Here's what makes this urgent: retirement in India can span 25–30 years. According to the World Bank, life expectancy at age 60 in India is already 19.7 years — and for HNI professionals with access to premium healthcare, that figure is likely higher. Every year of delayed planning narrows the compounding window and inflates the corpus you'll eventually need.

This article covers the definition of retirement planning, how to estimate your corpus, a step-by-step approach, life-stage guidance, and the aspects most people overlook until it's too late.

Key Takeaways

- Retirement planning is a coordinated strategy spanning investments, tax efficiency, healthcare costs, and withdrawal sequencing — not just a savings target

- India's 5.6% average CPI inflation means your corpus requirement is significantly larger than Western benchmarks suggest

- The right corpus typically equals 28–33x your annual retirement expenses — not the commonly cited 20–25x

- Start early: even modest SIP contributions benefit from 30+ years of compounding

- Healthcare costs, tax planning, and estate structuring are core to making your corpus last — not afterthoughts

What Is Retirement Planning and Why It Matters

Retirement planning is the ongoing process of identifying future income needs and building an investment strategy that adapts over time. Retirement planning is the ongoing process of identifying future income needs and building an investment strategy that keeps pace with your life. The goal: financial independence that holds, long after your last paycheck.

The key word is ongoing. A retirement plan is not a one-time spreadsheet exercise. It evolves with your income, life events, tax laws, and market conditions.

What retirement planning actually covers:

- Investment allocation across equity, debt, and alternatives

- Tax strategy — structuring withdrawals to minimise liability

- Healthcare provisioning, consistently the most underfunded element in most portfolios

- Estate planning — wills, trusts, and wealth transfer

- A realistic withdrawal plan that doesn't deplete your corpus too early

Only 37% of Indians currently have a retirement plan in place, down sharply from 67% in 2023 — despite retirement planning ranking as India's No. 1 financial priority. That gap — between knowing you should plan and actually having a plan — is what this guide is built to help you close.

How Much Retirement Corpus Do You Actually Need?

Your retirement corpus is the lump sum needed at retirement to sustain your lifestyle for the rest of your life. There's no universal number — it depends on your monthly expenses, inflation, life expectancy, and expected post-retirement returns.

A Simplified Estimation Approach

Use this four-step calculation:

- Estimate current monthly expenses — be honest about lifestyle costs, not just basic needs

- Inflate them to retirement day — use India's historical CPI average of ~5.6% to project what those expenses will cost in 15–20 years

- Multiply by retirement duration — typically 25–30 years for Indian retirees; longer for HNIs with better healthcare access

- Apply a safe withdrawal rate — more on this below

For example: a 40-year-old targeting retirement at 60 with ₹1 lakh/month in today's expenses will need significantly more than ₹1 lakh/month by the time they retire — and a corpus capable of sustaining those inflation-adjusted withdrawals for 25+ years.

Why the 80% Rule Doesn't Always Apply

The common rule of thumb — that you need roughly 80% of your pre-retirement income in retirement — often breaks down for UHNIs and early retirees. In practice, several costs move in the wrong direction:

- Travel spending peaks in the early retirement years

- Healthcare costs escalate continuously with age

- Lifestyle expenses rarely contract just because a salary has stopped

India's Inflation Problem Is Structural

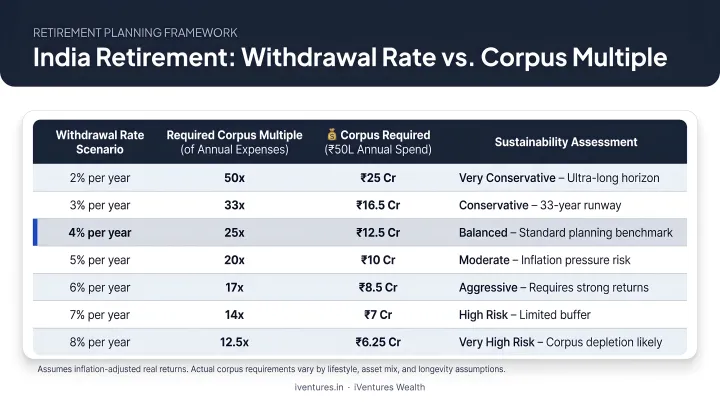

India's CPI inflation averaged 5.6% from 2012 through 2026, roughly double the 2–3% long-term average in Western economies. At 6% inflation, the rupee loses half its purchasing power in approximately 12 years.

For Indian retirees, that inflation rate pushes the recommended safe withdrawal rate down to 3–3.5% — not the US-standard 4%. The corpus multiples that follow:

| Withdrawal Rate | Corpus Required |

|---|---|

| 3.0% | ~33x annual retirement expenses |

| 3.5% | ~28–29x annual retirement expenses |

| 4.0% (US standard) | ~25x — insufficient for Indian conditions |

If you're planning with a 25x multiple, you're likely underfunded — particularly if you retire before 60 or carry a high-lifestyle baseline.

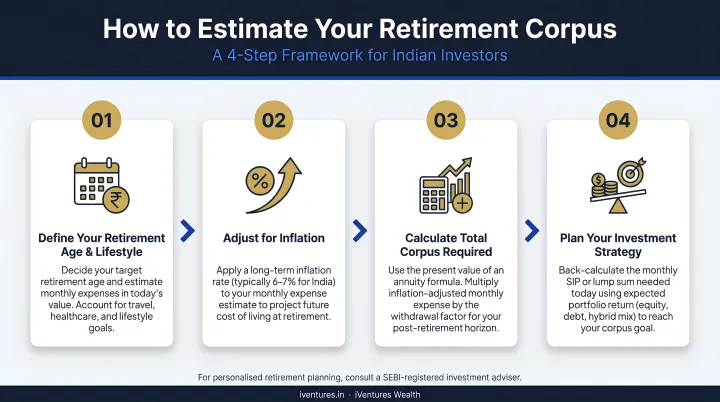

Key Steps to Building Your Retirement Plan

Step 1: Set a Clear Retirement Goal

Define your target retirement age, desired monthly income post-retirement, and any major anticipated expenses — healthcare, travel, children's responsibilities, legacy goals. A vague aspiration to "retire comfortably" is not a plan. You need a number and a timeline.

Step 2: Assess Your Current Financial Position

Take stock of everything:

- Accumulation assets: EPF balance, NPS corpus, mutual fund portfolios, direct equity, PPF

- Illiquid assets: Real estate equity, business value (if applicable)

- Liabilities: Outstanding loans, guarantees, pending obligations

- Monthly savings capacity: What you can actually invest after expenses

The gap between your current asset base and your required corpus becomes the foundation of your plan.

Step 3: Choose the Right Investment Vehicles

No single instrument solves the retirement challenge. The right approach combines instruments based on your timeline, risk tolerance, and corpus target:

| Instrument | Role in Portfolio | Key Benefit |

|---|---|---|

| NPS (Equity Scheme) | Long-term growth | ~14–15% 10-yr CAGR; tax benefits up to ₹2L |

| ELSS / Equity Mutual Funds | Accumulation | Inflation-beating returns over 20–30 years |

| PPF | Stability | 7.1% p.a., EEE tax status, sovereign-backed |

| EPF | Mandatory base | 8.25% p.a., tax-free at maturity |

| AIFs / Private Credit | UHNI-specific yield | 12–16% IRR with quarterly distributions |

| SWP from equity funds | Post-retirement income | Tax-efficient at 12.5% LTCG above ₹1.25L |

For HNI and UHNI clients, the allocation extends well beyond these retail instruments. iVentures Wealth, a SEBI-registered investment adviser, structures retirement portfolios across equity, debt, alternatives, and global assets, using an open-architecture model that is not tied to commission-generating products. For a CXO or doctor with ₹10 Cr+ in investable assets, that independence translates directly into better-aligned advice.

Step 4: Automate and Stay Consistent

Set up SIPs or automatic contributions so saving happens before discretionary spending. Consistency — not timing the market — is what drives compounding over a 25-year horizon. Even a modest SIP started at 30 will outperform a larger SIP started at 45, purely through time advantage.

Step 5: Review and Rebalance Annually

That consistency, however, only holds value if your plan stays aligned with reality. Market movements, income growth, new obligations, and tax law changes all create drift — which is why regular course correction matters. A retirement plan reviewed quarterly and rebalanced annually stays aligned with reality. One set at 40 and ignored until 58 does not.

Retirement Planning at Every Life Stage

The goal is the same across every stage. The tactics differ significantly.

Early Career (Ages 22–35)

Your primary asset at this stage is time. Even modest SIP contributions benefit from 30+ years of compounding. The focus should be on:

- Building the savings habit consistently

- Maximising equity exposure across a 25–30 year investment horizon

- Starting NPS early for tax-efficient retirement savings under Sections 80CCD(1) and 80CCD(1B)

Don't wait until you feel "financially ready" to begin. The cost of waiting five years at this stage is far higher than the cost of starting small.

Mid-Career (Ages 36–50)

Income is typically higher — but so are financial obligations. This stage requires deliberate choices:

- Maximise EPF contributions and step up SIPs as income grows

- Review whether your asset allocation still matches your updated retirement timeline

- Avoid lifestyle inflation absorbing every income increment

- Assess whether your corpus target needs revising based on actual expenses and goals

For HNIs and CXOs, this is also the right time to run a structured retirement projection — testing whether your current trajectory actually delivers the corpus you need, not just the one you assumed a decade ago.

Pre-Retirement (Ages 51–60)

The priority shifts from accumulation to preservation — protecting what you've built while structuring it for efficient withdrawal.

- Gradually move the portfolio toward lower-volatility instruments

- Project your EPF and NPS corpus at retirement

- Plan the transition from contribution to withdrawal — structuring SWPs, annuities, and income layers

- Address healthcare insurance before retirement, while you're still insurable at reasonable premiums

- Finalise estate planning documents — wills, trusts, nominees

Each stage demands a different posture. The earlier you recalibrate for where you are — not where you were — the more options you retain going into retirement.

Retirement Investment Instruments in India

Accumulation Phase Instruments

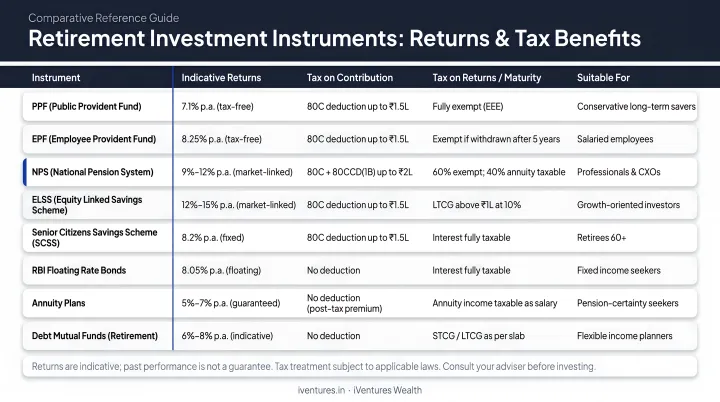

- EPF — Mandatory for salaried employees. Current rate: 8.25% p.a. (FY2024-25). Tax-free at maturity after 5+ years of continuous service.

- NPS — Market-linked with equity scheme CAGR of ~14–15% over 10 years. Tax benefits under Sections 80CCD(1) and 80CCD(1B) — total deduction up to ₹2 lakh. Requires partial annuitisation at age 60.

- PPF — Sovereign-backed at 7.1% p.a., 15-year lock-in with EEE tax status (exempt at contribution, interest, and maturity). Annual contribution capped at ₹1.5 lakh.

- ELSS / Equity Mutual Funds — Essential for beating inflation over 20–30 years. Volatility is the trade-off; long time horizons absorb it.

Post-Retirement Income Instruments

- SCSS (Senior Citizens' Savings Scheme) — Government-backed at 8.2% p.a. (FY2025-26), quarterly payouts, maximum deposit ₹30 lakh. Interest taxable at slab rate above ₹50,000/year.

- SWP from Equity Mutual Funds — Post Finance Act 2023, LTCG on equity fund SWPs is taxed at 12.5% above ₹1.25 lakh/year — more tax-efficient than debt funds, which are taxed at slab rate for investments made after April 2023.

- PMVVY — Closed for new subscriptions since March 31, 2023. No longer available.

For UHNI clients with larger retirement portfolios, standard instruments alone rarely suffice. iVentures Wealth structures additional income layers using REIT/InvIT distributions (6–8% yield with quarterly payouts), private credit AIFs (12–16% IRR), and bond ladders — asset classes outside the reach of typical retail portfolios.

Beyond Savings: What Most Retirement Plans Miss

Healthcare and Insurance Planning

Medical inflation in India runs at 12–14% annually — roughly 2–3x general CPI inflation. Out-of-pocket expenditure still constitutes 47.1% of total health expenditure in India, meaning a large portion of medical costs falls directly on individuals.

The practical implication: a retirement plan that doesn't include a dedicated healthcare reserve is materially understated. Secure adequate health insurance independently before retirement, ideally while still relatively young and healthy. Employer coverage ends when your employment does.

Tax Efficiency and Estate Planning

How you withdraw from your corpus is nearly as important as how much you accumulate. Key considerations:

- Structure SWPs from equity funds to stay within the ₹1.25 lakh LTCG exemption annually where possible

- Time redemptions across financial years to manage tax brackets

- Plan wealth transfer through wills and family trusts to minimise probate friction and tax leakage across generations

For retiring UHNIs managing multiple asset classes, cross-border holdings, and succession considerations simultaneously, these decisions rarely sit in isolation. iVentures Wealth coordinates tax optimisation, estate structuring, and portfolio management within a single advisory mandate, so each decision accounts for the others.

Inflation and Longevity Risk

Outliving your money is not a theoretical risk. Life expectancy at age 60 already stands at 19.7 years nationally — and is meaningfully higher for HNIs with access to premium healthcare. A 60-year-old today may need to fund 28–30 years of post-retirement life.

A corpus calculated on today's expenses, without inflation adjustment and without an adequate longevity buffer, will fall short. The plan needs to be built for the realistic duration, not the statistical midpoint.

Frequently Asked Questions

How do I plan and manage my retirement income?

Identify all income streams — EPF, NPS annuity, SCSS interest, mutual fund SWPs, rental income — and estimate monthly expenses adjusted for inflation. Ensure your withdrawal rate doesn't deplete the corpus over a 25–30 year horizon. A structured drawdown plan — sequencing withdrawals across instruments by tax efficiency and liquidity — holds up far better than ad-hoc decisions made year to year.

Is ₹2 crore enough to retire at 60?

For modest expenses in a lower-cost city, ₹2 crore may cover basics — but for someone expecting ₹80,000–₹1 lakh/month in today's terms, with 25+ years of retirement and rising healthcare costs, it is likely insufficient without supplemental income. At a 3.5% safe withdrawal rate, ₹2 crore generates roughly ₹58,000/year — not per month.

How can I plan to receive a monthly pension of ₹50,000?

Work backwards from the target. To generate ₹50,000/month (₹6 lakh/year) at a 3.5% withdrawal rate, you need a corpus of approximately ₹1.7 crore — inflation-adjusted to your retirement date. NPS annuity, SCSS interest, and SWPs from mutual funds can be layered to reach this figure once the right corpus is in place.

What are the best investments for post-retirement?

SCSS, SWPs from equity mutual funds, debt mutual funds (for pre-April 2023 investments), and high-quality bonds form the safety layer. Adding REIT/InvIT distributions and dividend-yield equities provides inflation protection. The right mix depends on risk tolerance — but some equity exposure is necessary to prevent real erosion over a 25-year retirement.

What is the 4% rule for retirement income?

The 4% rule was developed using US market and inflation data. In India, with structural inflation of 5–6%, most advisers recommend a more conservative 3–3.5% withdrawal rate — implying a corpus requirement of 28–33x annual expenses rather than the US benchmark of 25x.

Is wealth management the same as retirement planning?

No. Retirement planning is one component of broader wealth management, which also encompasses:

- Tax planning and estate planning

- Insurance structuring and business succession

- Investment strategy across all life goals

Retirement planning specifically focuses on building and distributing a corpus for post-work life — typically the largest single goal within a comprehensive wealth plan.