleanly, beneficiaries receive their shares, and the business continues without interruption. Same circumstances — entirely different outcomes, because one family planned and the other didn't.

India's UHNI population reached 13,263 individuals (net worth $30M+ USD) in 2023 and is projected to grow over 50% by 2028, according to the Knight Frank Wealth Report. Yet 36% of Indian family businesses lack clear succession plans — 8 percentage points worse than the global average.

The window to act is open right now. India has no inheritance tax. Probate rules just got simpler. But religion-specific succession laws, complex family structures, and rising political discussion around wealth redistribution mean that window won't stay open.

Key Takeaways

- Estate planning organises how your assets (property, investments, business interests) are managed and distributed during your lifetime and after death

- India has no inheritance or estate tax (abolished in 1985), but income from inherited assets remains taxable

- Succession laws vary by religion — Hindus, Muslims, and Christians follow different legal frameworks

- A Will provides legal clarity; a Trust adds control, privacy, and continuity. Most advisors recommend having both in place

- Starting early with a qualified advisor prevents family disputes and ensures your wishes are legally enforceable

What Is Estate Planning in India and Why It Can't Wait

Estate planning is the organised process of deciding how your assets will be managed, protected, and distributed — during your lifetime and after your death. It covers property, financial accounts, business interests, digital assets, and personal wishes around guardianship and charitable giving. Writing a Will is part of the process — but only one part of a much larger framework.

Estate Planning vs. Succession Planning

These terms are often used interchangeably, but they address fundamentally different concerns.

- Estate planning addresses all assets and personal wishes — healthcare directives, guardianship for minor children, charitable intent, and the full scope of personal wealth

- Succession planning specifically addresses business continuity — who takes over leadership, ownership structures, and operational transitions

If you're a founder, CEO, or family business owner, you need both. Treating them in isolation is one of the most expensive planning mistakes affluent families make.

Why the Urgency Is Real

India's HNWI population reached 3.589 million in 2023, holding total wealth of $1,145.5 billion — up 12.4% in a single year, per the Capgemini World Wealth Report 2024. This pace of wealth creation is dramatically outrunning the adoption of formal succession structures.

Three factors make planning increasingly urgent:

- Complex asset profiles — HNIs today hold wealth across equities, real estate, business interests, ESOPs, NRE/NRO accounts, and global investments simultaneously

- Regulatory uncertainty — while India abolished estate duty in 1985, political discussion around inheritance taxation resurfaces periodically; planning now removes speculative risk

- Family structure complexity — blended families, NRI children, and multi-generational businesses create succession scenarios that informal arrangements cannot handle

The more complex your wealth profile, the more a structured plan matters — and the more costly delay becomes.

The Legal Foundation: How Succession Works in India

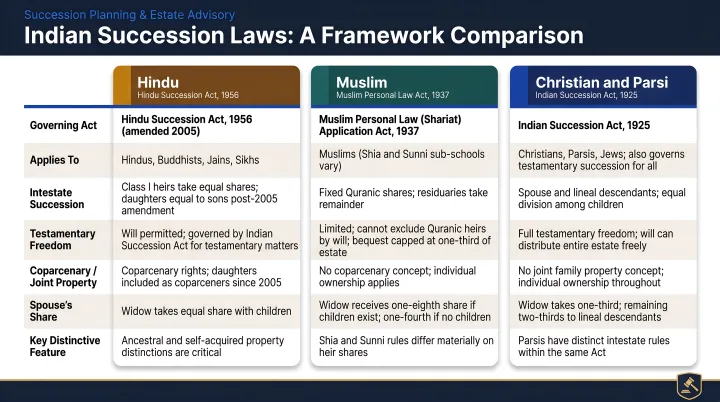

India does not have a uniform civil code for succession at the national level. The law that governs your estate depends primarily on your religion and domicile.

The Three Main Legal Frameworks

| Community | Governing Law | Key Feature |

|---|---|---|

| Hindus, Buddhists, Jains, Sikhs | Hindu Succession Act, 1956 (amended 2005) | Codified statute; governs intestate and testamentary succession |

| Christians, Parsis, and others | Indian Succession Act, 1925 | General statute; governs Wills for all communities |

| Muslims | Muslim Personal Law (Shariat) Application Act, 1937 | Testamentary freedom limited to one-third of the estate |

What Happens Without a Will

When someone dies intestate — without a Will — the law distributes assets strictly according to the applicable personal law, regardless of what the deceased may have verbally communicated or informally intended.

Under the Hindu Succession Act, a Hindu man's estate goes to Class I heirs (spouse, children, mother) in equal shares. If he informally intended to leave a larger share to one child who managed the family business, that intent has no legal standing. The law divides equally, and disputes follow.

These gaps in planning have real consequences — and two legal nuances, in particular, catch families off guard.

Two Legal Nuances Most Families Miss

1. Daughters have equal coparcenary rights. The 2005 amendment to the Hindu Succession Act made daughters coparceners by birth in ancestral/joint family property — with the same rights and liabilities as sons. Many families learned this during succession disputes years after the law changed. If your estate planning assumes sons inherit ancestral property exclusively, that plan is legally incorrect.

2. The December 2025 probate reform. Following a December 2025 amendment to the Indian Succession Act, mandatory probate has been abolished entirely across India — including the former Presidency towns of Mumbai, Chennai, and Kolkata. Probate is now optional everywhere, removing a procedural barrier that previously stalled estate transfers for months in those cities.

For NRIs and those with significant Indian assets, Section 228 of the Indian Succession Act allows foreign Wills to be recognised in India. However, executing a separate Indian Will often avoids procedural delays and saves weeks or months in transfer timelines.

Wills: The Foundation of Every Estate Plan

Key Requirements and Execution

A valid Will in India under the Indian Succession Act requires:

- Written form — no specific format, but must be in writing

- Testator's signature — or a mark, or direction to another person to sign in the testator's presence

- Two witnesses — each must witness the testator sign and sign the Will themselves in the testator's presence

- Sound mind and majority — the testator must be of legal age and mental capacity, free from coercion

Registration under the Indian Registration Act 1908 is not mandatory, but strongly advisable. A registered Will carries stronger evidentiary value and is significantly harder to challenge in court.

When Wills Work Well — and When They Fall Short

A Will does these things well:

- Provides legal clarity on asset distribution

- Names guardians for minor children

- Can explicitly address estranged family members

- Is relatively straightforward and inexpensive to draft

A Will has real limitations:

- Takes effect only at death — no protection during incapacity

- Can be challenged in court, particularly if informal or unregistered

- Becomes a public record when probated

- Offers no continuity mechanism for ongoing asset management

The most common drafting gap is coverage, not language. Many Wills fail to account for digital assets, jointly held property, and — most critically — nominee designations on financial accounts. A nominee on a mutual fund or bank account is legally a custodian, not an owner.

The Supreme Court confirmed this in Sarbati Devi v. Usha Devi (1984) and reaffirmed it as recently as Shakti Yezdani v. Jayanand Salgaonkar (2023). When a Will contradicts nominee designations, the resulting legal process is both time-consuming and expensive.

Equally overlooked: Wills that are never updated. Marriage, divorce, the birth of children, significant asset acquisitions, and business exits all warrant a review — and often, a revision.

Trusts in India: Types, Taxation, and When to Use Them

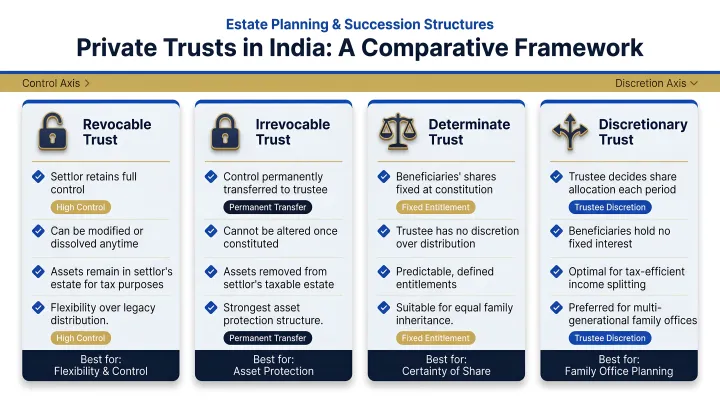

The Four Types of Private Trusts

Private trusts in India are governed by the Indian Trusts Act, 1882. They fall into four types across two axes:

| Determinate (fixed beneficiary shares) | Discretionary (trustee decides distribution) | |

|---|---|---|

| Revocable (settlor can cancel) | Revocable Determinate | Revocable Discretionary |

| Irrevocable (permanent) | Irrevocable Determinate | Irrevocable Discretionary |

Irrevocable trusts are increasingly preferred for estate planning among affluent families because they:

- Remove assets from the settlor's estate

- Maintain privacy (unlike a Will, which becomes public on probate)

- Allow phased distributions to beneficiaries — useful for minors or young adults

- Continue operating through the settlor's incapacity or death

- Provide a structured framework for family governance

The trade-off is significant: once an irrevocable trust is constituted, the settlor permanently relinquishes legal control over those assets — a structural commitment that warrants careful deliberation before execution.

How Trusts Are Taxed

Tax treatment varies sharply by structure — and this is where planning decisions carry significant financial consequences.

| Trust Type | IT Act Provision | Tax Treatment |

|---|---|---|

| Revocable trust | Section 61 | Income taxed in settlor's hands |

| Irrevocable determinate | General provisions | Taxed at each beneficiary's rate |

| Irrevocable discretionary | Section 164 | Taxed at Maximum Marginal Rate (~39%) |

The Maximum Marginal Rate for discretionary trusts — confirmed by an ITAT Special Bench ruling in April 2025 — runs approximately 39% under the new tax regime (30% base rate + surcharge + 4% cess). Under the old regime with income exceeding ₹5 crore, this can reach approximately 42.7%.

Trusts in India are not primarily a tax-avoidance tool. With no inheritance tax in force, the tax advantage is modest. The real value lies in orderly succession, privacy, continuity for minors or incapacitated beneficiaries, and reducing the risk of family disputes — outcomes that matter far more to most families than marginal tax savings.

Cross-Border Trust Considerations

For NRI families or those with offshore assets, trust planning involves a more complex compliance layer. Key obligations include:

- FEMA compliance: Trusts with non-resident settlors or beneficiaries must be structured in line with Foreign Exchange Management Act regulations

- Schedule FA disclosure: Resident beneficiaries of foreign trusts must declare their interest in their annual income tax return

- Black Money Act, 2015: Non-disclosure of foreign trust interests carries severe penalties — criminal prosecution is possible in egregious cases

These aren't technicalities. Getting the structure wrong can expose the settlor, trustees, and beneficiaries to regulatory action across multiple jurisdictions.

iVentures Wealth has advised on cross-border estate planning engagements where these considerations were central — including a case involving a senior executive in Gurugram with three NRI children in the US, where a family trust was structured to hold key business and property assets in alignment with applicable FEMA, income tax, and US succession frameworks. Structures involving non-resident beneficiaries or offshore assets require coordinated legal and tax counsel across each relevant jurisdiction.

Building a Complete Estate Plan: Practical Steps and Mistakes to Avoid

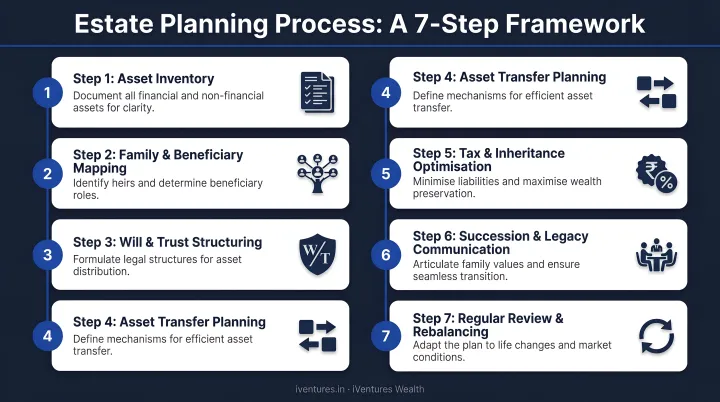

A Practical Starting Framework

- Inventory all assets — real estate, financial accounts, business interests, ESOPs, digital assets, insurance, HUF property, international holdings

- Identify your relevant succession law — Hindu, Muslim, or Indian Succession Act framework

- Define your goals and beneficiaries — who gets what, under what conditions, at what age

- Choose your instruments — Will, Trust, or both; most advisors recommend both for complex estates

- Appoint executors and trustees carefully — these are positions of significant legal responsibility

- Align nominee designations with your Will — misalignment is one of the most common and costly planning gaps

- Review and update regularly — after major life events, asset acquisitions, and at minimum every three to five years

Three Mistakes Affluent Families Make Most Often

Over-relying on nominees. A nominee is a custodian, not a legal heir. Nomination facilitates administrative transfer to the institution but does not create ownership rights. The Will or applicable succession law governs final ownership. Many families discover this only when disputes arise.

Failing to plan for incapacity. India lacks a durable power of attorney equivalent to those in Western jurisdictions. If you become incapacitated without a Trust or appropriate joint ownership structure in place, managing your assets becomes legally complicated. Irrevocable trusts and carefully structured joint ownership are practical alternatives.

Treating business and personal estate plans separately. For founders and family business owners, business succession and personal estate planning need to be designed together. Who inherits your shares? What triggers a valuation? Who has operational authority? These questions must be answered together, not in separate silos.

When to Bring in Professional Advisors

For straightforward estates — one or two asset classes, clear family structure, no NRI beneficiaries — a competent lawyer and a basic Will may be sufficient.

For complex estates — multiple asset classes, business interests, NRI or OCI beneficiaries, cross-border holdings — a do-it-yourself approach carries genuine legal and financial risk.

iVentures Wealth integrates estate planning directly into its wealth management engagements, coordinating investment structures, nominee designations, and succession goals so they work together rather than against each other. The firm works alongside senior legal counsel, including Supreme Court–level practitioners, to draft and review Wills and Trust documents as part of client mandates.

Frequently Asked Questions

What is estate planning in India?

Estate planning in India is the process of organising how your assets — property, investments, business interests, financial accounts — will be managed, protected, and distributed during your lifetime and after death. It uses instruments like Wills, Trusts, and gifts, under religion-specific succession laws.

What are the 7 steps in the estate planning process?

The core steps are: (1) inventory all assets, (2) identify your applicable succession law, (3) define beneficiaries and goals, (4) choose instruments — Will, Trust, or both, (5) appoint executors and trustees, (6) align nominee designations with your Will, and (7) review and update the plan regularly after major life events.

What is the biggest mistake in drafting a Will?

The most common mistake is failing to align nominee designations on financial accounts with the Will — nominees can legally override it if the two conflict. Not updating the Will after major life events like marriage, divorce, or new asset acquisitions is a close second.

What are the 4 types of trusts in India?

The four types of private trusts in India are: revocable determinate, revocable discretionary, irrevocable determinate, and irrevocable discretionary. Each varies by whether the settlor can cancel the trust and whether distributions to beneficiaries are fixed or left to trustee judgment.

What is the cost of preparing a Will in India?

A basic Will typically costs ₹5,000–₹20,000 in drafting fees, plus nominal stamp duty and registration charges at the sub-registrar. Complex estates involving multiple asset types, business interests, or NRI beneficiaries will cost more given the specialised legal work involved.

Can a trust be set up to avoid inheritance tax?

India abolished inheritance tax in 1985 via the Estate Duty Amendment Act, so this is not a planning concern here. Trusts are instead used for privacy, orderly succession, protecting assets for minor beneficiaries, and reducing the risk of family disputes.